LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

The aluminium market isn’t short. It’s scared. 3m tonnes of Middle East smelting capacity is offline, and buyers are watching supply, not price. Orders pulled forward, inventories rebuilt, supply routes reopened. This isn’t a spike. It’s a shift from price discovery to availability management.

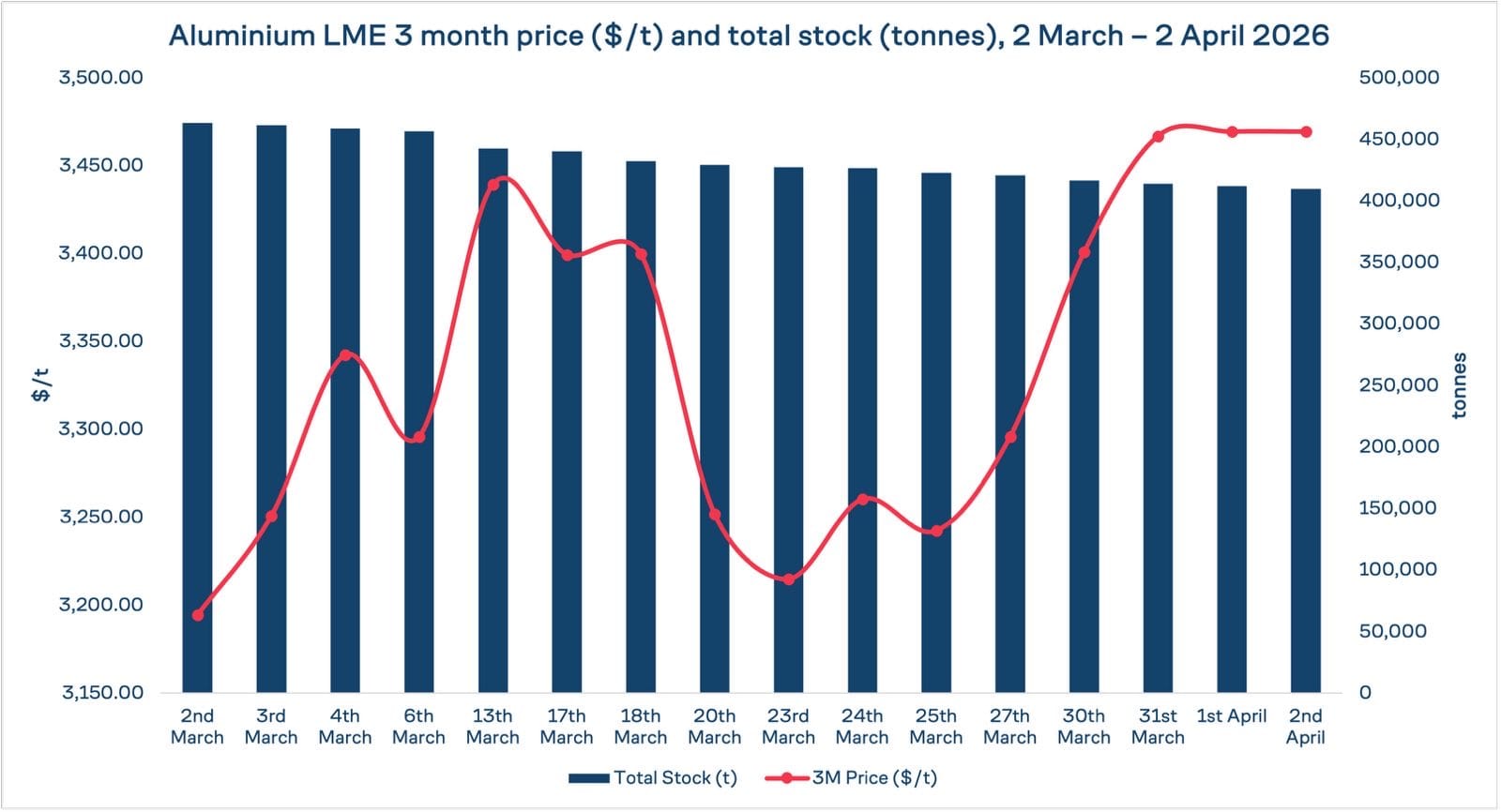

LME three-month aluminium rallied $235.50 over four sessions, from $3,296 on March 27 to $3,531.50 by 01 April 2026, before pulling back to $3,469.50 on 02 April 2026. The cash price has tracked higher: $3,504.50/3,505 as of Wednesday [01 April 2026].

