Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

LME three-month nickel jumped 2.7% on Wednesday after Indonesia's Finance Minister confirmed that President Prabowo had signed off on export tariffs covering nickel and coal. The specific rates remain unpublished, the market has not waited for them, and the price move is only a small part of the story.

Indonesia is caught in a structural contradiction of its own making. The country built the world's dominant nickel processing industry on two inputs it does not control: Chinese capital and Middle Eastern sulphur. The Iran conflict has now put pressure on both simultaneously.

Jakarta's answer - a windfall tax on its most valuable commodity exports - has introduced a third variable into a cost structure that was already deteriorating. The market is only beginning to work out what that means.

The sulphur dependency is the most direct transmission mechanism. Indonesia's high-pressure acid leach plants, which convert low-grade laterite ore into battery-grade mixed hydroxide precipitate, consume roughly 24 to 30 tonnes of sulphuric acid per tonne of nickel produced. Around 75% of the sulphur feedstock comes from the Middle East. Gulf shipping disruption has pushed sulphur prices 30 to 35% above their pre-conflict level of around $500 per tonne. Before the conflict began, sulphur costs were already running at roughly half the total operating cost of a typical HPAL plant. That ratio has now moved materially.

Indonesia is also a net crude and fuel importer. The same conflict that is disrupting its sulphur supply chain is raising its energy import bill. A windfall tax on nickel exports is the rational fiscal response to a government staring at a widening budget deficit. The timing, however, places that fiscal pressure directly on producers whose operating margins are already contracting.

That is a contradiction Jakarta cannot easily resolve. Much of Indonesia's nickel processing capacity was financed by Chinese capital, and Beijing has a direct interest in affordable battery materials. The Indonesian government cannot simply tax its way out of that relationship. Export rates, when they are eventually set, may be lower than the market is currently pricing. But the cost structure underneath them has changed regardless of where the tariff lands.

For the global nickel price, the question is how quickly this feeds through to supply. A market previously forecast to show a surplus of 90,000 tonnes - Sumitomo had been working with a figure of 256,000 tonnes - could swing into deficit this year, according to revised modelling from Macquarie's analysts following Jakarta's December tightening of ore production quotas. NPI output fell an estimated 10% year-on-year through January and February. The direction of travel has not reversed.

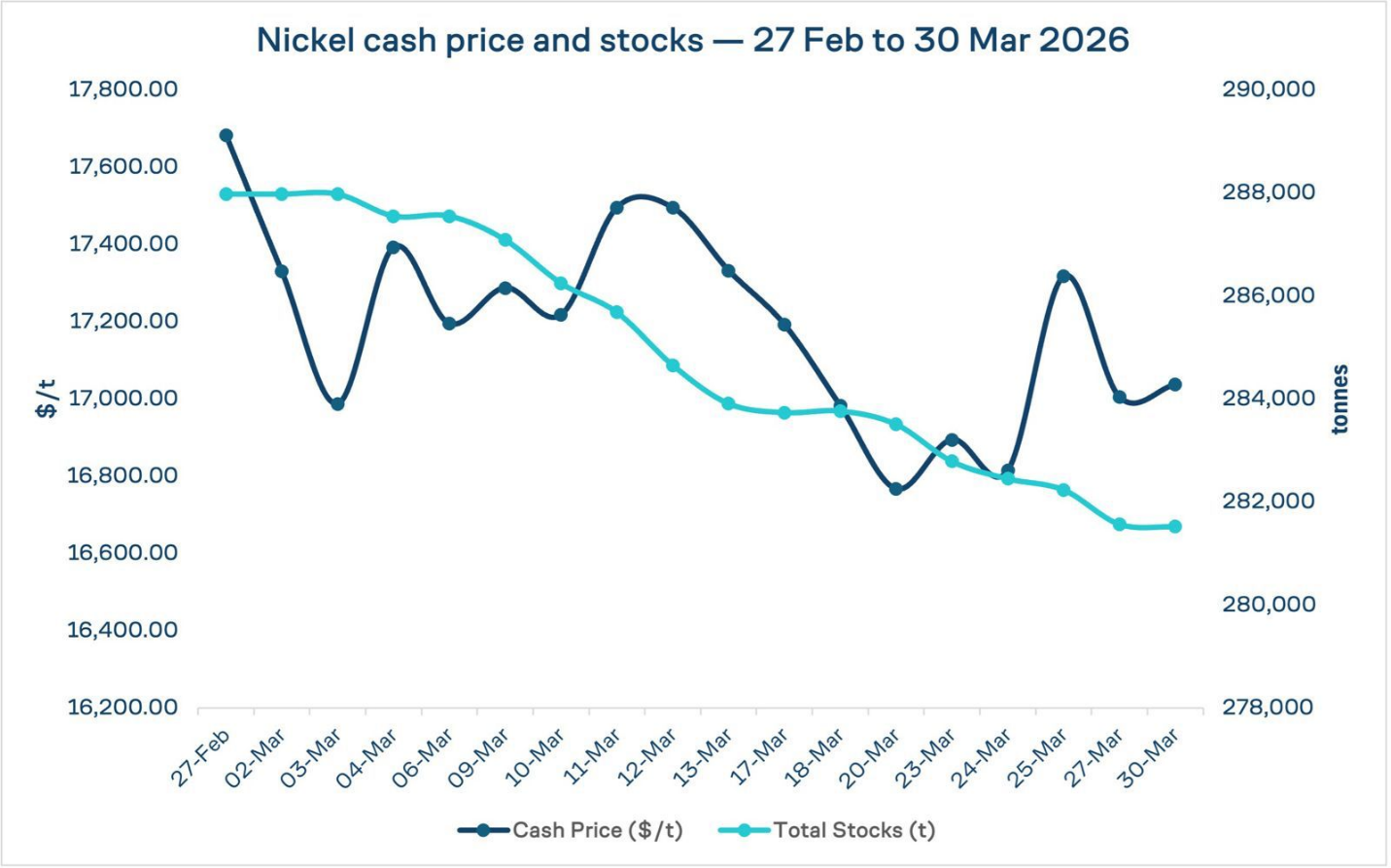

LME cash nickel was trading at $17,000 to $17,020 on Friday, precisely at the lower bound of the $17,000 to $18,000 floor Macquarie has identified. The December 2027 contract is bid at $18,155. Warehouse stocks stand at 282,456 tonnes, with 18,276 tonnes in cancelled warrants, indicating near-term draws already in progress.

The spread between spot and the 2027 contract is the market's current working assumption: an orderly resolution to the sulphur supply problem, tariff rates that disappoint the bulls, and a deficit that builds slowly rather than arrives suddenly.

That assumption requires Indonesia to navigate its fiscal pressures without further disrupting the processing capacity it has spent a decade building. The export tax announcement has just made navigation harder.

LME price and stock data as of 27 March 2026. Supply and cost data sourced from Macquarie Group and Mining.com.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Aluminium’s recent surge isn’t just a war premium – it’s an energy premium. Gulf supply risks, higher power costs and thin inventories are reshaping the market’s cost floor.

In critical minerals, the real question isn’t how much you hold but how quickly materials can be used. We explore global stockpiling strategies and ask whether, without processing capacity, governance and strong alliances, stockpiles risk symbolism over security.