Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.

Base metals traded with a risk-on mindset through the middle of the week before Friday’s selloff pulled most of the complex back from its highs. The immediate catalyst for the pullback appeared to be disappointment that President Trump’s visit to China failed to produce any real breakthroughs on either trade, or the Iran conflict. That left markets facing the same uncomfortable mix of elevated geopolitical risk, uncertain China demand, and higher energy and shipping costs.

The volatility of this week’s price moves seem to be more macro-driven than fundamental with spreads and warehouse moves showing limited immediate physical tightness.

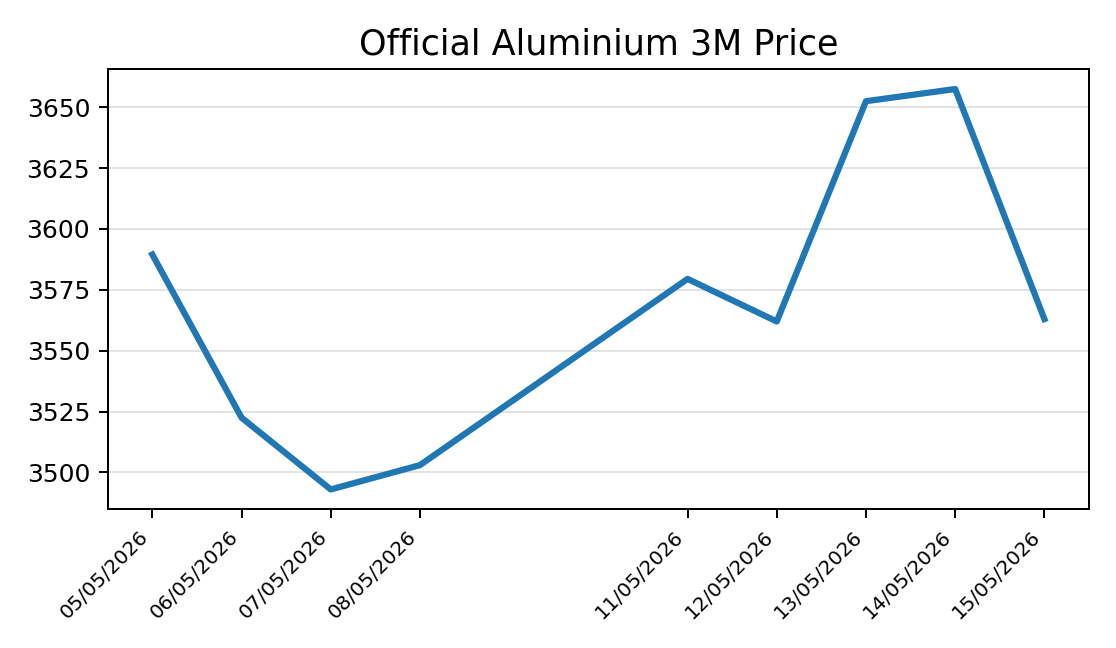

Aluminium held up better than most of the complex, still able to finish $60 higher week over week despite giving back Wednesday’s gains on Friday. While aluminium started the week strong on the back of the continued Iran conflict and ongoing supply concerns, it was caught up in the broader risk-off end to the week.

