The LME Weekly Review: 15-19 June 2026 - Spotlight on Aluminium

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

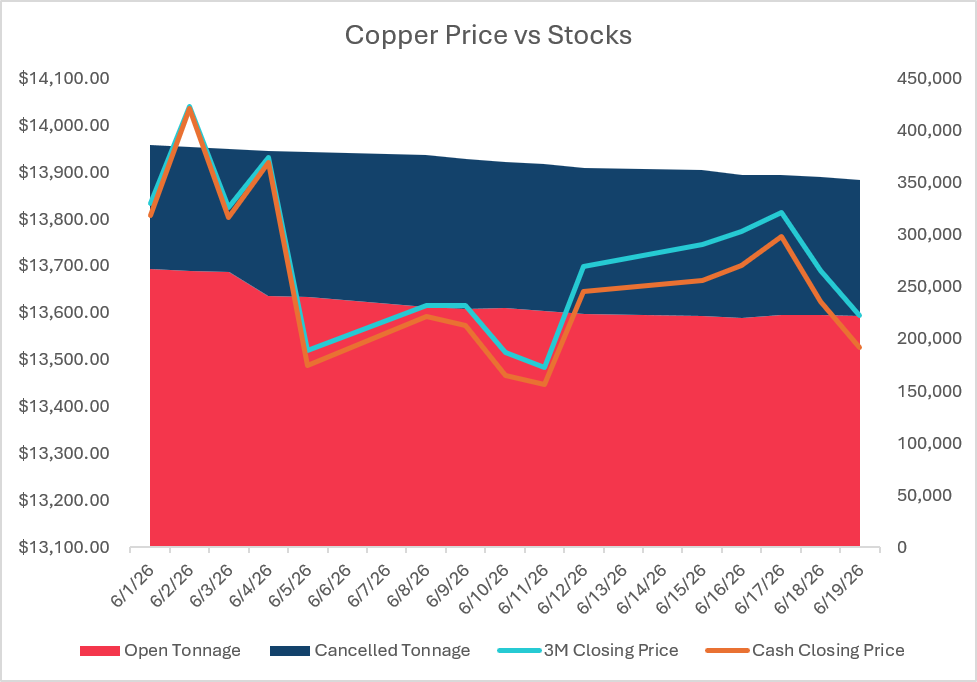

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory. Metals prices initially took their lead from oil which sold off following a preliminary US-Iran memorandum of understanding aimed at reopening the Strait of Hormuz and creating a 60-day window for negotiations. Whether that de-escalation holds remains uncertain, with shipping flows through the Strait still vulnerable to renewed disruption.

Further to that, new Fed Chair Kevin Warsh gave his inaugural news conference on Wednesday where, aside from questioning the traditional figures the Fed has used to make decisions, he recommitted to the long-term 2% target for inflation. Those expecting a strongly dovish Fed shift may be disappointed as half of the 19 FOMC participants expect interest rate rises before the end of 2026. LME metals (which are priced in USD) have historically benefited from lower US interest rates (and conversely weaker USD) so this also took some steam out of the recent rallies.

Last week we put copper under the spotlight given its global importance and overall barometer of economic health. This week we look at aluminium – which on a global scale is actually the most widely consumed non-ferrous metal and one of the clearest examples of how energy, logistics, trade policy and physical premiums can matter just as much as the LME flat price.

