Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Aluminium’s recent surge isn’t just a war premium – it’s an energy premium. Gulf supply risks, higher power costs and thin inventories are reshaping the market’s cost floor.

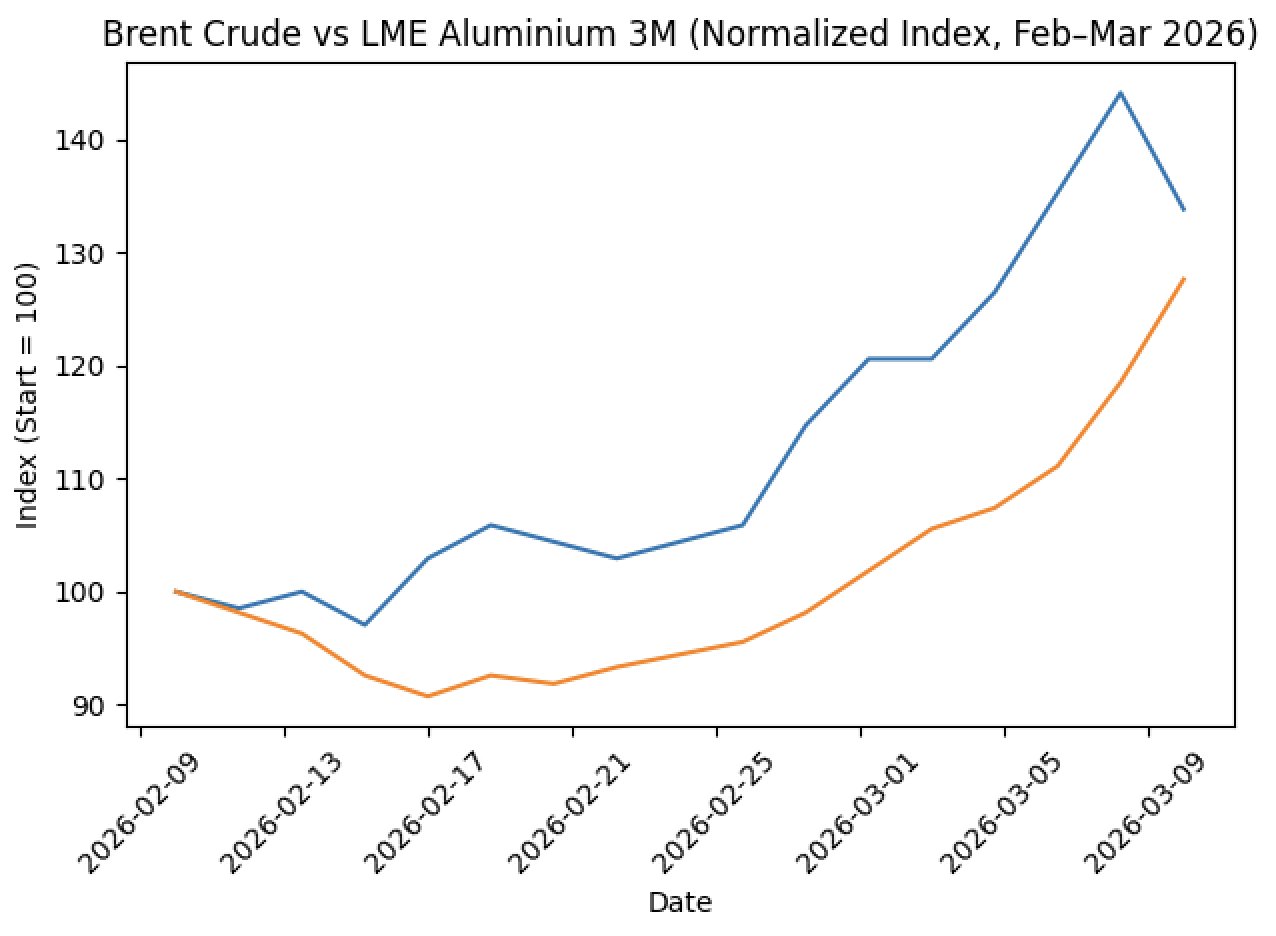

Aluminium’s thundering rally looks increasingly like a power market signal rather than a metals market one, as the price tracks the rally in crude oil and gas prices. The official LME cash price was $3,384.50/mt bid, and $3,385.00/mt offered, 6 March, while the Final Evening Evaluation [close] for the three-month contract stood at $3,446/mt. The move follows a steep climb through early March, as geopolitical tensions in the Gulf intensified, and continue to rattle global markets.

The response suggests traders are not simply pricing the risk of disrupted metal shipments. Aluminium is the most electricity intensive of the base metals, and the current price strength points to growing concern over energy supply disruption and the potential inflation of power costs. In effect, the aluminium market appears to be attaching a risk premium to the possibility that higher energy prices could tighten smelter economics and constrain production.

What was once described as the age of peace now looks increasingly like the age of disruption. Oil and gas markets have reacted quickly to conflict in the Middle East, but aluminium may prove the more revealing signal.

