Qatar Aluminium Manufacturing Company (QAMCO), which holds a 50% stake in Qatalum, confirmed on Sunday June 14 that the marketing and offtake arrangements with Hydro Aluminium AS, Qatalum's marketing agent, have been terminated.

Export restrictions and carbon pricing are reshaping who can access European aluminium scrap. Domestic remelters are gaining ground that they previously ceded to Asian buyers. But contamination means the discount on secondary metal can only close so far.

LME Aluminium cash prices slid to three-week lows and settled at $3,498.50/t on Thursday 11 June 2026, down sharply from the four-year high of $3,795.50/t reached just ten days earlier on Monday 1 June 2026.

The market has moved in two phases:

Phase one: visible stocks rose and prices fell.

Phase two: available stocks tightened and prices recovered.

Copper did not fall because demand disappeared. It fell because inventories rose. It recovered because available metal still looked scarce.

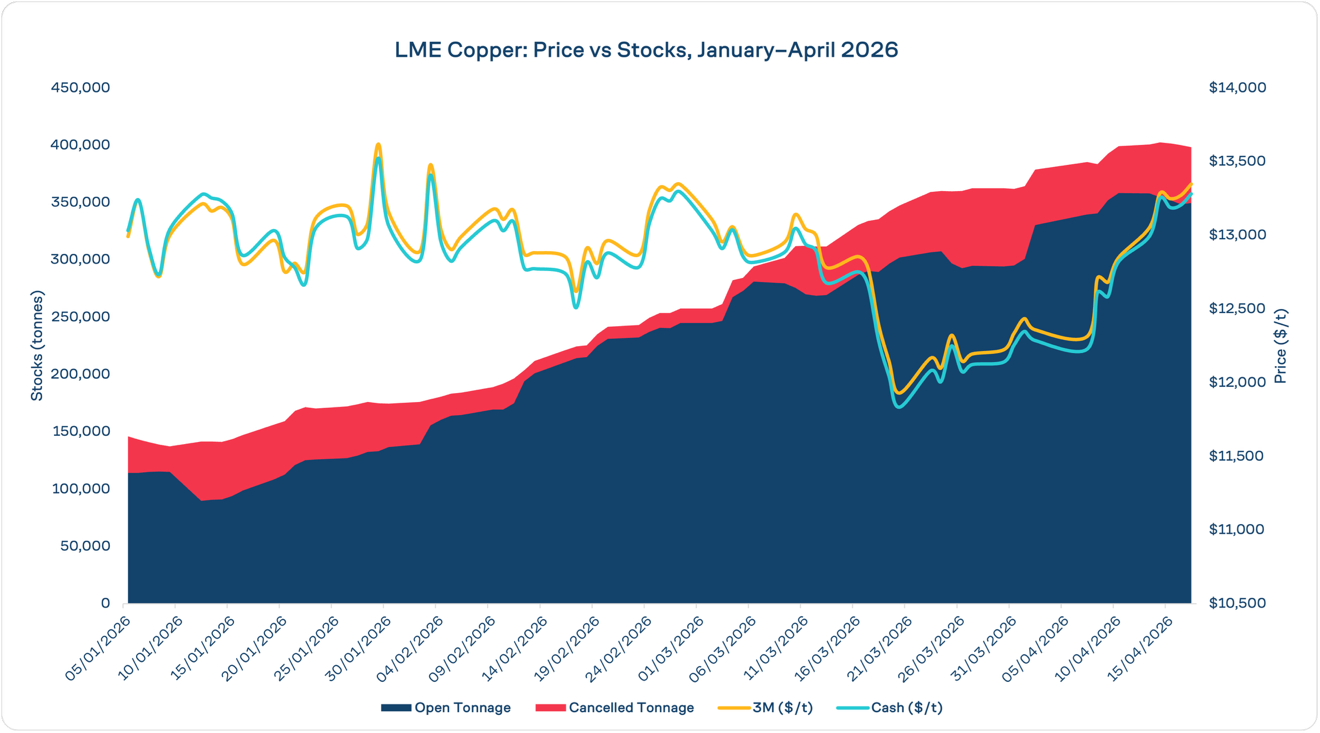

LME copper inventories have surged since late February. Prices have gone nowhere.