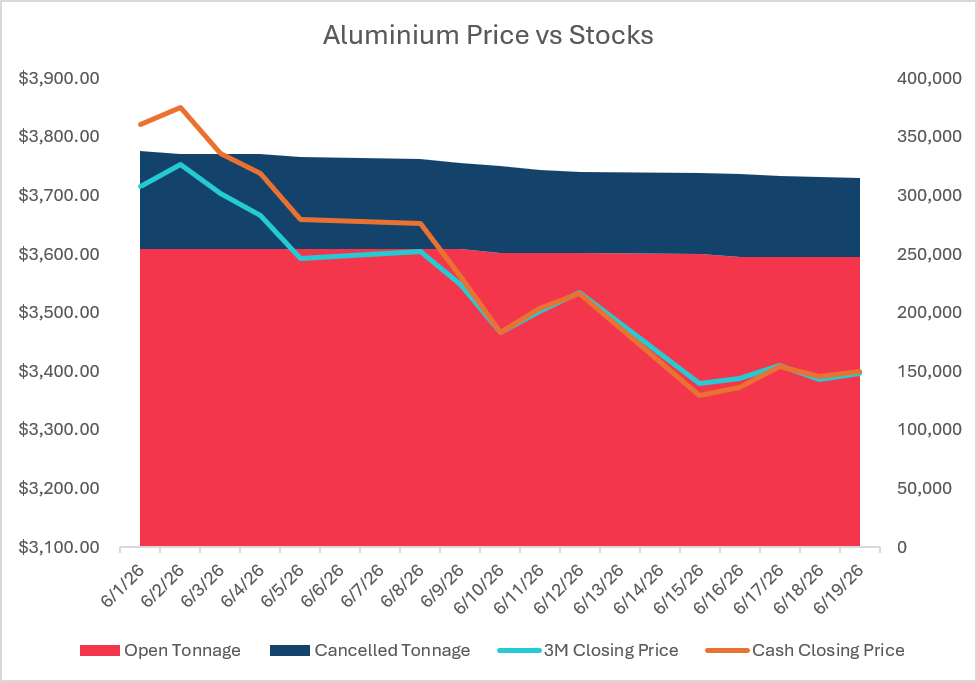

Weekly Open: $3,379.50 | Weekly High: $3,410.50 | Weekly Low: $3,379.50 | Last: $3,396.50

Cash – 3’s: $3.5b

Stock: 315,300mt (-4,625mt) | Cancelled Tons: 67,725mt (-1,675mt)

Weekly Open: $13,745 | Weekly High: $13,814.50 | Weekly Low: $13,595 | Last: $13,595

Cash – 3’s: $68.5c

Stock: 352,150mt (-11,950mt) | Cancelled Tons: 129,850mt (-10,475mt)

