Alcoa Corporation has agreed to acquire South32's entire aluminium value chain for an implied enterprise value of up to $5.6 billion in a deal that represents one of the largest consolidations in the global aluminium industry in years.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 26 June 2026.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 26 June 2026.

It was a risk-off week across the LME base metals complex, with all six metals finishing lower week-over-week. While there was some resilience shown in the back half of the week, particularly from copper, even the red metal still finished down 2.1% on the week.

Base metals also appeared to be caught up in the broader cross-asset de-risking across global markets. The selloff in technology and semiconductor equities weighing on investor appetite for cyclical and growth-sensitive assets. That does not mean metals sold off purely because of equities, as each metal still had its own micro drivers. However, when macro books are under pressure, industrial metals can become a source of liquidity as funds reduce gross exposure, protect margin, or free up capital after losses elsewhere

With the Fed’s messaging around 2% inflation firmly in focus the US dollar has seen continued support with the DXY sitting comfortably above 101 with rate rises now likely. China also remains mixed with industrial profits being supported by upstream and technology-linked sectors but downstream manufacturing, property demand, and consumer-facing sectors remain lackluster. Metals may need at least one of these macro headwinds to ease before the broader uptrend can reassert itself.

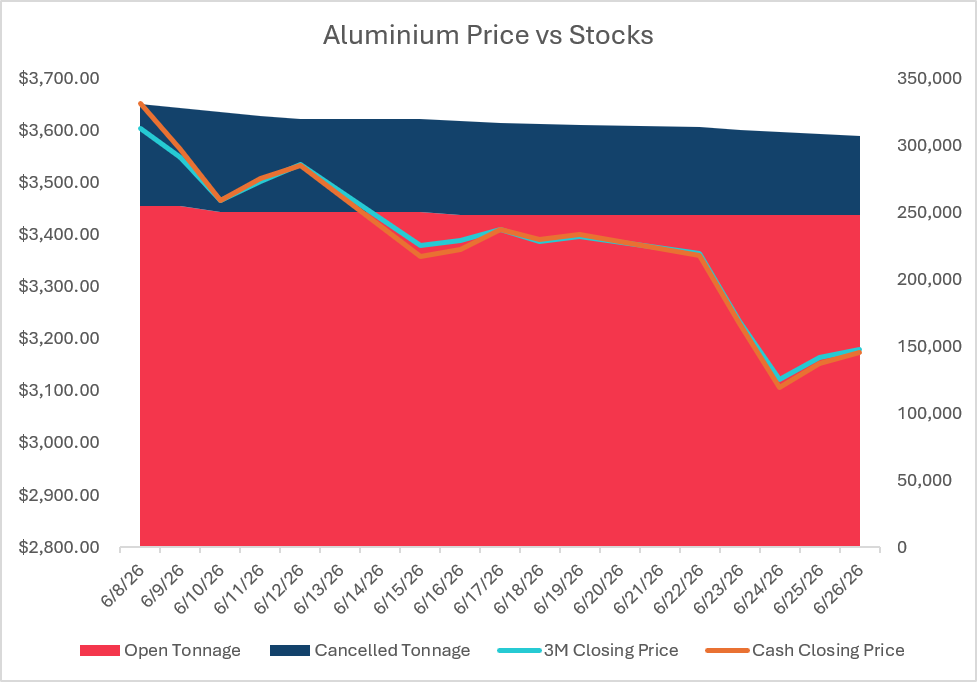

Aluminium opened the week at its high and then sold off sharply through the middle of the week before stabilizing into Friday. With news of increased vessel shipments through the Strait of Hormuz, a lot of the risk premium came out of the market. Though it should be stated that any agreement on the Strait is fragile at best. Barring any other micro or macro shocks, aluminium will likely continue to follow a similar pattern: risk-off on easing Middle East tensions and risk-on should peace talks falter.

There were no major movements as already cancelled tons flowed out of the warehouse without additional warrant cancelations. Perhaps traders are taking a wait and see approach as to how quickly aluminium will begin flowing out of the Gulf again. As we often see with a sharp selloff, nearby spreads continued to ease and we saw cash-3s settle as wide as $16.50c midweek – a level not seen since the beginning of March this year.

