Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Tungsten prices are surging as war, stockpiling and China’s export squeeze drain the system. Inventories are vanishing, supply can’t keep up, and every missile fired deepens the deficit. This isn’t a cycle – it’s the market tightening fast.

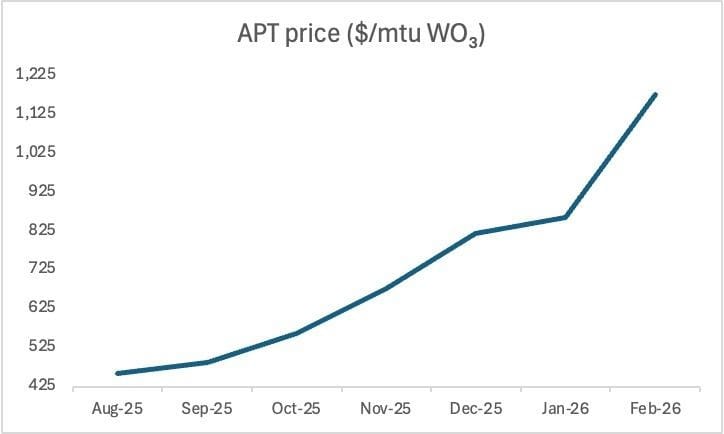

Ammonium Paratungstate (APT) prices are rising sharply as war accelerates the drawdown of tungsten units. APT is the primary intermediate product in the tungsten supply chain. It is the standard reference material from which most tungsten products are produced and priced.

Tungsten demand is concentrated in a small number of critical applications, with around 50–60% of global consumption in cemented carbides used in cutting tools and industrial equipment (U.S. Geological Survey, Mineral Commodity Summaries, January 2025), forming the base load of the market.

Beyond that, demand is shifting. Automotive and engineering account for roughly 25–30%, while smaller but faster-moving segments – particularly defence, aerospace, and electronics – are becoming increasingly influential (U.S. Geological Survey, Statistics and Information, 2026). Electronics and power applications are among the fastest-growing segments, supported by electrification and semiconductor demand (Global Tungsten Market Trends, Valuates Reports, 2025).

APT prices rise as Chinese export controls tighten supply. Source: ScrapMonster; SMM; company analysis

Defence demand is also accelerating. The US conflict with Iran is consuming munitions at scale, both offensive and defensive. Each missile fired carries a material cost in critical inputs such as tungsten, used for its density and heat resistance in high performance military systems.

This is not a typical demand cycle. It is inventory depletion.

Inventories are being drawn down faster than they can be replenished. Restocking is no longer optional; it is immediate, but replenishment is colliding with a system already under strain.

APT prices have risen from $450 to $500 per mtu in late 2025 to above $1,100 in early 2026, while ferrotungsten has climbed from around $45 per kg to $200 per kg. The price signal is clear: the physical market is tightening.