But the more telling signal is what is happening in the physical market. Carmakers are building contingency stocks (Carmakers rush to secure aluminium as Middle East war hits supply – FT 24 Mar 2026). Procurement teams are drawing down inventories, pulling forward orders and, in some cases, reopening supply routes they had previously closed. The shift is not driven by a shortage that exists today. It is driven by fear of one that is coming.

That distinction matters. It changes what the market is doing and how much further it has to run.

The trigger is the weekend strikes on EGA's Al Taweelah smelter. When potlines go into uncontrolled shutdown, metal solidifies in the smelting circuits. That is not a switch-off-switch-on situation.To resume operations at the 1.6 million tonnes smelter, EGA must repair infrastructure damage and progressively restore each of the reduction cells. Early indications are that a complete restoration of primary aluminium production could take up to 12 months (Update on EGA’s Al Taweelah site – EGA 03 April 2026).

The deeper problem is upstream. EGA can produce some alumina domestically, but both Al Taweelah and the Dubai smelter rely on imported cargoes transiting the Strait of Hormuz. The fact that EGA has already been selling alumina volumes into the market post-strike suggests the operational picture is deteriorating faster than official statements indicate.

The physical market responds to this kind of structural uncertainty by front-loading.

Buyers are not responding to current scarcity. They are responding to the risk of future unavailability. Orders that would have been placed in Q3 are being placed now. Inventory that would have been drawn down is being rebuilt. The result is a tightening of the prompt market that has nothing to do with underlying supply and everything to do with procurement behaviour.

Regional premiums have moved sharply and held their gains. This is the physical market's regional price signal, and it is more instructive than the LME benchmark. The benchmark reflects global balance. The premium reflects local availability, in the right specification, now. When premiums detach from the benchmark and stay detached, it means tightness is localised.

LME aluminium stocks fell 51,650 tonnes between 03 March 2026 and 02 April 2026. But the more telling number is cancelled warrants, which dropped from 375,525 to 269,000 tonnes. Cancelled warrants represent metal queued for physical delivery. That queue has shortened sharply. Less aluminium is being pulled from the system than the headline stock draw suggests. The immediate supply pressure has eased. Whether that reflects demand softening, logistics shifting, or simply a pause before the next wave of cancellations is the question the market is now asking.

Scrap usage is rising. Inventories are being treated as strategic assets rather than working stock. These are not the behaviours of a market managing a temporary disruption. They are the behaviours of a market that has concluded the disruption is structural.

The producer response tells a clearer story, and equity markets corroborate it: Alcoa and Century Aluminum were both up more than 7% earlier in the week, pricing in the same margin and volume expectations. When producers re-rate that sharply, they are signalling a sustained supply deficit, not a spike that gets sold.

The precedent is instructive. During the European energy crisis of 2022, smelter curtailments removed flexible supply. Consumers extended contract cover, built inventories, and pushed premiums sharply higher. The cost of securing certainty exceeded the spot cost of metal. That is the condition the market has now returned to, except the supply shock this time is harder to reverse. Energy costs can normalise. Battle-damaged potlines cannot restart on a spreadsheet.

China used to absorb this kind of shock with increased production. That buffer is gone. Beijing's capacity cap means the usual release valve is closed.

High inventories, spare smelting capacity, and predictable trade flows once provided the optionality to redirect metal when one region tightened. Those buffers are weaker now. Energy costs have eroded flexible capacity in Europe. Trade flows are more constrained after years of protectionism. And automotive supply chains are specification-driven: alternative sources cannot be qualified at speed.

There is a feedback problem embedded in all of this.

Defensive procurement is rational at the individual level. A carmaker that fails to secure aluminium risks shutting production within months. But the collective behaviour amplifies the very tightness each buyer is trying to hedge. Premiums inflate faster. Logistics seize up.

The distinction between real shortage and scarcity hedging will not become clear until the buying wave passes. Demand destruction and substitution are risks that build over time; they are not what is driving the market today. In the meantime, the premium layer has developed effective price inelasticity. Buyers need the metal, in spec, on time. The price is secondary.

What is clear is the direction. Availability has become as important a consideration as price in procurement decisions. The disruption in the Strait of Hormuz has not just tightened supply. It has changed how buyers think about sourcing. Certainty of access now carries a premium that price alone did not previously need to reflect.

The EGA strikes did not create that condition. They confirmed it.

LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.