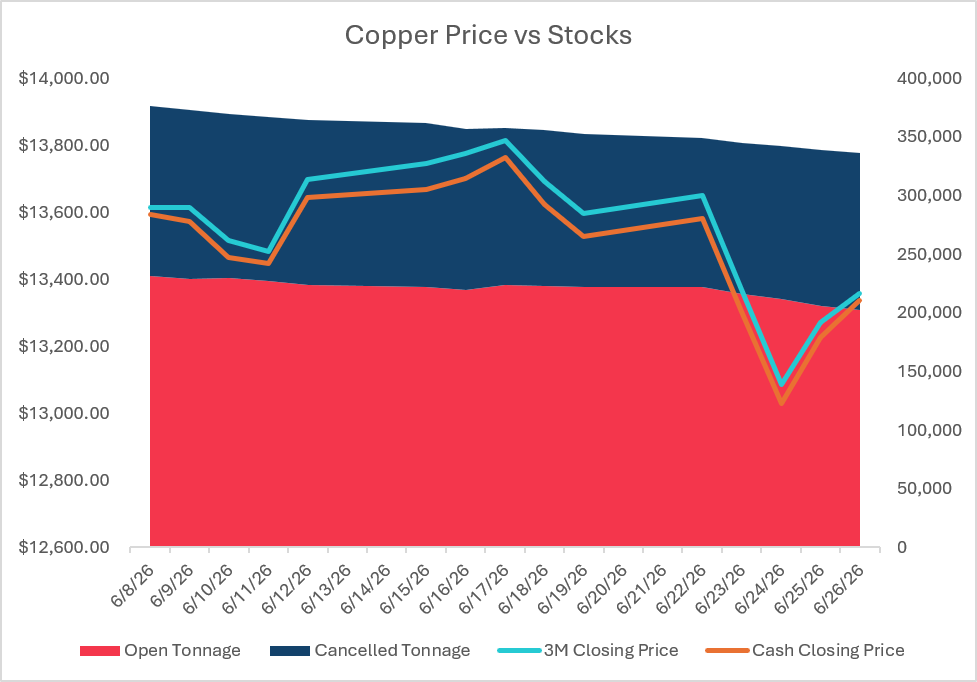

Copper was the relative winner last week, managing to cap losses at 2.1%. However, the micro picture looks a little more supportive as we continue to see cancelations and decreases in visible stocks. We also saw the cash-3s spread tighten to finish the week at just $21.5C after spending the last few weeks in the 60s and 70s.

June 30th is a pivotal date for the copper market as we await news from the US commerce secretary as to whether they will recommend refined cathode be included in the Section 232 tariffs. Given the tightening spreads and stock situation, copper could be primed for a move higher should tariffs be enacted on cathode. Particularly if traders attempt to repeat the arbitrage trade we saw in 2025 – moving metal from LME warehouses to CME. This will largely depend on how quickly any tariff would be implemented and how quickly metal could be imported to the US.

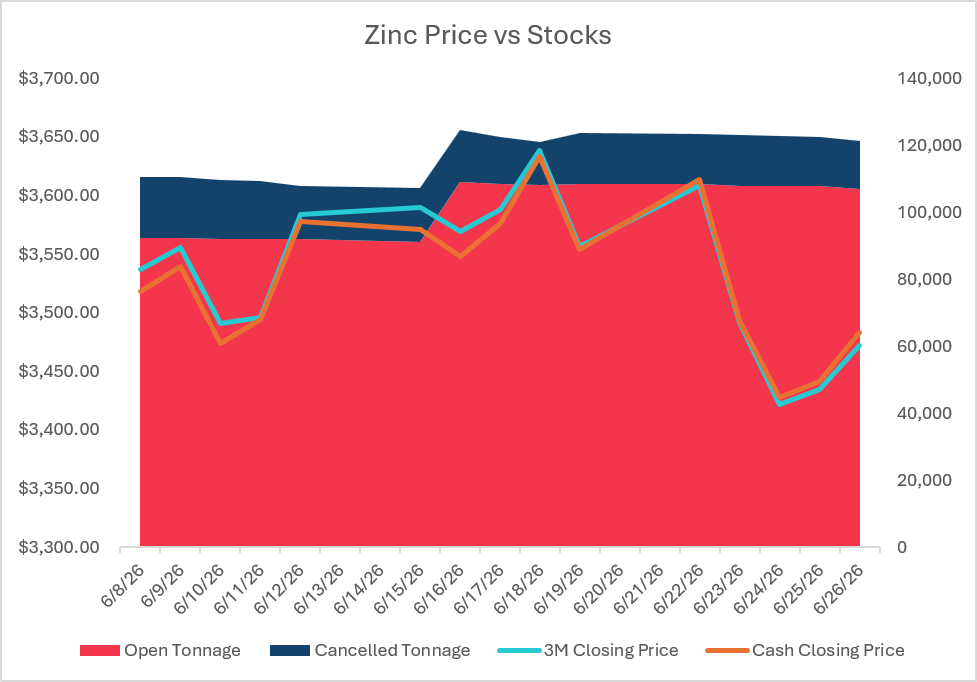

Zinc fell nearly 4% this week and on Wednesday hit its lowest level in almost two months. Zinc’s demand remains closely tied to galvanized steel, construction, and manufacturing activity and with higher rates and a strong dollar, these types of infrastructure projects may face headwinds.

