China’s May copper imports show mixed trend as unwrought volumes decline

May brought a modest increase in China’s copper concentrate imports, but unwrought copper volumes continued to lag last year’s pace.

May brought a modest increase in China’s copper concentrate imports, but unwrought copper volumes continued to lag last year’s pace.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 5 June 2026.

London Metal Exchange copper stocks remain near their highest levels since 2013, but available metal is tightening as cancellations rise.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 5 June 2026.

After a constructive start to the week with several metals making new short-term highs on Monday and Tuesday the complex sold off hard on Friday leaving aluminium, copper, nickel, and tin all lower week-on-week.

The main macro theme was the collision between resilient US economic data, a firm rates backdrop, and still-uncertain demand signals from China. Friday’s US employment report showed payrolls increasing by 172,000 in May (vs. 85,000 expected) and unemployment holding at 4.3%. This reduced the near-term case for the Federal Reserve to ease rates, and led to markets pricing fewer cuts in 2026. All of these factors were supportive of the US Dollar.

Because LME metals are priced in US Dollar, any appreciation in USD vs EUR, GBP, JPY, and other major currencies tends to weigh on demand for metals. A stronger dollar makes those metals comparatively more expensive in non-USD currencies. For example, using a EUR/USD rate of 1.15, copper at $13,000/mt equates to EUR 11,275/mt. If the rate changes to 1.13, that same copper at $13,000/mt now equates to EUR 11,504/mt – a EUR 229/mt increase without a change in the LME price for copper.

With macroeconomic, geopolitical, and commodity-specific factors all pulling prices in different directions, short-term forecasting remains exceptionally difficult. We can however expect volatility to remain elevated across the base metals complex for the foreseeable future.

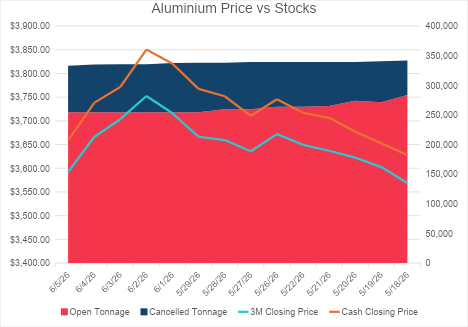

Weekly Open: $3,716 | Weekly High: $3,752.50 | Weekly Low: $3,592 | Last: $3,592

Cash – 3’s: $66.5b

Stock: 333,200mt (-4,800mt) | Cancelled Tons: 78,575mt (-4,800mt)

Aluminium finished $74.50/mt lower week-on-week after failing to hold the highs seen at the beginning of the week. 3M briefly pushed above $3,750/mt on Tuesday but closed the week at the low, with the price still sensitive to macro pressure when there is a lack of escalation in the supply story.

Stocks fell by nearly 5KMT as metal continues to move out of the exchange warehouse system. And while the backwardation eased with Friday’s flat price selloff, cash-3s remains firmly in a backwardation, closing at $66.5b.

Large backwardations are often a catalyst for warrant deliveries into exchange warehouses but until we see more concrete easing of supply through the Strait of Hormuz it is hard to see exchange stocks being replenished.

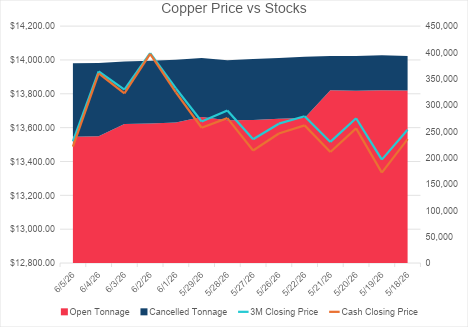

Weekly Open: $13,832 | Weekly High: $14,040.50 | Weekly Low: $13,519.50 | Last: $13,519.50

Cash – 3’s: $32c

Stock: 379,225mt (-10,200mt) | Cancelled Tons: 139,175mt (+27,025mt)

Copper briefly traded above $14,000/mt early in the week but met selling pressure and failed to close above that same barrier on Thursday. It was one of the hardest hit on Friday dropping over $400/mt in a day to finish $116.50/mt lower week-on-week. While the copper price is still at historically elevated levels, Friday’s price action demonstrated how quickly profit-taking can appear when the macro turns less supportive.

Physical indicators were more constructive with LME stocks falling by over 10KMT and cancelled tonnage rising by 27KMT taking cancellations to more than one third of visible stock. Cash-3s tightened slightly finishing at $32c as traders are still looking to LME warehouses as a source for the LME/CME arbitrage trade – where they are still able to achieve CME premiums of $500/mt.

Should copper regain speculative support it could again make a run at the all-time-high.

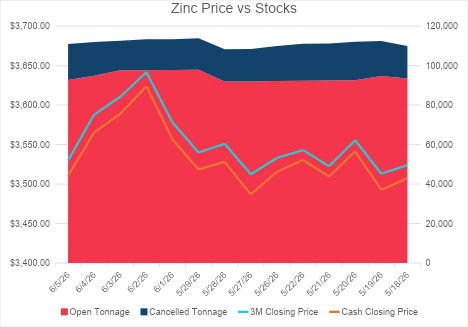

Weekly Open: $3,578 | Weekly High: $3,641.50 | Weekly Low: $3,530 | Last: $3,530

Cash – 3’s: $19.5c

Stock: 110,950mt (-2,850mt) | Cancelled Tons: 18,300mt (+2,350mt)

Compared to the rest of the complex zinc was surprisingly resilient, finishing only $10/mt lower week-on-week despite the broader Friday selloff. This marked a second week where zinc traded in a fairly narrow range. It did have one close above the $3,600 handle but was unable to maintain this level.