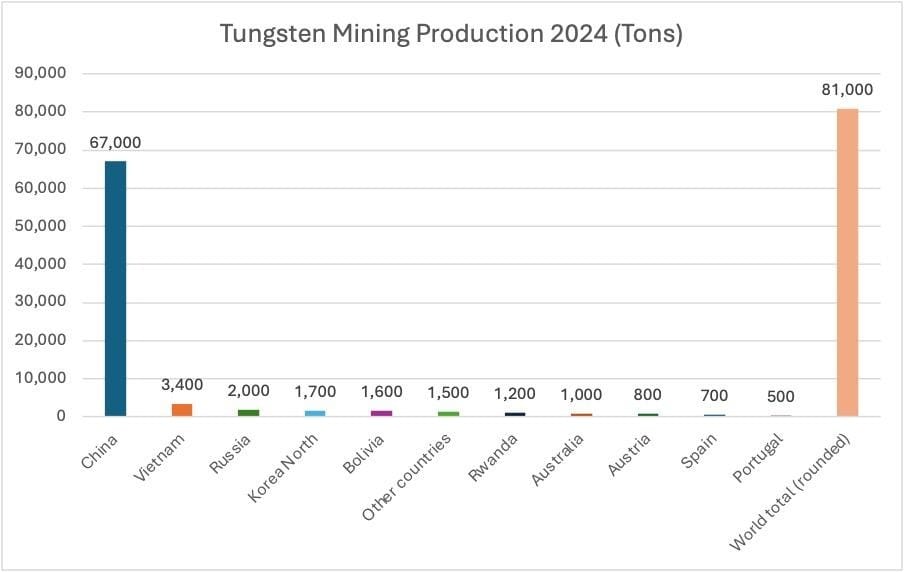

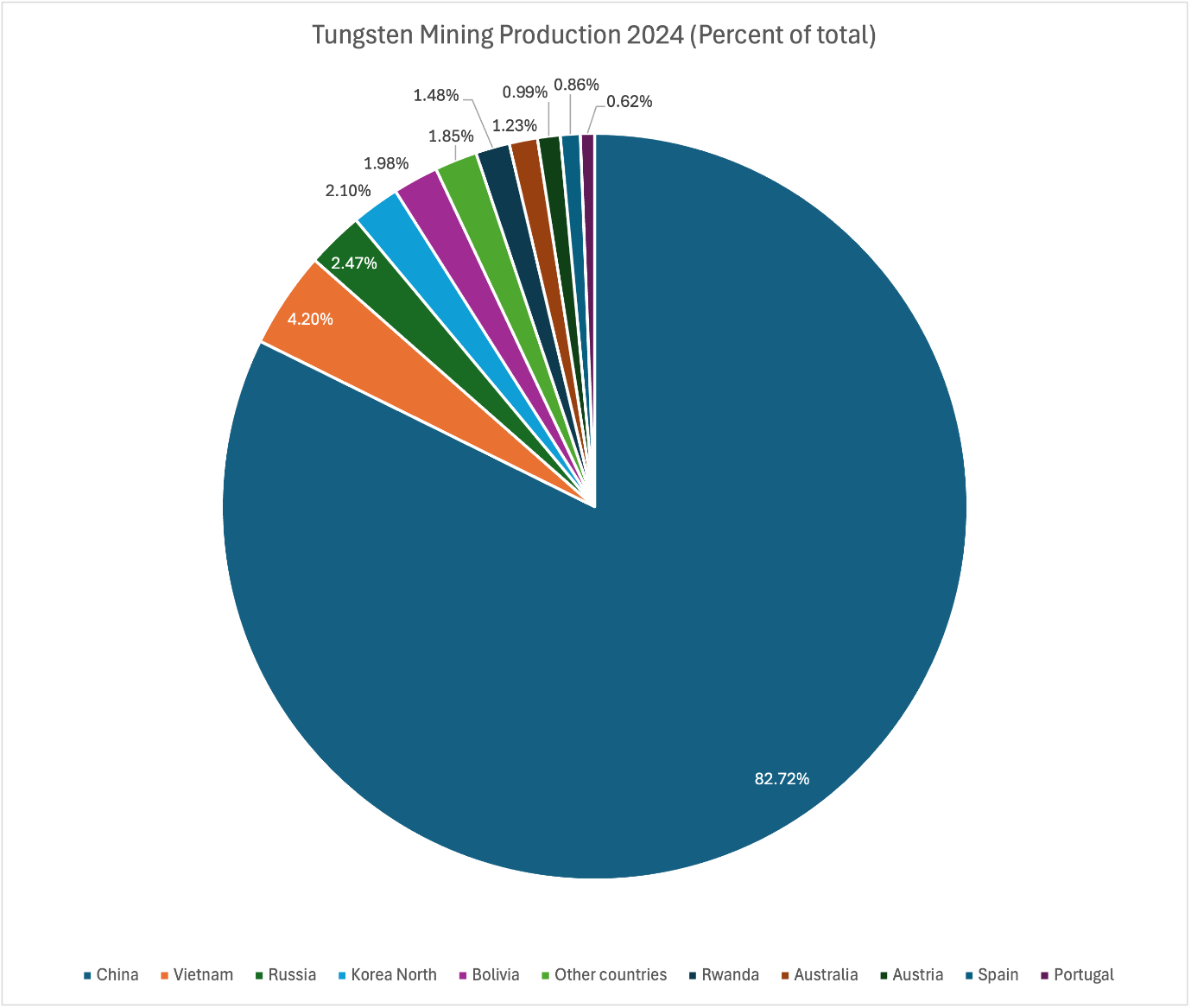

China dominates both mining and processing, producing around 67,000 tonnes of tungsten annually, roughly 83% of global output. The rest of the world combined accounts for less than 20%, with no single producer exceeding 5% (US Geological Survey, 2024). This is not a balanced market. It is a single-point system

