Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 29 May 2026.

LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 29 May 2026.

Base metals traded through a shortened 4-day week with Monday 25May closed for the bank holiday. The reduced trading window did not remove volatility, but it did make for a quieter trading week than several others in May.

The main macro theme remains the tug of war between geopolitical risk and persistent inflation concerns. Oil prices fell sharply into Friday on hopes that the US-Iran ceasefire would be extended for 60 days and restrictions around the Strait of Hormuz may ease, reducing pressure on energy-intensive parts of the metals supply chain.

Concurrently the market was pricing a more difficult rates backdrop with reporting that some Fed policy makers were actually discussing the possibility of rate hikes if inflation does not ease. Typically rate hikes would support a stronger US Dollar, making commodities priced in USD comparatively more expensive.

China also remained a mixed demand signal with expectations of the official May PMI release suggesting factory activity will likely be flat, reflecting weaker domestic demand and pressure from higher input costs.

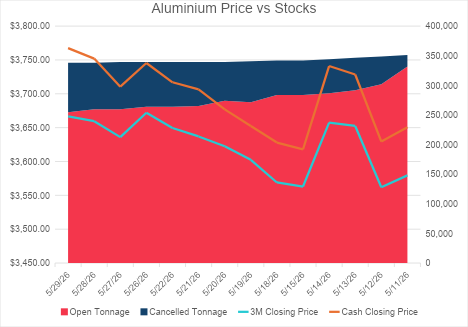

Aluminium finished only $17/mt higher week-on-week but that headline 3M price move understates the continued tightness in the nearby market. The trend is still up as the 3M price continues to hold the $3600 handle – and cash-3s tightened to finish at $101b by Friday.

The disruption in the Middle East alongside US tariffs are causing Canadian aluminium to be redirected toward Europe, where regional premiums have risen sharply as buyers compete for non-Russian and non-Gulf units.

We saw another cancellation bringing cancelled tons above 83KMT, almost a quarter of closing stock – reinforcing the view that exchange stocks are being lent on for prompt delivery.

The biggest risk to the aluminium price is any de-escalation in the Gulf. However, even if a longer-term peace can be achieved, it will not be an overnight fix so aluminium may remain tight for the foreseeable future.

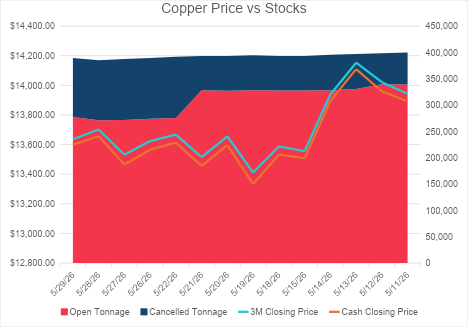

Copper finished $31.50/mt lower week-on-week, with a narrow but choppy range between $13,500/mt and $13,700/mt. Cash-3s remains in contango finishing the week at $36.5c but the trend has certainly been tightening, reducing from more than $80c just a few weeks ago.

Adding to the complexity of the copper price is the potential for another round of US tariffs on copper imports. Cathode was spared in the 2025 tariffs but should it be included we will again see the CME/LME arbitrage widen. The potential for this has already seen that spread increase and traders will look to bring LME material to the US. This could be what is impacting LME spreads with additional interest in prompt material.

As a broader bellwether for the global economy copper continues to benefit from peace talks but could struggle to continue its upward trajectory should inflation, demand, and interest rate concerns persist.

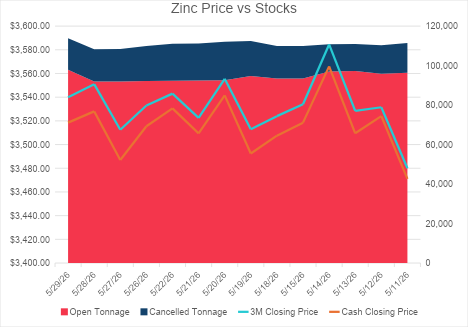

Zinc was largely unchanged this week, finishing just $3/mt lower week-on-week. Zinc again struggled to build momentum above $3,550/mt with a limited range between $3,500-$3,551/mt.

