Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

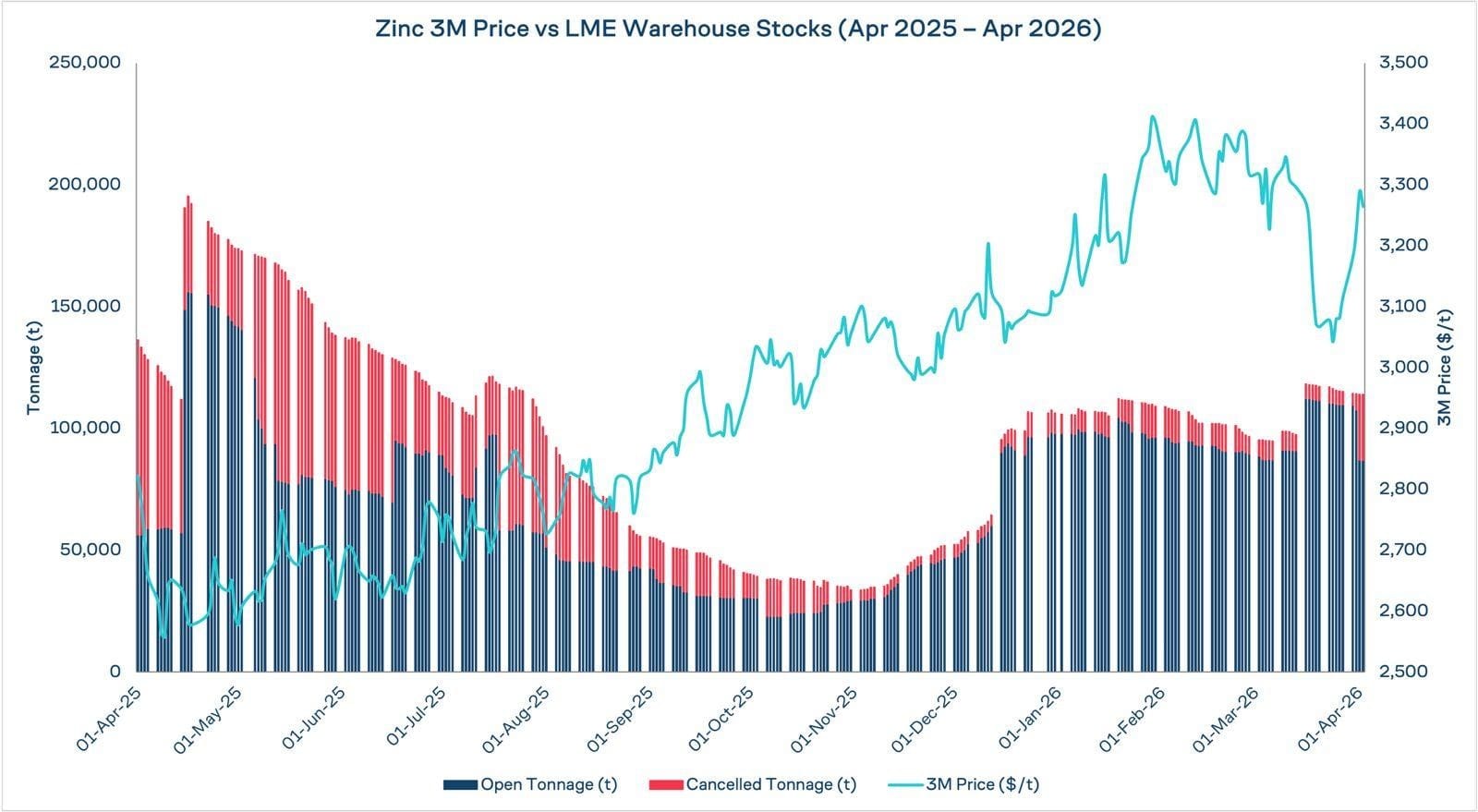

Zinc sent mixed signals in March: a big warehouse build and price dip looked bearish, but the market absorbed it fast. The real issue is structural – mine supply is rising faster than refining capacity, with smelter constraints and demand uncertainty capping prices for years.

So far in 2026, zinc has been caught between improving mined supply and constrained refining capacity, with weak and uneven demand preventing a decisive price move in either direction. Rising treatment charges signal a looser mined market. Smelter bottlenecks and patchy demand are keeping refined metal availability tight enough to prevent a clean price correction. The result is range-bound prices, persistent volatility, and a market that is sending signals that require careful reading.