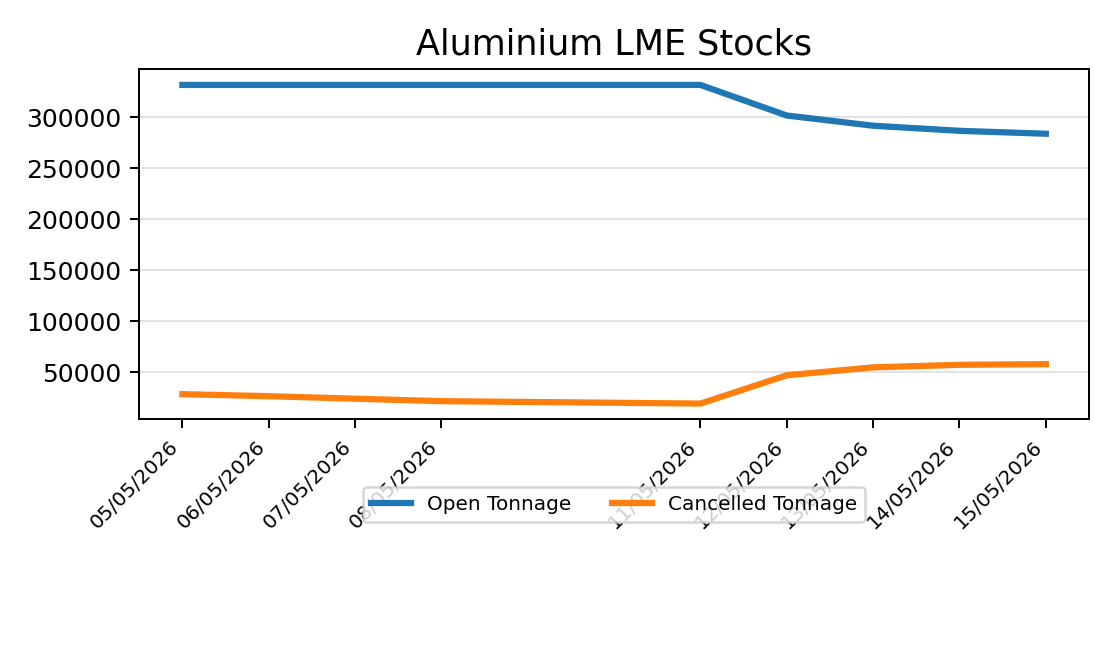

The more interesting move this week was in stocks rather than price. Closing stocks fell 11,575mt on the week but cancelled tonnage increased by 36,275mt to 57,900mt. Cancelled warrants are metal that has been earmarked for withdrawal from LME warehouses. It does not always leave immediately but it is a signal to the market that exchange metal may be moving toward physical consumption. Given the potential for a drawn out conflict, traders appear to be seeking replacement units from the exchange.

While the cash-3s backwardation did soften with the selloff from $84b to $55b, this cancellation can help explain why spreads remain tight. In a backwardation nearby prices are higher than further out prices – traders are willing to pay more to access prompt material than they are in the future when supply constraints may have eased.

