Oyu Tolgoi Copper Exports Resume After Protest Disruption in Mongolia

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

Protesters blocked a transport route serving Rio Tinto's Oyu Tolgoi mine in Mongolia, disrupting copper concentrate exports and prompting warnings of economic losses.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

The numbers looked extraordinary. Aluminium Bahrain closed 2025 with a net profit of $582 million, up 18.5% year-on-year, capped by a fourth quarter that delivered $289 million alone, a 193% surge on the same period in 2024 and the highest quarterly result in the company’s history.

QAMCO, the Qatari holding vehicle for the Qatalum joint venture, posted a 25% profit increase to QR768 million ($210.99 million). Gulf smelters, running on long-term gas contracts at costs European producers could only watch from the sidelines, had quietly become the most profitable primary aluminium operators in the world. The LME cash price that underpinned those results averaged $3,104/mt in the weeks before the conflict began, with the market in contango: a standard structure for a well-supplied commodity.

When February 2026 arrived, the architecture of that profitability was exposed.

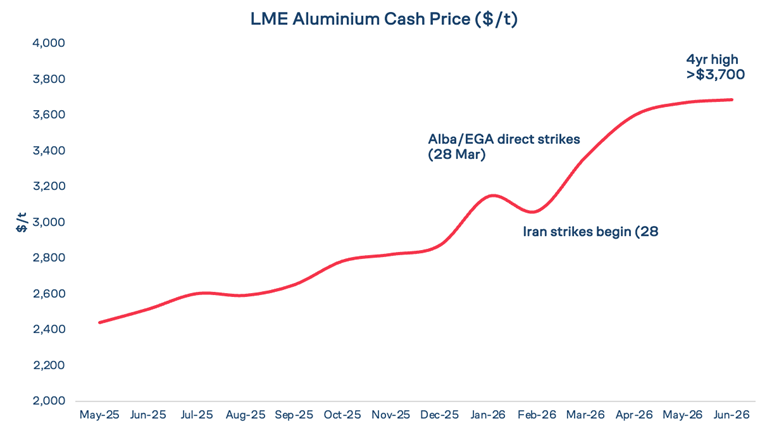

The conflict that began with US and Israeli strikes on Iran on February 28 moved faster than the market had modelled. Within days, the Strait of Hormuz was effectively closed. The Gulf, which accounts for roughly 8% of global primary aluminium supply, ships nearly all of its production through that single corridor. Alba declared force majeure on deliveries and cut 19% of its 1.62 million tonne annual capacity by mid-March. Qatalum dropped to 60% nameplate capacity after QatarEnergy suspended gas supply. On March 28, Iranian missiles struck both the Alba smelter and EGA’s Al Taweelah facility, with both declaring force majeure. Full restoration at EGA could take up to 12 months.

LME three-month aluminium surged to a four-year high above $3,700/mt by early June, a 25% rise from the days the first missiles flew. Potential Gulf output losses for 2026 have been estimated at 3.5 million tonnes.

Outside the conflict zone, the story was different. Rio Tinto’s aluminium segment delivered underlying EBITDA of $4.4 billion in 2025, up 29%, on production of 3.38 million tonnes. South32 posted underlying earnings up 75%. Neither carries meaningful Hormuz exposure. Their more complex, multi-continent cost structures – once the source of competitive disadvantage against lean Gulf operators – now look like resilience premiums.

The piece of the picture that has received less attention is what happens as the conflict moves toward resolution. The preliminary ceasefire agreement signed on June 15 ends the acute phase of disruption and ties the Strait’s reopening to the deal sticking. It does not end the structural questions the conflict exposed.

The 2025 profit surge at Alba and Qatalum was not purely operational. It was built on an LME price environment averaging $2,873/mt across the 12 months May 2025 to April 2026, elevated partly by the same regional tensions that then caused direct physical damage. The cash-to-three-month spread peaked at $104/mt on June 1, signalling acute physical tightness across the market. By June 11, that spread had collapsed to $6/mt. The $343/mt fall in the cash price over the same nine trading days tells the same story: the market began pricing the ceasefire before it was signed. Gulf smelters will begin the slow, expensive process of restarting curtailed capacity into a market where the unwind is already underway. Restart costs are real: bringing potlines back online from cold takes six to twelve months and carries significant capital and energy costs. The 193% increase in Q4 profit that made headlines will not be the baseline from which recovery is measured.

China’s position adds another constraint on the upside. Chinese aluminium production has been boosted in recent months and is ever-present in global markets. Full-year 2025 output reached 45.02 million tonnes, technically breaching the government’s self-imposed capacity cap. Strong continued growth in Chinese production is unlikely, given tighter energy, environmental and carbon policies. The cap provided a structural floor under global prices independent of Gulf disruption. That floor remains, but it is not infinitely supportive. Chinese producers, unaffected by Hormuz, operating at near-capacity utilisation and benefitting from a wider LME-SHFE aluminium spread since the war are the natural beneficiaries of any sustained price elevation that Gulf disruption creates.

The question the market is beginning to ask is one Gulf producers have not previously had to answer: how much of the cost advantage that drove record 2025 profitability was contingent on conditions – stable gas supply, open shipping lanes, functioning regional infrastructure – that can no longer be assumed? The Hormuz chokepoint was always an implicit hypothetical in the Gulf model. It is now explicitly priced.

The June 15 agreement to end the US-Iran war is preliminary. A 60-day window for more substantial negotiations follows, and analysts are sceptical that a final settlement can be reached on that timetable. But the market has already moved. Roughly half the $746/mt conflict premium built into LME cash prices since the war began remains embedded in the aluminium price today, and market participants may become more confident in a possible conclusion to hostilities.

As the Strait reopens and curtailed capacity returns, that residual unwinds too. Gulf smelters may face a tighter spread between their rebuilt cost base and an LME price that no longer reflects an acute supply shock.

The same regional tensions that inflated Gulf profits in 2025 then threatened the infrastructure that earned them. The ceasefire resolves the second part for now. It does not undo the first.

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

Protesters blocked a transport route serving Rio Tinto's Oyu Tolgoi mine in Mongolia, disrupting copper concentrate exports and prompting warnings of economic losses.

Argentina has approved the Vicuna copper project - a joint venture between Australia's BHP and Canada's Lundin Mining - in what Economy Minister Luis Caputo called the largest mining project in Argentina's history.

There was a split tone on LME base metals this week with copper, zinc, and tin finishing higher week-on-week, while aluminium, lead, and nickel all closed lower.

Stay connected with our latest developments. Share your details to receive updates and analyses from LME Insight.