Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

It was a steadier but uneven week across the LME base metals complex, with the market moving away from the aggressive risk-off tone seen in the prior week. The complex was not uniformly stronger, but the balance improved: tin and zinc were the clear outperformers, copper and nickel managed modest gains, and aluminium stabilized. The most important macro shift came from the softer US labor data, which took some pressure off the dollar and reduced the market’s confidence that the Fed will need to tighten as aggressively.

The weaker US jobs picture was important for metals because it came alongside still-expansionary but moderating manufacturing data. US nonfarm payrolls missed expectations, ADP private payrolls also slowed, and the ISM and S&P Global manufacturing PMIs both eased but remained above 50. China’s official manufacturing PMI also moved back into modest expansion, while the UK, Germany, Japan, South Korea, and China’s private PMI readings all showed continued factory growth. That combination helped stabilize growth-sensitive metals without creating the sort of demand surge that would justify a broad-based rally.

Middle East risk also remained central, but this week the market increasingly priced the reopening and normalization of flows through the Strait of Hormuz rather than a further deterioration. Oil prices stayed under pressure as shipping and oil flows recovered, removing some of the energy and logistics risk premium that had previously supported aluminium in particular. At the same time, the truce and technical talks remain fragile, so the market is not yet able to fully discount geopolitical risk.

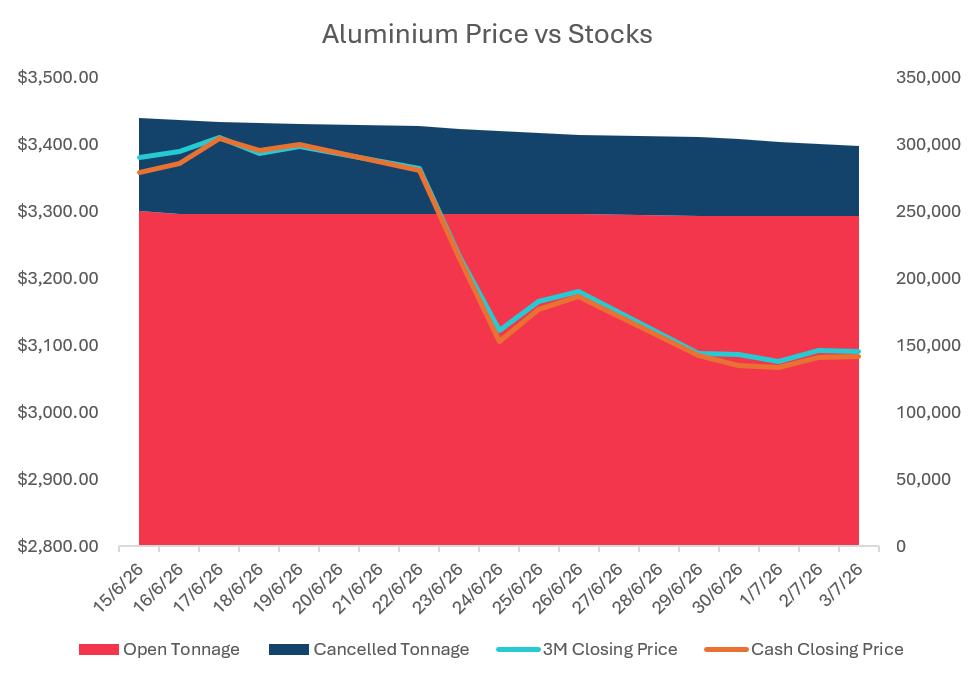

Aluminium spent the week consolidating after the sharp selloff seen in the prior week. The market opened close to where it finished and traded in a very narrow range. With lower oil prices, improving Strait of Hormuz traffic, and softer US Midwest premiums, this all points to less urgency in the physical market.

The micro picture was also more mixed than outright bullish. LME stocks fell again but several supply-side headlines leaned in the other direction. Slovalco is expected to restart 75,000 tons of annual capacity in Slovakia and Mag 7 plans to bring back 75,000 tons of production to Missouri.

Cash-3’s barely changed week-over week as we remain in a small contango after a protracted period of backwardation. However, should cancellations increase we could easily see a shift from contango to back as traders scramble for units.