Exchange stocks rose from 257,675 tonnes on 27 February to 398,425 tonnes by 17 April, a gain of 140,750 tonnes, or 55% in seven weeks. Normally, that sort of warehouse build would be enough to cool a hot market. More metal in LME sheds should mean better nearby availability, weaker prompt premiums and less incentive to chase spot units.

The market initially responded in textbook fashion. LME cash copper fell from $13,294 per tonne on 27 February to its lowest since the beginning of 2026 to $11,834 on 20 March, an 11% correction as fresh tonnage punctured the scarcity narrative that had propelled prices to record highs.

The sell-off did not last. By 17 April, cash copper had recovered to $13,281 per tonne, just $13 below its pre-war level.

The reason lies in the fine print of the warehouse data.

Stocks up, cancellations up faster

While headline inventories were rising, so too was the amount of metal being earmarked for physical withdrawal. Cancelled warrants climbed from 12,775 tonnes on February 27 to 48,775 tonnes by 17 April.

That is an increase of 36,000 tonnes, or 282%. The cancelled ratio rose from 5.0% of total stocks to 12.2%.

Cancelled metal is no longer freely available to the market. It has effectively been booked for load-out by a consumer, merchant or trader.

So, while more copper was entering the exchange system, a growing share of it was simultaneously leaving the pool of available supply.

What looked like abundance was at least partly transit metal.

The market saw through it

Copper is unusually sensitive to deliverable units.

It is not total inventory that matters most, but inventory that can actually be bought today.

That helps explain the swift price recovery. Traders appear to have concluded the stock build was temporary rather than structural.

Fresh units had arrived in warehouses, but they were not sitting idle. They were already being claimed.

The visible surplus was smaller than the headline number suggested.

War risk changes buyer behaviour

The timing is unlikely to be coincidence.

The U.S.-Iran war injected a fresh layer of logistical risk into global metals supply chains.

Any threat to Gulf shipping routes, insurance cover, freight schedules or port reliability changes procurement behaviour.

For copper consumers running lean inventories, the safest response is often to secure nearby cathode rather than wait for cargoes at sea.

LME warehouse metal becomes optionality. A cancelled warrant is effectively insurance against delayed shipments, disrupted freight or worsening geopolitics.

That would help explain why cancellations rose even as inventories swelled. Buyers were not ignoring the incoming metal. They were taking it.

Another hidden risk: sulfur

There is a second transmission channel.

Copper production depends heavily on sulfur and sulfuric acid, both critical to leaching operations and refining flows.

Any disruption to Middle East sulfur trade can create concern over feedstock costs and availability elsewhere. And the possibility of tighter sulfur markets may also encourage precautionary buying of refined copper, reflecting concerns over potential constraints on future production rather than immediate cathode availability.

What the numbers really say

A 55% increase in LME stocks would normally be enough to engineer a sustained downward repricing.

This time it produced only a brief correction.

Once cancellations accelerated, prices recovered almost fully.

That suggests the copper market remains structurally uneasy about supply.

Large inventories can coexist with tight conditions if much of the metal is tied up, already committed to consumers, or located in regions where it is not readily accessible to demand. This geographic mismatch is often overlooked when headline inventory levels are rising. At the same time, movements in other exchange inventories (COMEX, SHFE) can have an influence on price signals and perceived market tightness.

That appears to be the case now.

LME copper CA data: LMElive official reports, 17 April and 21 April 2026. Stock summary report dates 17 April and 20 April respectively. China output data: National Bureau of Statistics via Bloomberg, 21 April 2026. Sulfuric acid income reference: Yang Changhua, Beijing Antaike Information Co., cited in Bloomberg. Seasonal output guidance: Shanghai Metals Market.

Qatar Aluminium Manufacturing Company (QAMCO), which holds a 50% stake in Qatalum, confirmed on Sunday June 14 that the marketing and offtake arrangements with Hydro Aluminium AS, Qatalum's marketing agent, have been terminated.

Export restrictions and carbon pricing are reshaping who can access European aluminium scrap. Domestic remelters are gaining ground that they previously ceded to Asian buyers. But contamination means the discount on secondary metal can only close so far.

LME Aluminium cash prices slid to three-week lows and settled at $3,498.50/t on Thursday 11 June 2026, down sharply from the four-year high of $3,795.50/t reached just ten days earlier on Monday 1 June 2026.