The widening cash-3s spread reflected some of the lack of urgency in the price action moving from $12.5c to finish the week $9 wider at $21.50c. There were no major moves in either stock level or cancelled warrants.

The tougher macro conditions appear to be making it harder for the market to price a clean demand-led breakout but with disruptions at several producers and low LME stocks, zinc remains vulnerable to squeezes if demand improves or further smelter issues emerge.

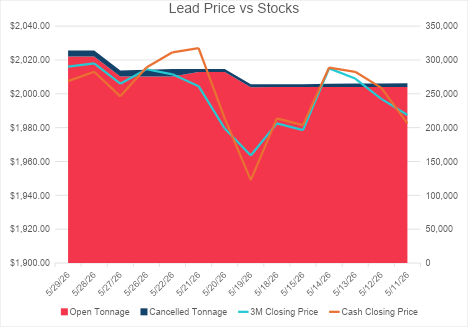

Lead traded quietly this week finishing only $4.50/mt higher, though it did manage to hold above $2,000/mt every close this week. While not as widely traded by the speculative community as copper or aluminium, holding $2,000/mt could attract some technical buying.

The bigger story for lead was the delivery of 27KMT of warrants to the exchange – a sizeable weekly build for a market that often trades on thin liquidity. This delivery helped the cash-3s spread flip from a $13 backwardation last week to close at $8.50 contango this week.

Lead can often trade in isolation to the rest of the complex so it is worth watching for any further moves in exchange stock and price for clues to the short-term direction.

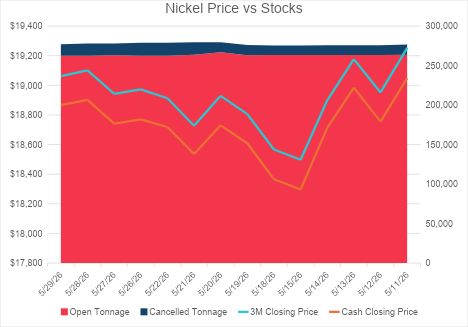

Nickel continued its recent upward trajectory, closing $149/mt higher week-on-week and briefly trading above $19,100/mt. This is the first time in several weeks nickel has looked comfortable above the $19k handle.

There is still a wide contango with cash-3s closing at $195c and no obvious stress in exchange inventories. The support is more likely coming from processing-cost concern and investor positioning than from visible exchange tightness. Sulfuric acid availability remains an issue, especially where processing economics are sensitive to energy and acid costs.

For nickel to build a stronger rally the market likely needs evidence that cost pressures are translating into actual production reductions. Similar to aluminium, this leaves nickel susceptible to reversals should conditions in the Strait improve.

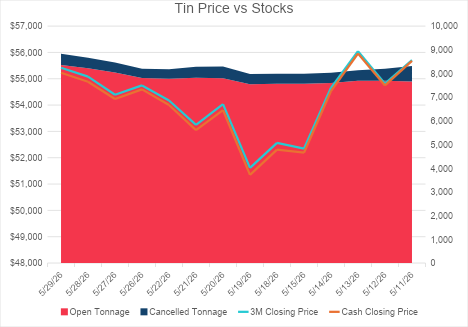

Tin was the strongest performer in the complex, finishing more than $1,200/mt higher week-on-week to close at $55,418/mt. The move took prices back toward levels approaching the all-time-highs we saw at the beginning of 2026.

While there is no immediate pressure on exchange inventories and cash-3s remains in a healthy contango, investors are still betting on scarcity because of tin’s role in electronics, AI, robotics, and concentrated supply chains.

Indonesia’s wider plan to centralize some commodity exports through a state-backed structure remains an item to watch. While tin is not the immediate focus of the first phase, the market has a long memory of Indonesian export policy changes and tin is likely to keep pricing some of that political risk.

LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.