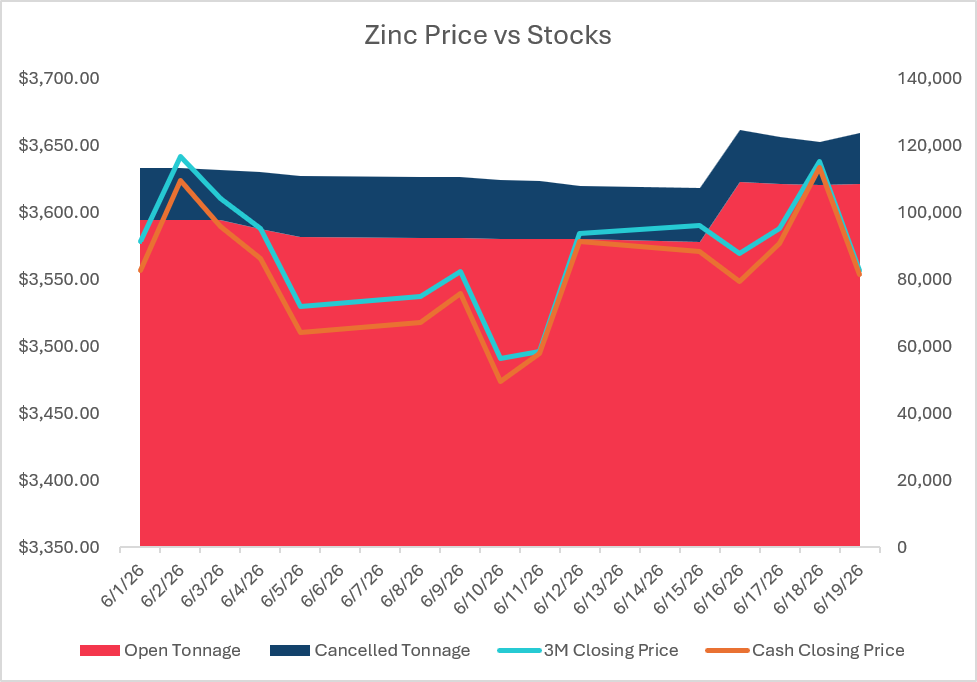

Weekly Open: $3,590 | Weekly High: $3,638 | Weekly Low: $3,556.50 | Last: $3,556.50

Cash – 3’s: $3c

Stock: 123,775mt (+16,025mt) | Cancelled Tons: 15,325mt (-525mt)

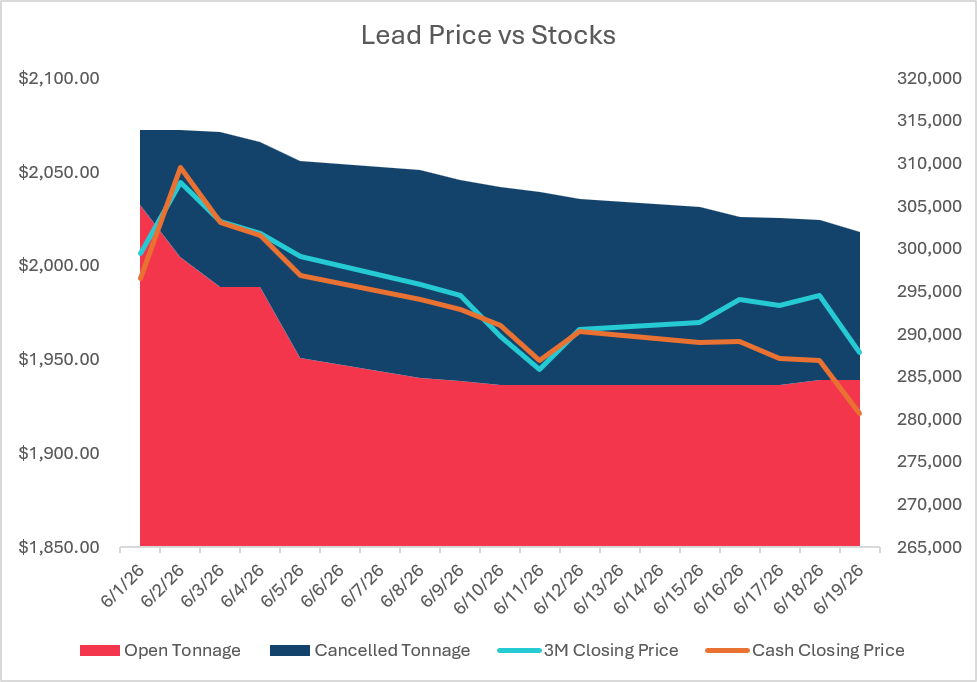

Weekly Open: $1,970 | Weekly High: $1,984 | Weekly Low: $1,954 | Last: $1,954

Cash – 3’s: $32.5c

Stock: 301,950mt (-3,925mt) | Cancelled Tons: 17,400mt (-4,425mt)