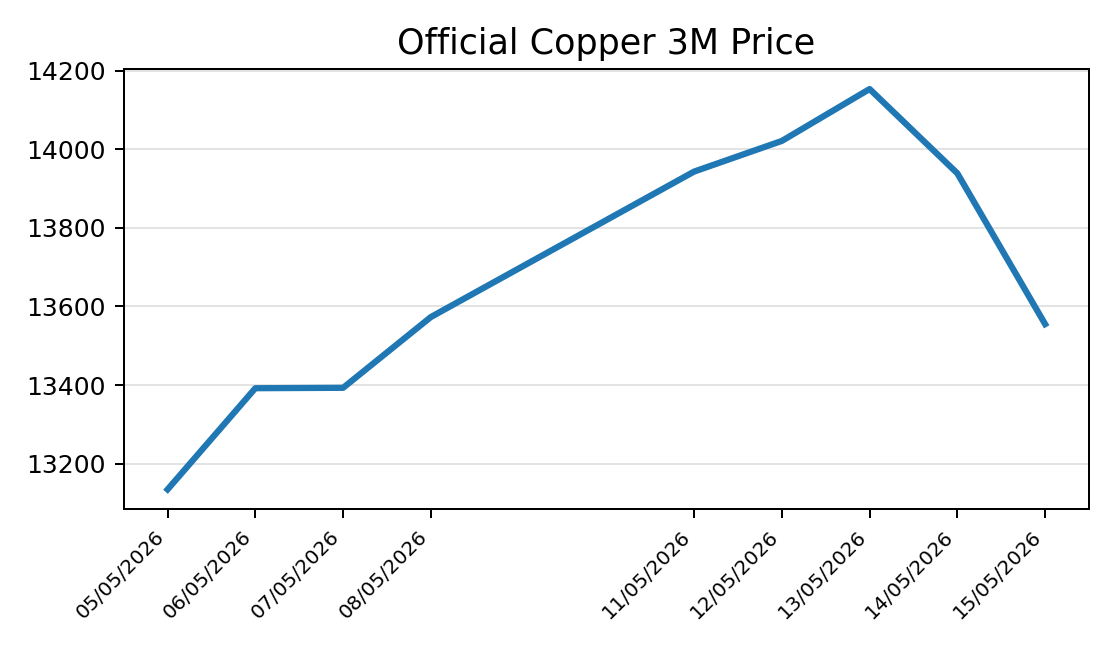

Copper was looking strong through the middle of the week, closing at a high of $14,153/mt on Wednesday off the back of strong technical buying. However, this reversed sharply on Friday to close at $13,555/mt leaving copper almost unchanged week on week. While coming within $400/mt of its all time high, the rally failed.

Copper is the base metal most closely tied to macro expectations and fund positioning. When markets were hoping for a breakthrough, copper was a beneficiary but when those hopes faded it was also one of the first places risk was reduced.

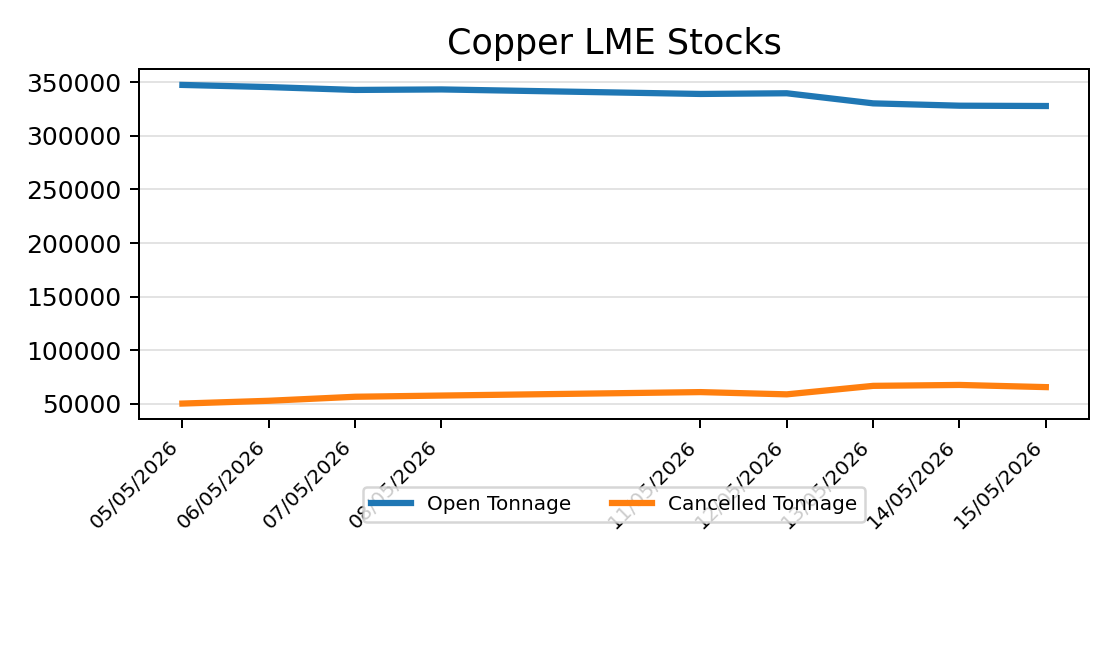

Stocks remain high and the cash-3s spread has been consistent between $40-$60c, finishing the week at $47c. While macro may be driving the price action, physical demand is not seeing the same tightness for now. Should the supply or demand picture change, this could be the push copper needs to re-test its all time high.

