Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

After one of the most extreme boom-and-bust cycles in recent commodities history, the lithium market is entering a more mature and balanced phase, but uncertainty remains. Prices have corrected sharply, but demand continues to grow, and the focus is shifting from resource abundance to the challenge of delivering usable supply. Execution delays, policy friction and refining bottlenecks are now emerging as the key forces shaping the market.

Lithium carbonate prices rose from around $7,000/mt in 2020 to a peak near $70,000/mt in 2022, before falling sharply through 2023 and 2024. Prices have stabilised well below their 2022 peak, with lithium carbonate trading broadly in the mid-teens, to around $20,000/mt.

Despite the sharp price correction, demand has continued to expand. Annual battery demand surpassed 1 TWh in 2024, with EV battery demand growing 25% year on year. Electric car sales rose to 17 million, while global battery manufacturing capacity reached 3 TWh, illustrating how quickly the sector moved from scarcity to overbuild.

The supply response is now visible in project execution. Rio Tinto has said it will slow the pace of construction at Nemaska during 2026, Albemarle has idled the remaining operating train at Kemerton, IGO and Tianqi have ceased work on Kwinana’s second lithium hydroxide plant, and Core Lithium’s Finniss operation remains under restart study.

Lithium Carbonate Price Cycle. Lithium carbonate prices rose from around $7,000/mt in 2020 to a peak near $70,000/mt in 2022, before falling sharply through 2023 and 2024. Prices have stabilised well below their peak, with recent movements indicating a slowdown in the rate of decline.

Individually, these are incremental adjustments. Collectively, they reduce near term supply growth and concentrate future output in fewer projects.

The constraint is most visible in chemical conversion. Several refining projects have encountered commissioning delays, cost overruns and operational challenges. Conversion capacity remains a limiting factor in the delivery of battery grade material.

Lithium resources could expand, but resources do not determine price. Deliverable supply does.

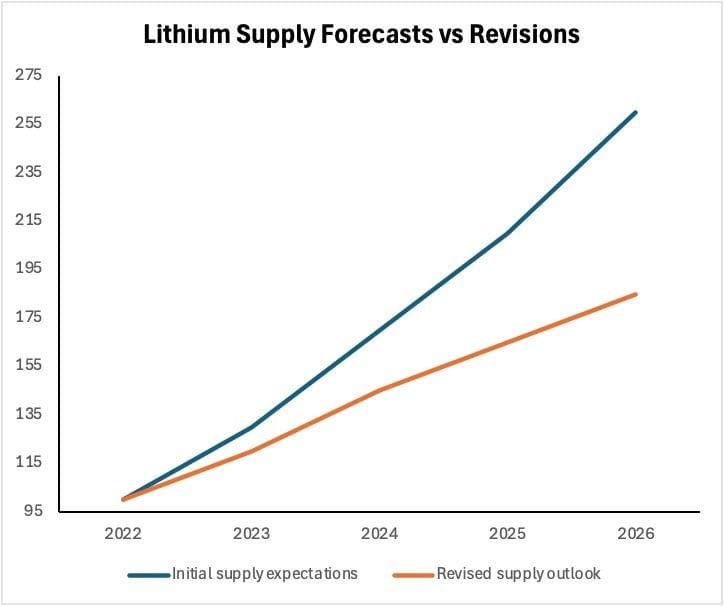

Lithium Supply Forecasts vs Revisions. Initial supply expectations have risen steadily since 2022, but revised supply projections remain consistently lower. The divergence reflects project delays and slower than expected capacity ramp up.

The market does not require exceptional demand growth to tighten. It requires supply growth to fall short of the expectations formed during the price spike.

That gap is beginning to emerge.

Aterian CEO Charles Bray said local value addition requirements, often described as resource nationalism, are better understood as an evolution of post-colonial economic policy aimed at retaining more downstream value within producing countries.

By encouraging processing closer to the point of extraction, these frameworks support domestic industrial development and shift value capture upstream. From a market perspective, however, the effect is to extend project timelines and increase execution complexity, slowing the conversion of geological resources into deliverable supply. This introduces friction into global supply chains and tightens the near-term availability of battery grade material.

Zimbabwe provides a clear example. Restrictions on the export of lithium concentrate have reduced the volume of spodumene reaching international markets, as authorities push for domestic processing capacity to be developed.

Policy and execution are extending timelines. Refining capacity takes years to build. Projects face technical and financial constraints. Higher cost operations remain offline. The result is a delay between resource development and market delivery.