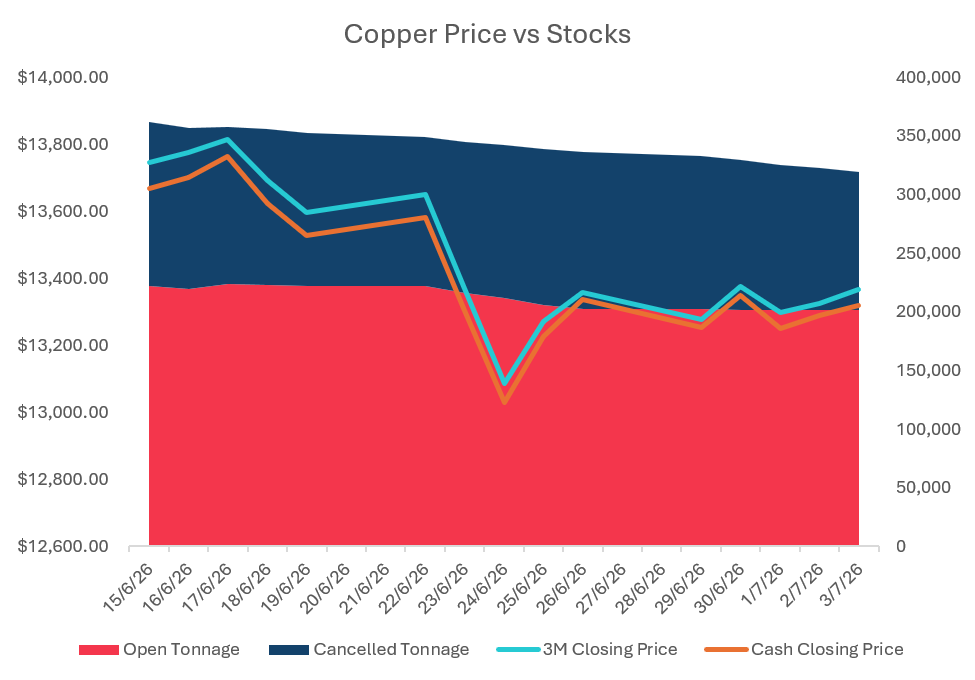

Copper was modestly higher on the week, helped by the weaker US dollar and a less hostile macro backdrop after the softer US labor data. We did not see a breakout, but it remained resilient relative to the scale of recent volatility.

The US tariff question remained unanswered as June 30th came and went without any announcement from the Commerce Department. Any tariff on refined cathode would likely lead to a dramatically increased premium for CME over LME units but timing will be key. If we see a repeat of 2025, LME stocks will see significant draws as traders look to move units to the United States. Cash-3s moved further into contango this week but should LME stocks start moving to CME locations this will likely change.

An interesting development in the concentrates market continued this week with Antofagasta’s move toward spot-indexed TC/RC pricing. While this is more of a smelter margin concern amid concentrate availability, it continues to support the longer-term bullish copper narrative.

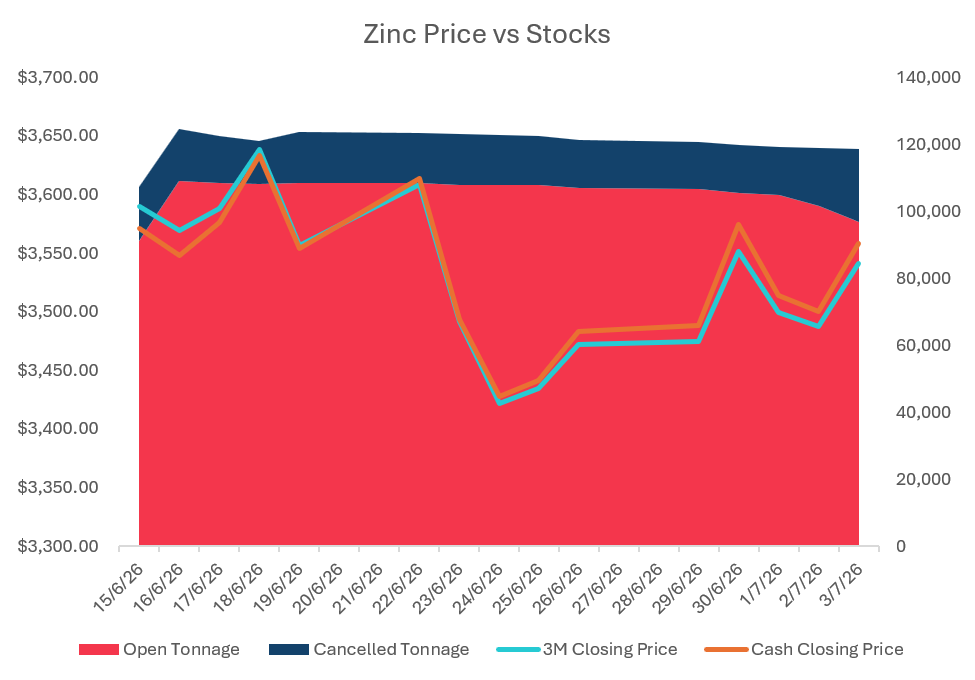

Zinc was one of the stronger metals this week, moving higher as the macro backdrop improved and manufacturing PMIs stayed in expansion territory. Zinc remains highly exposed to galvanized steel, construction, infrastructure, and industrial production so the combination of a softer dollar and still-positive factory data provided enough support for a rebound.