Price moves remain below the $4,000 plus spike seen in 2022, but it represents a clear repricing of risk as energy markets lurch higher and the industrial metals complex absorbs a new geopolitical shock.

Blue line: LME aluminium three-month price (indexed). Aluminium climbs sharply through early March before easing slightly from the latest high.

Orange line: Brent crude oil (indexed). Oil moves higher first, suggesting rising energy costs helped drive the subsequent move in aluminium.

Aluminium reacts to energy risk, not just geopolitical risk

At first glance, the rally looks like a familiar war premium. It is something closer to an energy premium. Aluminium is one of the most electricity-intensive industrial products in the world. Smelting converts alumina into metal through electrolysis, meaning power costs typically account for around 30 to 40% of operating expenditure. When energy systems become unstable, aluminium’s cost base moves almost immediately.

The current conflict has already begun to interfere directly with both energy supply and aluminium production in the Gulf. Hydro’s Qatalum joint venture has started a controlled shutdown after its gas supplier suspended deliveries, while Aluminium Bahrain has declared force majeure on shipments, citing transit disruption around the Strait of Hormuz. Restarting a smelter is not like restarting a furnace. Once curtailed, full recovery can take months.

The Middle East produces roughly 6.8 million tonnes of primary aluminium each year, about 9% of global output and more than one fifth of supply outside China. Around three quarters of that metal is exported, almost all moving through the Strait of Hormuz.

The immediate market concern is logistics. The strait has never been formally closed to commercial shipping despite decades of geopolitical tension. Markets do not require a blockade to reprice risk. Reduced vessel traffic, higher insurance premia and occasional disruption are sufficient to tighten effective supply. These frictions tend to appear first in prompt pricing and regional premiums, which is exactly where the current tightening is emerging.

Rio Tinto’s suspension of second quarter premium negotiations with Japanese buyers offers an early signal that producers and consumers are recalibrating in real time. An initial offer around $250/mt was withdrawn as tensions escalated. That is not a negotiating tactic; it reflects a supply chain whose costs and delivery routes have become harder to predict.

The tightening is not confined to bilateral negotiations. LME warehouse inventories have been trending lower in recent years, leaving the market with a smaller visible buffer than during previous shocks. When stocks are thin, disruptions in production or transport translate more quickly into price volatility.

LME aluminium stocks have tightened sharply over the past fortnight, with live warrants dropping from 420,850 tonnes on 27 February to 273,775 tonnes by 9 March, a fall of roughly 147,000 tonnes.

Gulf disruption exposes a fragile global supply chain

But the deeper story lies beyond logistics: energy is increasingly the binding constraint on aluminium supply. Cheap gas and abundant electricity helped turn the Gulf into one of the world’s major aluminium exporting regions over the past two decades. When that energy system is disrupted, the metal system moves with it. As Andy Leyland, MD and Co-Founder of SC Insights says: “Cheap gas has fuelled energy-intensive aluminium production in the Middle East. The disruption to Qatari supply both threatens production and pushes up costs elsewhere, as energy prices rise.”

The impact extends well beyond the Gulf itself. Electricity prices in many industrial regions remain linked directly or indirectly to fossil fuel markets. Higher gas prices lift power tariffs, higher oil prices lift freight rates for both raw materials and finished metal, and insurance costs add a further layer. Each element pushes aluminium’s marginal production cost higher.