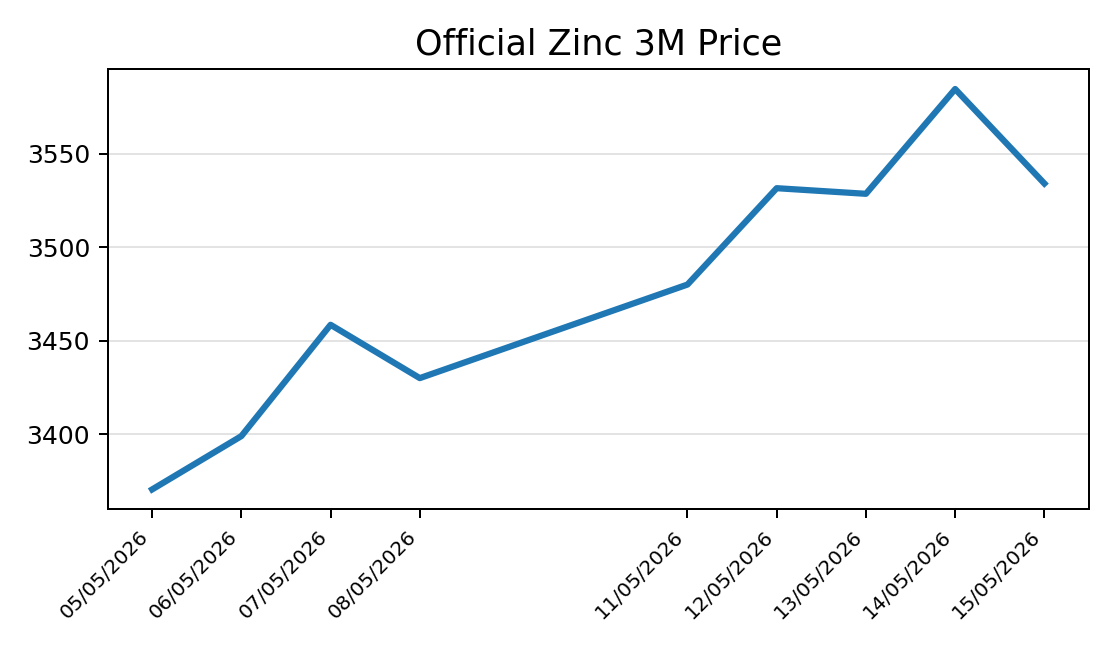

Zinc had a standout week, rallying $104/mt above the previous week’s close and managing to retain a large part of those gains even after Friday’s selloff. Zinc has actually been lagging certain parts of the complex but it still remains sensitive to energy costs and smelter economics. It was also buoyed by news that Glencore-owned Kazzinc in eastern Kazakhstan announced reduced operating capacity after an explosion the previous week.