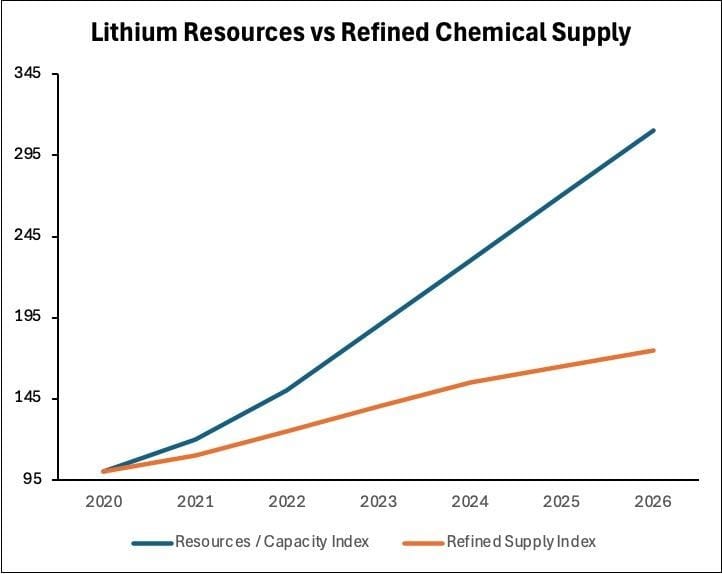

Lithium Resources vs Refined Chemical Supply. Lithium resource capacity has expanded from an index of 100 in 2020 to over 300 by 2026, while refined chemical supply has increased more gradually to around 175. The gap highlights a growing constraint in conversion capacity.

This is typical of commodity cycles. High prices drive expansion. Expansion overshoots demand. Prices fall. Investment slows, higher cost producers exit and project timelines extend. The market tightens not because resources disappear, but because marginal supply arrives later than expected.

Lithium appears to be entering that phase.

According to S C Insights lithium prices in 2025 were unsustainably low for an industry which needs to attract investment.

A meaningful supply response could take years.

The pace of decline has slowed, suggesting that expectations for uninterrupted supply growth are being reassessed. The adjustment is visible in project pipelines, refinery utilisation and capital allocation decisions.

The key variable is no longer how much lithium exists, but how quickly it can be converted, processed and delivered.

In that sense, the current surplus is less secure than headline resource numbers imply.

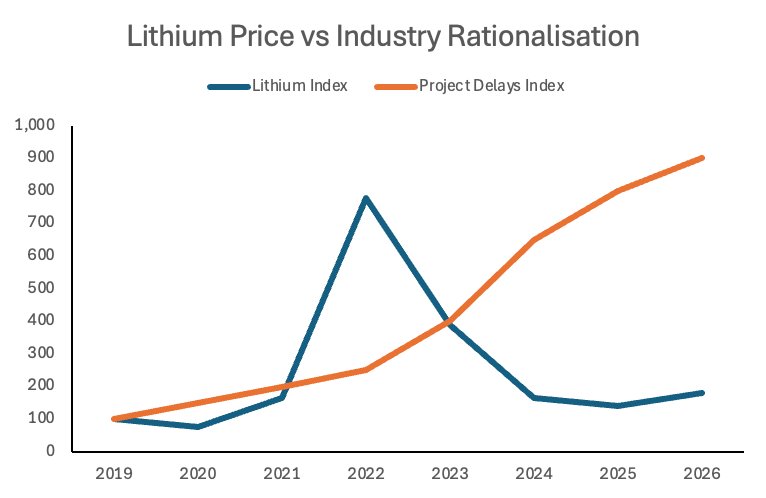

Lithium Price vs Industry Rationalisation. The lithium price index peaked in 2022 before declining sharply, while the index of project delays and curtailments continued to rise. Industry rationalisation is increasing as prices fall, reducing near term supply growth.

Sources: USGS, World Bank Commodity Price Data, industry forecasts and company disclosures, analysis by CPAL. Indices are illustrative and normalised to a common base year to show directional trends.

Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Aluminium’s recent surge isn’t just a war premium – it’s an energy premium. Gulf supply risks, higher power costs and thin inventories are reshaping the market’s cost floor.

In critical minerals, the real question isn’t how much you hold but how quickly materials can be used. We explore global stockpiling strategies and ask whether, without processing capacity, governance and strong alliances, stockpiles risk symbolism over security.