Interestingly the stocks and spreads position remains precarious. LME stocks are just 4 days of global consumption and the cash-3s spread has moved from contango to backwardation, finishing the week at $11b – all this despite the selloff in the flat price. If the backwardation continues to grow we may see traders look to take advantage of worsening demand by delivering into the exchange. However, if the macro situation improves and demand increases, the stock and spreads could materially worsen as cancelations increase and spreads tighten further.

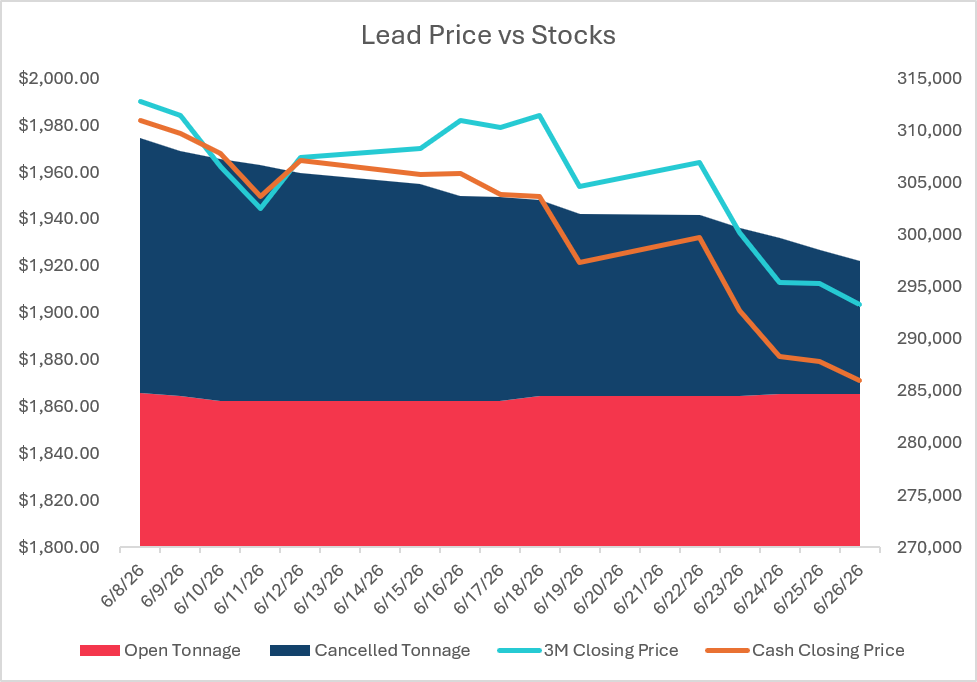

Lead continues to follow the wider group in its flat price moves, though because it is not as widely traded by the speculative community its moves are often not as volatile as the rest of the complex. That said the sideways moves we had seen over the last few weeks definitely turned downward as the 3M price is now perilously close to breaking below $1900/mt – a level it has held since March this year.

With cash-3s holding steady at $32.50C and stocks stable, there is no sign of tightness in the lead market. Given the lack of fund activity and its often contrarian behavior, lead may also not see an immediate boost should the rest of the complex turn around on any improving macro readings.