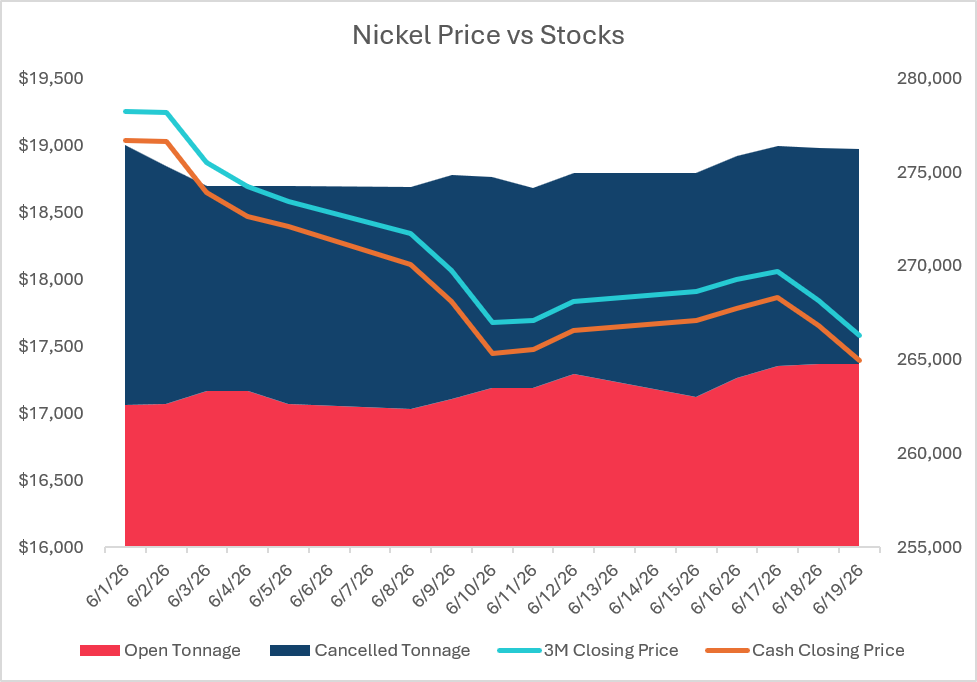

Weekly Open: $17,911 | Weekly High: $18,060 | Weekly Low: $17,580 | Last: $17,580

Cash – 3’s: $185c

Stock: 276,216mt (+1,278mt) | Cancelled Tons: 11,460mt (+768mt)

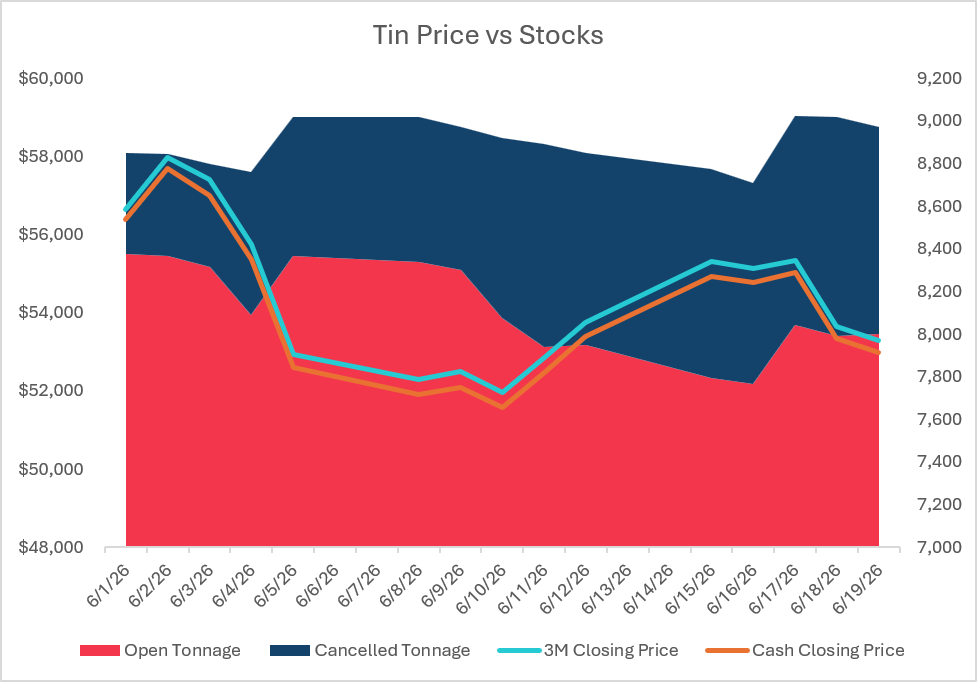

Weekly Open: $55,301 | Weekly High: $55,344 | Weekly Low: $53,293 | Last: $53,293

Cash – 3’s: $319c

Stock: 8,970mt (+120mt) | Cancelled Tons: 970mt (+70mt)

Aluminium does not get the same macro metal reputation as copper, but it sits at the center of modern industry. Compared to an annual consumption of ~29 million tons of refined copper, refined aluminium consumption exceeds 75 million tons globally each year.

