Copper’s phantom tariff

London Metal Exchange copper stocks remain near their highest levels since 2013, but available metal is tightening as cancellations rise.

London Metal Exchange copper stocks remain near their highest levels since 2013, but available metal is tightening as cancellations rise.

Konkola Copper Mines has taken its Nchanga smelter offline for planned maintenance, with the shutdown forming part of a wider cycle of outages across Zambia’s copper-processing sector.

Aluminium Bahrain [Alba] has agreed to acquire Aluminium Dunkerque, the largest primary aluminium smelter in the EU, in a deal valued at $2.2 billion, subject to regulatory approval.

London Metal Exchange copper stocks remain near their highest levels since 2013, but available metal is tightening as cancellations rise.

The copper is there. The question is how much of it is still available.

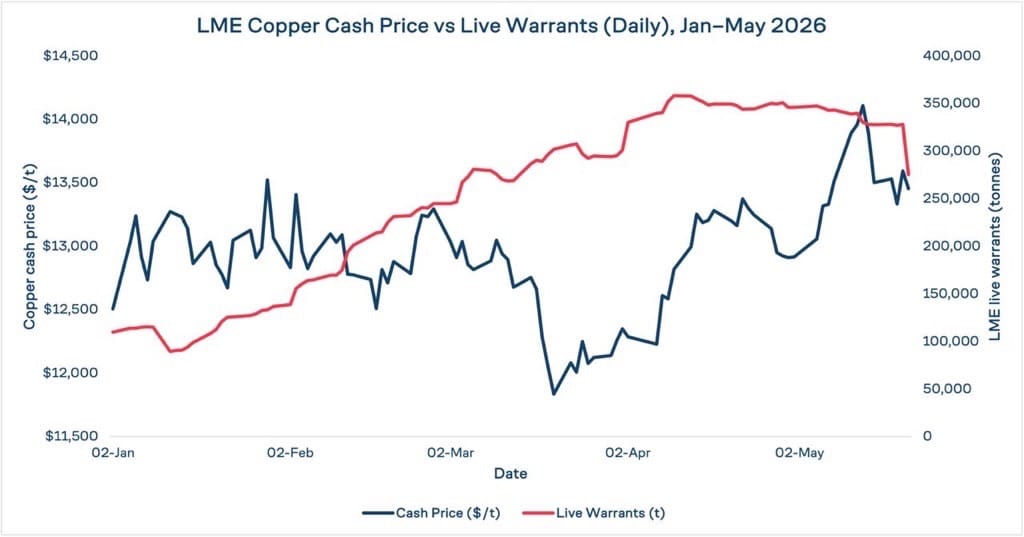

London Metal Exchange copper stocks remain near their highest levels since 2013, but available metal is tightening as cancellations rise. This does not point to a fundamental shortage of copper, but to a market repositioning ahead of potential US tariffs on refined metal that have yet to materialise.

In the last full week of May, the share of London Metal Exchange copper stock cancelled and booked for withdrawal jumped from 16.5 percent on 20 May to 29.7 percent on 21 May, before rising further to around 37 percent. The increase was driven mainly by New Orleans and Baltimore, where just over 60 percent of copper stock has been cancelled. Around 51,000 tonnes were ordered out of LME sheds in a single step in late May, contributing to the largest monthly net outflow from LME warehouses since December. Prices were driven by other factors. Copper cash price rose from $12,147/mt on 2 April to $14,097/mt on 13 May before easing to $13,513/mt by May 28, a move largely attributed to ceasefire talks between the US and Iran and the usual macro rotation.

The inventory data tells the more important story, and it points to a single destination.

A build that masked the turn

From January 12, LME copper stocks nearly tripled from 141,550 tonnes to a peak of 400,625 tonnes on 13 April. The forward curve confirmed the loosening market, shifting from a small cash backwardation early in the year into contango as metal flowed into warehouses. On the surface, copper looked well supplied, and the weakness seen in early April fits that narrative.

Then the flow reversed.

The sharp rise in cancellations in late May was not routine warehouse churn. Closing stocks began to fall, and the metal leaving the exchange had somewhere specific to go.

Copper is moving, not disappearing

It is heading to the United States. The premium of Comex front-month copper over the LME cash price widened beyond $500/mt, the largest gap since last autumn, opening a profitable arbitrage and pulling spare units west. US refined copper cathode imports surged to 532,427 tonnes in the first quarter of 2026, more than double the roughly 253,000 tonnes imported in the same period of 2025, while exchange inventories in the country climbed toward record highs as traders positioned ahead of the 30 June deadline.

The world’s visible copper stock is not disappearing. It is being moved into one jurisdiction and held there.

The economics are simple. A trader that can buy copper against the LME price and deliver it into a US market pricing a future tariff captures the spread. The metal itself is unchanged. What changes is its location. In that sense, the arbitrage is less a bet on copper demand than a bet on policy.

Fresh supply is not keeping pace with the units being drawn west. Output in Chile, the world’s largest producer, fell 13.8 percent year on year in April to 399,954 tonnes, pressured by lower ore grades and a tough base comparison. The base effect exaggerates the decline, but the deterioration in grades is the more structural issue, limiting how quickly new supply can refill the sheds the arbitrage is draining.

Supply constraints are also extending beyond mine output. Tight sulphuric acid availability has weighed on cathode production from some African and Indonesian smelters, further limiting the flow of fresh refined units into a market already being pulled toward the United States.

Priced for a duty that has not arrived

The trade is being built around a tariff that does not yet apply to refined copper.

Refined copper, the form deliverable against both LME and Comex contracts, still does not face a direct US import duty. The latest White House update broadened and adjusted the tariff framework for steel, aluminium and copper products, but stopped short of imposing an immediate duty on refined copper itself, leaving the market focused on the commerce secretary’s expected 30 June update and the earlier recommendation for phased duties of 15 percent from 2027 and 30 percent from 2028.

The Comex premium is therefore the market pricing in a potential future duty. Metal is moving now to sit inside the US border before the line has officially been drawn.

Stockpiles are not independence

This is where the position begins to turn on itself.

The United States is accumulating record copper inventories, yet its dependence on imported metal continues to rise rather than fall. Net import reliance reached 57 percent in 2025 from 45 percent in 2024. The current drawdown is relocating metal, not relocating dependency. A measure intended to rebuild domestic supply chains is, for now, pulling the world’s copper into US warehouses while the country’s refining capacity remains structurally limited.

Against just 264,100 tonnes of LME copper available on live warrant as of 3 June, and falling, the arbitrage does not require tariffs to materialise in order to keep working. The incentive already exists. Metal will continue moving whether or not the June 30 review results in new duties.

The visible buffer that capped prices through April is being drained ahead of the test, even as the test itself may yet be delayed.

The copper market is tightening, not because supply has disappeared, but because geography now matters more than outright availability.

Sources

Reuters, Bloomberg and Mining.com, 22 May 2026 (LME copper warehouse withdrawals).

Bloomberg, 27 May and 1 June 2026 (Comex-LME arbitrage and US import flows).

Chile National Statistics Institute (INE), via Reuters and Mining.com, 29 May 2026 (Chile copper production).

US Presidential Proclamation, Adjusting Imports of Copper into the United States, 30 July 2025.

Congressional Research Service, Section 232 National Security Tariffs on Copper Imports, 23 April 2026 (implemented rates and effective date).

USGS, Mineral Commodity Summaries 2026.

UN Comtrade Database

Stay connected with our latest developments. Share your details to receive updates and analyses from LME Insight.