Cancelled tons rose again while LME stocks continue to fall, leading to the cash-3s back tightening to $17.5B to finish the week after reaching a high of $22.50B on Tuesday. The zinc market looks increasingly like a regional availability story where China can increase output but ROW smelting has continued to underperform. If stocks remain low and the backwardation continues to build, zinc could remain well supported even without a dramatic improvement in end-use demand.

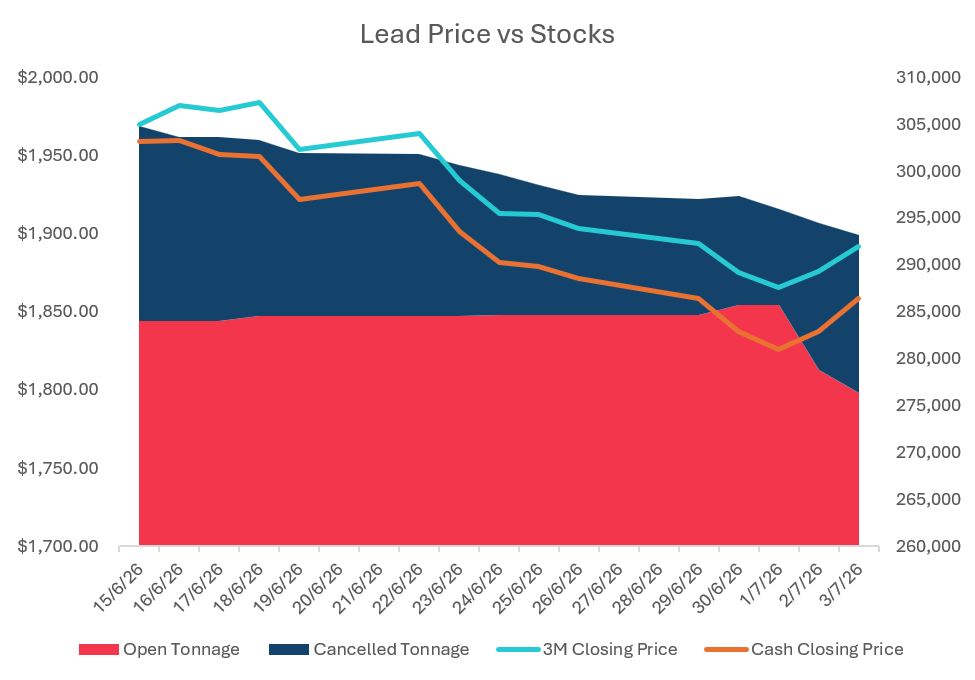

While recovering slightly toward the end of the week, lead continued to look weak as its momentum is still downward. Lead is behaving more defensively than the rest of the complex with limited speculative interest and little evidence of a compelling demand story.

Limited pressure on stocks is also giving way to a healthy cash-3s contango that has settled above $30C for the last 3 weeks. While cancelled tons increased, this was not enough to impact the broader story. With the $1900 handle giving way, lead is hitting lows not seen since March of this year and will likely need to reclaim this level in order to prevent further selling. The downside risk remains a break below the mid-$1,800s support area.