There were no significant changes to LME inventories and the nearby cash-3s contango closed only $2 tighter week over week.

The zinc market is not showing the same nearby supply stress as aluminium or attracting the same physical cancellations as copper. However, with less than 100KMT available LME warrants it remains susceptible to volatile moves should demand pick up or we see further smelter disruption.

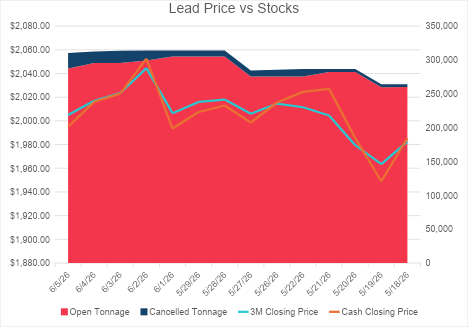

Weekly Open: $2,006.50 | Weekly High: $2,044.50 | Weekly Low: $2,005 | Last: $2,005

Cash – 3’s: $10c

Stock: 310,350mt (-3,650mt) | Cancelled Tons: 23,150mt (+14,375mt)

Another quiet week for lead, finishing slightly lower ($11/mt) week-over-week but holding just above the $2,000 handle to close the week. With the selloff on the rest of the complex there was little hope for lead pushing on from its high of $2,044.50.

After last week’s large stock build, we saw cancellations rise by over 14KMT. Interestingly this did not have much of an impact on the cash-3s spread which actually widened week-over-week, finishing at $10c.

Lead can often trade on its own rhythm, ignoring the broader complex moves. But if cancellations continue to rise we could see upward pressure on the price and tightening in the spreads even if the complex continues to sell off.

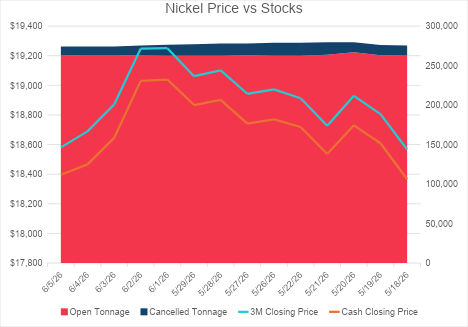

Weekly Open: $19,251 | Weekly High: $19,251 | Weekly Low: $18,581 | Last: $18,581

Cash – 3’s: $185c

Stock: 274,236mt (-2,628mt) | Cancelled Tons: 11,580mt (-2928mt)

Nickel was in a similar boat to copper, falling $481/mt week-over-week and closing at the weekly low. Unable to hold the $19k handle it was not spared from the macro-based selloff. It needs to see further support above $19,000 to push on significantly, with help from either the broader complex or nickel-specific supply story.

Barely any changes in cash-3s spreads or overall stock position.

For now, higher energy and acid prices will likely keep downside limited but for a more durable rally the market will need clearer evidence that those pressures are translating into reduced supply.

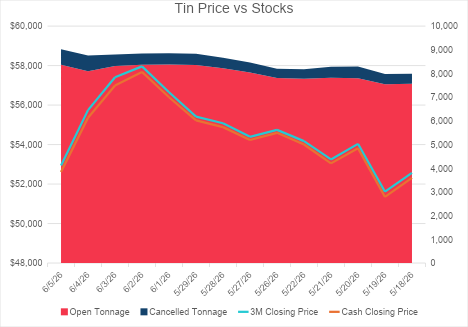

Weekly Open: $56,649 | Weekly High: $57,960 | Weekly Low: $52,935 | Last: $52,935

Cash – 3’s: $325c

Stock: 9,020mt (+190mt) | Cancelled Tons: 655mt (+185mt)

Tin was the most volatile metal of the week. It traded up to a close of $57,960/mt early in the week before reversing sharply to close the week at $52,935, an intra-week drop of over $5k/mt and a week-over-week decrease of $2,483/mt. The size of the move reinforces how sensitive tin remains after the strong rally seen through May.

While tin’s longer-term narrative remains bullish around electronics, AI demand, robotics, and concentrated supply chains, the risk that a large portion of this has already been priced in may leave tin vulnerable. While a deeper correction would not necessarily change that structural story, it may suggest the market needs more supply, or demand-side evidence before re-testing the highs.

May brought a modest increase in China’s copper concentrate imports, but unwrought copper volumes continued to lag last year’s pace.

Konkola Copper Mines has taken its Nchanga smelter offline for planned maintenance, with the shutdown forming part of a wider cycle of outages across Zambia’s copper-processing sector.

Aluminium Bahrain [Alba] has agreed to acquire Aluminium Dunkerque, the largest primary aluminium smelter in the EU, in a deal valued at $2.2 billion, subject to regulatory approval.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 29 May 2026.

Stay connected with our latest developments. Share your details to receive updates and analyses from LME Insight.