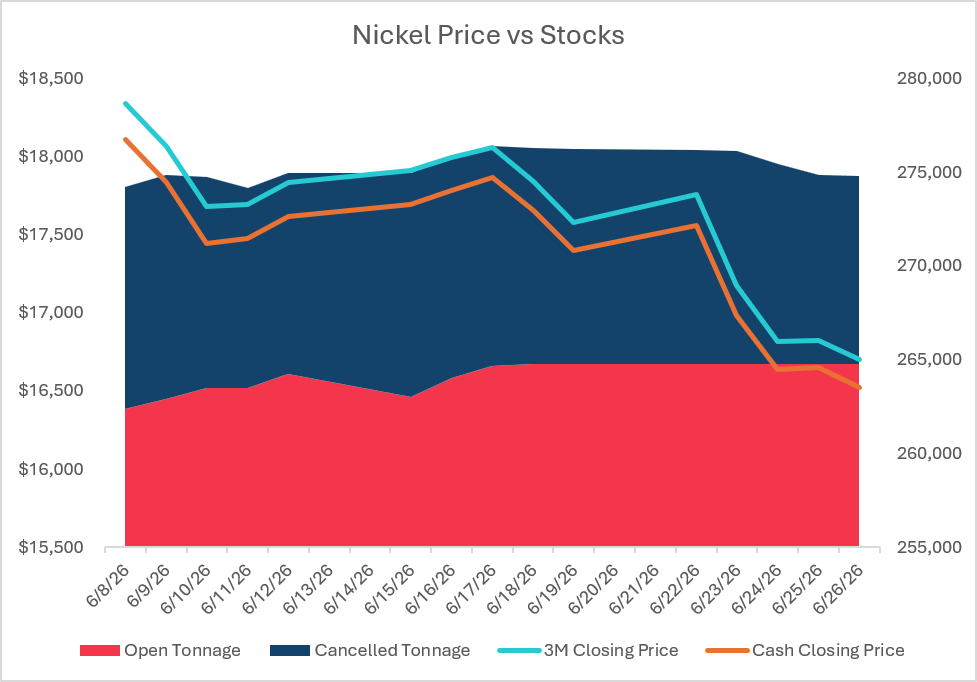

Nickel was one of the weakest metals this week, falling nearly 6% and unlike copper and aluminium that were able to recoup some losses, nickel closed at the weekly low. It broke through the $17k handle which undoubtedly attracted additional technical selling.

Indonesia’s mining industry has not yet decided on its nickel production quota for the balance of 2026 and until there is clarity around this number we could see additional selling without any reduction in Indonesian production being enforced.

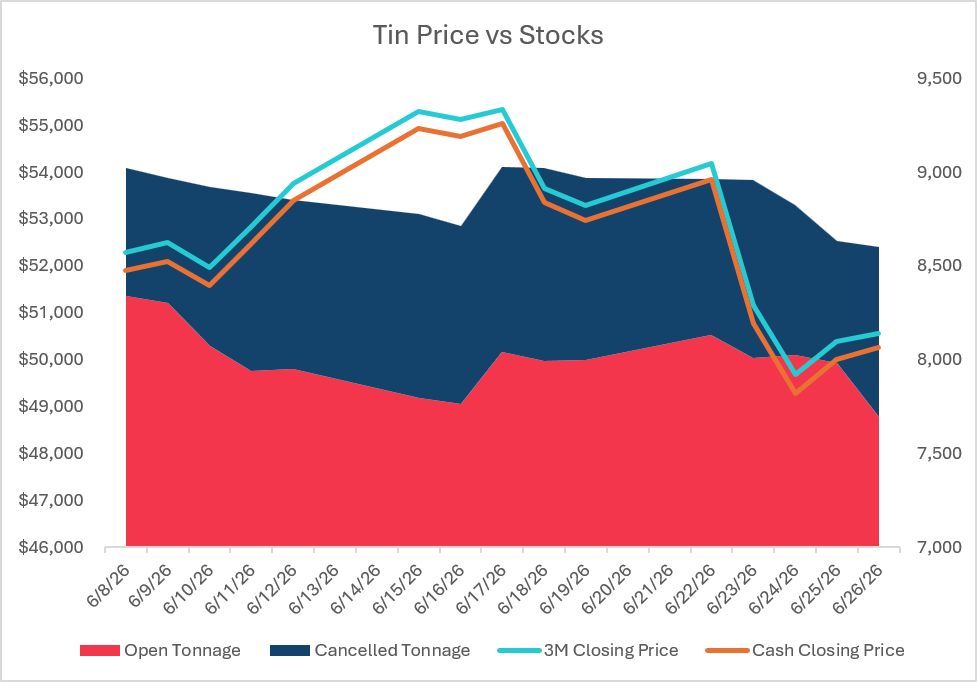

Tin was the weakest metal of the week, down nearly 7% as we saw a mix of profit taking and de-risking after a very elevated price environment for the prior two weeks. It managed to hold the $50k handle to close the week but several closes below this level could attract significantly more selling.

The high price environment and increased volatility make tin vulnerable to sharp corrections when macro sentiment turns lower.

Alcoa Corporation has agreed to acquire South32's entire aluminium value chain for an implied enterprise value of up to $5.6 billion in a deal that represents one of the largest consolidations in the global aluminium industry in years.

The European Commission has pushed back its planned aluminium scrap export restrictions to September 2026, according to sector group European Aluminium, after missing an original spring 2026 target. The Commission has not publicly explained the delay.

Century Aluminum and Brimstone, a California-based innovator in alumina production, signed a memorandum of understanding aimed at establishing what would be the first fully domestic mine-to-metal aluminium supply chain in the United States.