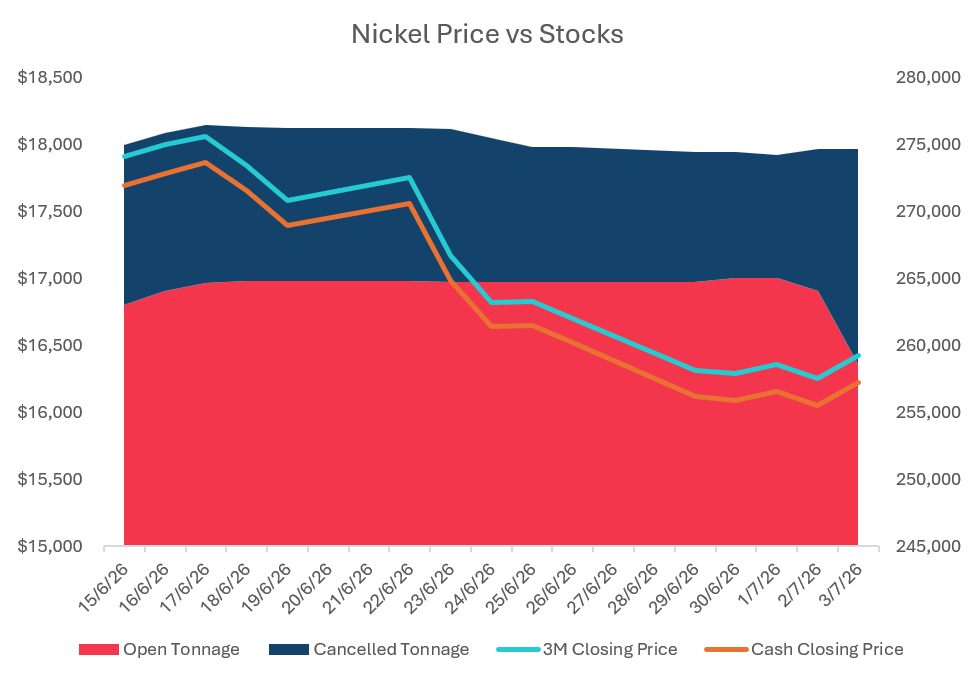

While nickel managed a modest gain from where we opened the week, it still looks heavy relative to the rest of the complex. The price recovered from the lows seen earlier in the week but we are close to testing $16,000, a close below which could trigger more technical selling.

Indonesia remains the key driver. Earlier quota cuts helped take nickel to multi-year highs, but growing speculation that Jakarta could loosen or revise 2026 mining allowances has capped the market. With exchange inventories still elevated and a healthy cash-3s contango, the market has not shown any evidence of physical tightening. A short-covering bounce is possible if Indonesian policy disappoints the bears but any sustained rally likely requires clearer evidence that surplus metal is being absorbed.

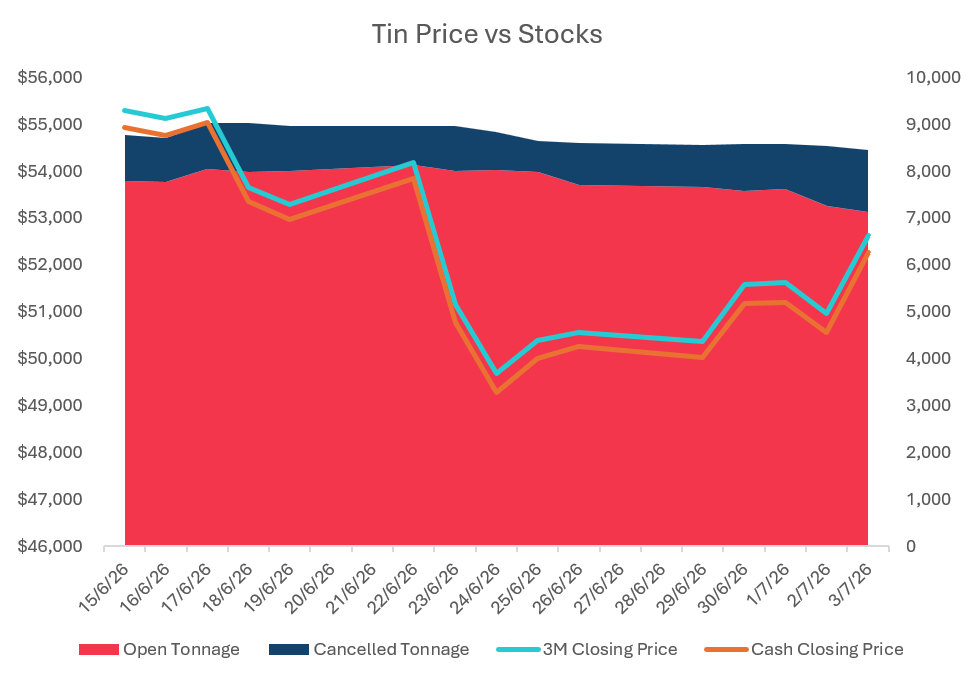

Tin was the strongest metal of the week, rising more than 4% from Monday’s open and closing at the weekly high. The recent volatility in tin seemingly working in both directions as the market rewards tin when macro sentiment stabilizes.

Tin will likely remain volatile and with low LME stocks impacting flat price and spreads far less than the other metals in the complex, tin is being led more by long-term scarcity and strategic demand than nearby tightness.

Holding the $50k handle this week was important – a sustained move above $52k would put the prior highs back into focus where closes below $50k bring downside risk of testing $47k.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Hydro's Slovalco aluminium plant in Slovakia has agreed terms with the Slovak government to restart 75,000 tonnes of primary aluminium production capacity, with output expected to begin in the fourth quarter of 2026.

Alcoa Corporation has agreed to acquire South32's entire aluminium value chain for an implied enterprise value of up to $5.6 billion in a deal that represents one of the largest consolidations in the global aluminium industry in years.