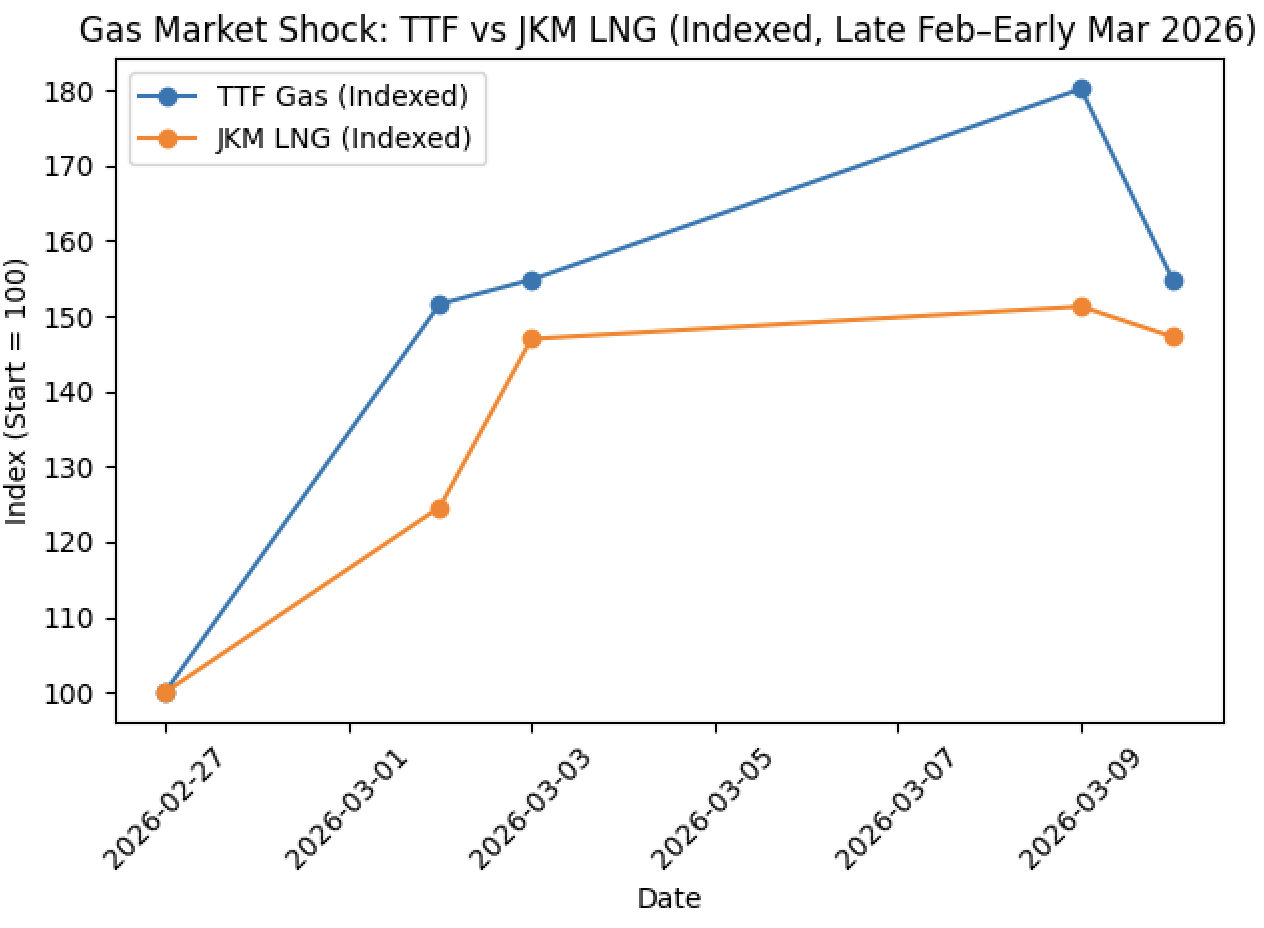

European gas and global LNG prices surged in early March as traders priced supply disruption risk in the Gulf. The Dutch TTF benchmark climbed from roughly €30/MWh in late February to almost €56/MWh by 9 March, while Asia’s JKM LNG benchmark rose from around $10.7/MMBtu to above $16/MMBtu over the same period. With the Strait of Hormuz a key artery for global LNG trade, even the possibility of disruption has been enough to jolt gas markets sharply higher.

China’s capacity ceiling removes the market’s traditional shock absorber

The timing of this shock is awkward for the aluminium market because its traditional shock absorber has weakened. For much of the past decade, rising prices could trigger additional output from China, which steadily expanded smelting capacity and absorbed much of the world’s marginal demand. That mechanism is now constrained. Chinese aluminium capacity is effectively capped at around 45 million tonnes under government policy, and utilisation rates are already close to that ceiling.

The result is that China is no longer the flexible supplier it once was. Imports of primary aluminium have increased while exports of semi-manufactured products have slowed. In effect, the world’s largest producer is absorbing more metal internally rather than releasing it to global markets.

Thin inventories and idle smelters increase price volatility

Outside China, smelter flexibility is even more limited. A significant amount of Western smelting capacity sits idle after years of high power prices. Restarting those facilities requires long term electricity contracts at competitive rates. In today’s energy environment, those contracts are difficult to secure, particularly as large electricity consumers such as data centres compete for the same supply.

This is why aluminium volatility has increased in recent years. The market is emerging from a long period of surplus into one where spare capacity is thinner, inventories are smaller and production is tightly linked to energy availability.

The Iran conflict has simply exposed that structure. Even if shipping routes remain open and curtailed plants restart within months, the broader repricing may prove durable. Higher energy costs raise the marginal cost of aluminium production globally. In commodity markets, marginal cost tends to act like gravity. Prices may move above or below it temporarily, but they rarely remain disconnected from it for long.

There is also a financial dimension. Hard assets often attract renewed investor attention during periods of geopolitical stress. Aluminium options activity has increased in recent sessions, suggesting that financial positioning is amplifying underlying fundamental tightening rather than offsetting it.

The market is therefore not yet pricing a collapse in supply. It is pricing friction: in energy, in logistics and in inventories.

If the Strait of Hormuz remains open and energy markets stabilise, the war premium embedded in aluminium could fade. But if power markets remain volatile and transport risk persists, aluminium may simply settle at a higher cost floor. What looks like a geopolitical rally may therefore turn out to be something more structural. Aluminium has always been described as a metal of electricity. The current market is merely rediscovering how closely the two remain connected.

Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

In critical minerals, the real question isn’t how much you hold but how quickly materials can be used. We explore global stockpiling strategies and ask whether, without processing capacity, governance and strong alliances, stockpiles risk symbolism over security.