March was a case in point.

Zinc was drawing steadily through the first week of the month. LME stocks fell from 96,775 tonnes at the end of February to 94,800 tonnes by 6 March 2026: a quiet, consistent drain. A Western market that is still running short of refined metal.

Then the signal broke.

On 9 March 2026, stocks jumped by 4,150 tonnes. A week later, on 16 March 2026, zinc warehouse stocks had surged by a further 20,875 tonnes in a single session. Total stocks hit 118,375 tonnes. The three-month price, which had been trading above $3,300, fell to just above $3,060 by 20 March 2026.

Reading that move as innately bearish required ignoring rather a lot.

Western smelters have not been running the refined zinc pipeline to delivery points at full capacity for some time. A large inflow arriving into that context fits the pattern precisely.

The price trough on 20 March 2026 came three days after stocks peaked. What followed was not a continuation of the bearish move.

From 118,375 tonnes on 17 March 2026, stocks have drawn consistently: to 115,275 by 27 March 2026, falling further to 112,325 by 8 April 2026. The 8 April 2026 draw alone was 1,600 tonnes, the largest single-session decline in the post-surge sequence. The three-month price has recovered from its $3,060 trough to $3,292.50. The draw rate is accelerating.

That pattern reflects something the headline stock figure obscures. LME zinc inventory is not evenly distributed. On-warrant levels reflect a structurally uneven split between Asia and Europe, and that regional dislocation is what periodically lifts nearby spreads into backwardation and supports elevated physical premiums in supply-constrained locations. Headline global balance figures do not capture the granular reality of where metal sits and who can access it. Availability, not just supply, is what prices the nearby market.

Upstream, the picture looks different, and in some respects more bearish.

Rising spot treatment charges (TC) are sending an unambiguous signal: the mined zinc market is loosening. After years of disruptions and curtailments between 2022 and 2024, concentrate availability has recovered. Smelters are regaining negotiating leverage. Boliden's Tara mine in Ireland has restarted. Ivanhoe's Kipushi project in the DRC is ramping up. The mined supply recovery that analysts have been forecasting is broadly on schedule, and the market is expected to move into modest surplus this year.

The refining bottleneck

Mined supply and smelter output are different parts of the chain. That distinction matters more than it might appear.

Smelter capacity in both China and Europe remains constrained, preventing upstream feedstock gains from fully translating into refined metal supply. Concentrate from a restarted mine in Ireland or a ramping project in the DRC still needs to be processed before it can reach consumers or LME warrant stocks. More ore does not mean more metal. Yet.

The TC signal is the classic early-cycle pattern. Mine markets turn first. Metal follows. The lag is a countdown, but it has not yet expired.

On the demand side, there is little to accelerate it. China's property sector remains zinc's most significant vulnerability. Demand from galvanised steel, which accounts for roughly half of all zinc consumption, has been stop-start, held back by a construction sector that has yet to find a sustainable floor. There is no broad-based recovery underway. There is cautious, uneven buying, heavily contingent on policy signals and project pipelines that remain uncertain. Until China builds again with conviction, sustained price rallies will remain difficult to justify on fundamentals alone.

In Europe, energy costs are keeping smelter margins fragile and the threat of further curtailments very much alive. That structural vulnerability functions as a price floor. When demand weakens and prices soften, uneconomic smelters pull back, tightening refined supply and limiting the downside. It is not a bullish argument. It is a meaningful constraint on how far prices can fall.

The macro backdrop is not helping. A strong dollar and persistently elevated interest rates are weighing on base metals as an asset class, constraining investment flows, raising the cost of carry, and dampening the speculative appetite that can amplify moves in either direction. Until that environment shifts, whether through rate cuts, dollar weakness, or a genuine uptick in risk appetite, the ceiling on price rallies will remain lower than the underlying structural picture might otherwise support.

Korea Zinc's launch this week of Project Crucible, a $7.4 billion integrated smelter in Clarksville, Tennessee, with production not expected until 2029, is a signal of where the market thinks the structural gap lies, and precisely how long it will take to close it.

The March warehouse surge looked like a resolution. The draw that followed suggests the Western market absorbed it and came back for more. Spread and cancelled warrant data will show whether the surplus forming upstream can reach LME delivery points fast enough to change.

Cancelled warrants tend to move before the price does.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Hydro's Slovalco aluminium plant in Slovakia has agreed terms with the Slovak government to restart 75,000 tonnes of primary aluminium production capacity, with output expected to begin in the fourth quarter of 2026.