It is light, corrosion resistant, highly recyclable, and conductive enough to be used across transport, packaging, construction, power infrastructure, consumer goods, and machinery. That breadth of demand means aluminium is exposed to both cyclical manufacturing trends and long-term themes such as electrification, lightweight vehicles, renewables, grid buildout, and energy-efficient construction.

It is also why the current Middle East disruption matters. Around 9% of global refined aluminium production flows out of the Strait of Hormuz so any disruption to this critical waterway not only impacts energy prices but has a drastic impact on the supply of Aluminium. This tends to show up first in rising premiums, increases in cancelled LME warrants, and volatility in the flat price.

Aluminium is produced by mining bauxite, which is refined into alumina, then further smelted into primary aluminium through an extremely electricity-intensive process. Even without the recent disruption to shipping routes, we have seen global curtailments as increases in energy costs have made refined aluminium production unprofitable.

While not as widely traded by the speculative community as copper, there is still a large contingent of speculative traders that take positions in the aluminium market. Because of this we can see both spreads, and flat price react violently on short-term signals that may not reflect longer-term fundamentals.

China dominates production and consumption of aluminum globally. They produce ~60% of all refined aluminium and make up ~62% of global consumption. Other major production points are India (6%) , Russia (5%), Canada (4.5%) and the Middle East (9%). Despite consuming ~5 million tons of primary aluminum each year, the US struggles to produce aluminium due to high electricity costs, producing less than 1% of global aluminium. This has placed the US in the precarious position where imports of this critical metal are vital, but recent tariffs have increased import costs dramatically without increasing domestic production.

You cannot discuss aluminium without talking about premiums. Unlike other base metal markets where premiums are relatively stable and largely booked on long-term basis, aluminium premiums can be extremely volatile. They are also hedgeable through swap contracts, allowing producers, traders, and consumers to take physical and speculative positions on the premium. The three main markets for aluminium premiums outside of China are CIF Japanese main ports, Delivered Duty Paid Midwest USA, and in-warehouse duty paid Rotterdam. These premiums have been impacted not only by power costs and shipping chokepoints, but export restrictions, tariff changes, warehouse drawdowns, and trader positioning. The result of this can be a market where premiums move before, and sometimes by larger amounts than the LME flat price. For example, the current US Midwest premium is over $2,200/mt – nearly 65% of the LME aluminium price.

Key signals to watch on aluminium are physical premiums, drawdowns on LME stocks should the situation in the Middle East deteriorate, alumina availability, power cots, and whether buyers in Europe and the United States continue to compete for replacement units. A sustained disruption would be more bullish if it tightens ex-China availability and forces consumers to pay up for prompt metal. In this case we would likely see a return to backwardated cash-3s spreads that have recently eased on the hopes for a resolution. Further de-escalation would reduce the immediate risk premium, but it would not remove the lessons from this episode – that aluminum supply is increasingly exposed to energy security, regional trade policy, and logistics chokepoints.

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

Protesters blocked a transport route serving Rio Tinto's Oyu Tolgoi mine in Mongolia, disrupting copper concentrate exports and prompting warnings of economic losses.

Argentina has approved the Vicuna copper project - a joint venture between Australia's BHP and Canada's Lundin Mining - in what Economy Minister Luis Caputo called the largest mining project in Argentina's history.

Stay connected with our latest developments. Share your details to receive updates and analyses from LME Insight.