Source: US Geological Survey, 2024Source: US Geological Survey, 2024

This concentration has always been a structural feature, but now it is a constraint. Supply is tightening. Demand is rising. The two are reinforcing each other.

The market used to absorb this through inventories and arbitrage, but those buffers are weakening. Export controls have tightened seaborne availability, and the adjustment has been delayed but sharp. Spot units have become harder to source, inventories have been drawn down, and buyers have been forced back into the market at higher prices.

Concentrate prices were already rising before the policy shift, reflecting declining ore grades and constrained mining quotas in China. Those costs are now feeding through into APT and downstream products. Delivery times are lengthening, suggesting the squeeze is not confined to a single point in the supply chain.

Consumers are responding by moving upstream. Some are seeking direct access to mine supply; others are entering processing partnerships to secure units. This is already visible in the tungsten market. Almonty Industries has signed binding offtake agreements with a US defence contractor and processor, committing supply of tungsten oxide directly into missile, drone and ordnance production (Almonty, 2025).

This effectively links primary production to end-use demand, bypassing traditional spot market exposure. Governments are moving in parallel. The United States is expanding stockpiling initiatives and actively supporting non-Chinese supply chains, adding a further layer of demand for accessible material.

Supply cannot respond at the same speed. Higher prices are improving the economics of projects outside China, but supply response remains slow and uneven. A small number of projects are emerging as potential drivers of non-Chinese supply. The Sangdong mine in South Korea, currently being redeveloped by Almonty, is expected to produce around 4,000 tonnes of tungsten concentrate annually, making it one of the largest new sources outside China (Mining.com, 2026).

In Southeast Asia, Vietnam’s Nui Phao complex remains the single largest producing asset outside China, supplying roughly 3,400 tonnes per year and supported by one of the few integrated processing facilities in the region (Vietnam Briefing, 2025).

In North America, Canada’s Mactung project represents one of the largest undeveloped tungsten resources globally, but remains in the permitting and development stage, highlighting the long lead times required to bring new supply online.

These projects illustrate the constraint. New supply exists, but it is concentrated in a handful of assets, often years from full production and still dependent on permitting, financing and processing capacity. Recycling offers some flexibility but is not scalable enough to offset primary supply constraints in the short term.

The constraint is not absolute resource availability; it is access. Usable, policy-compliant tungsten units are becoming harder to secure. Geography is starting to matter more than price.

This is no longer a balanced market. Policy is shaping supply. War is accelerating consumption. Stockpiling is reinforcing demand.

The buffers that once allowed the system to absorb shocks – inventory, arbitrage, and flexible flows – are shrinking. What remains is a market where availability is tightening faster than supply can respond.

Tungsten is not short in the ground; it is short in the system. And the system is losing optionality.

Nickel is waking up – and Jakarta just hit the alarm. Indonesia’s dominance rests on supply chains it doesn’t control, now squeezed by geopolitics and taxes. A looming surplus could vanish fast, with global nickel prices caught in the middle.

Lithium is shifting from boom‑and‑bust volatility to a tighter, more complex market, as project delays, policy friction and refining bottlenecks slow the flow of deliverable supply.

Aluminium’s recent surge isn’t just a war premium – it’s an energy premium. Gulf supply risks, higher power costs and thin inventories are reshaping the market’s cost floor.

In critical minerals, the real question isn’t how much you hold but how quickly materials can be used. We explore global stockpiling strategies and ask whether, without processing capacity, governance and strong alliances, stockpiles risk symbolism over security.