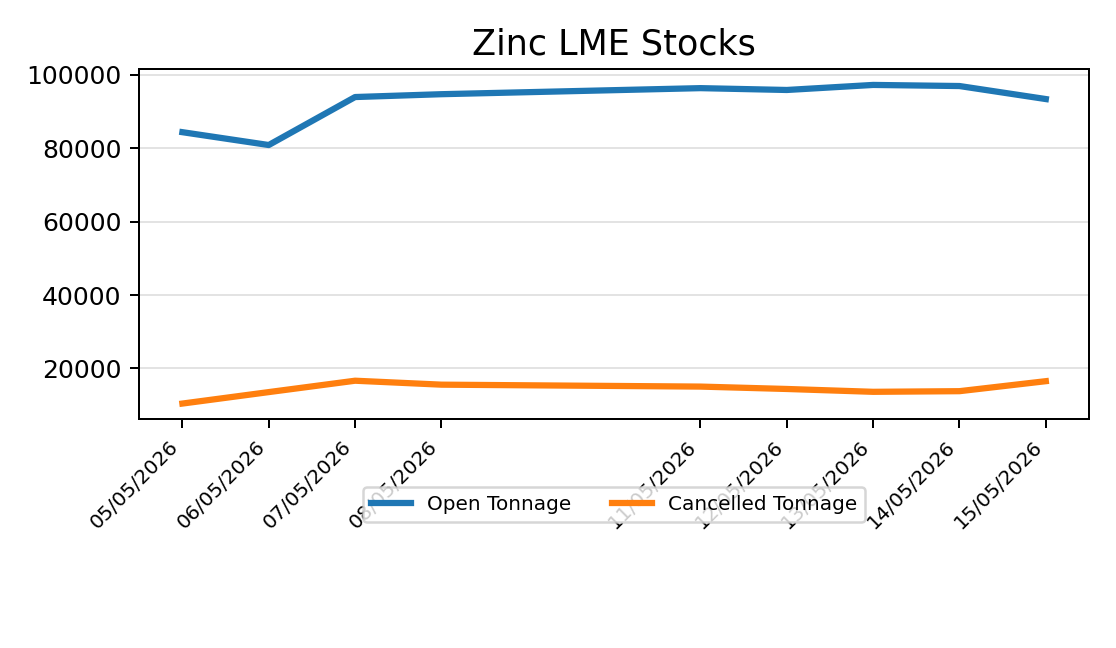

We did not see any large moves on zinc stocks this week, however there is only 111,925mt of exchange stock remaining, and 22% of that has already been cancelled. The cash-3s spread is still in a contango but should we continue to see the stock reduce, I would expect to see this spread tighten.

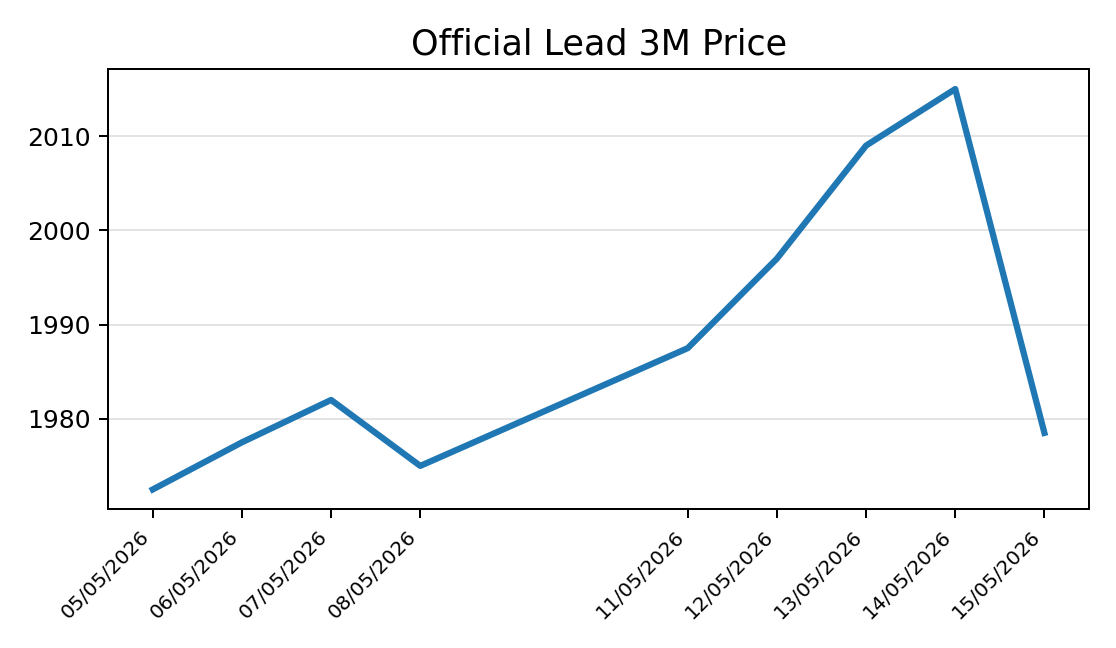

Lead continued to trade in a tighter range than the rest of the complex. It briefly reclaimed the $2,000/mt handle on Wednesday and Thursday but Friday’s selloff dragged it back down to settle at $1,978.50, just $3.50/mt higher than the previous week.

This relative calm is fairly typical for lead. It has a much more industrial, less speculative profile than copper or aluminium, so it often participates in broader base metal moves without matching their volatility. However, the fact it could not hold above $2,000/mt may attract further selling if the broader complex remains under pressure.

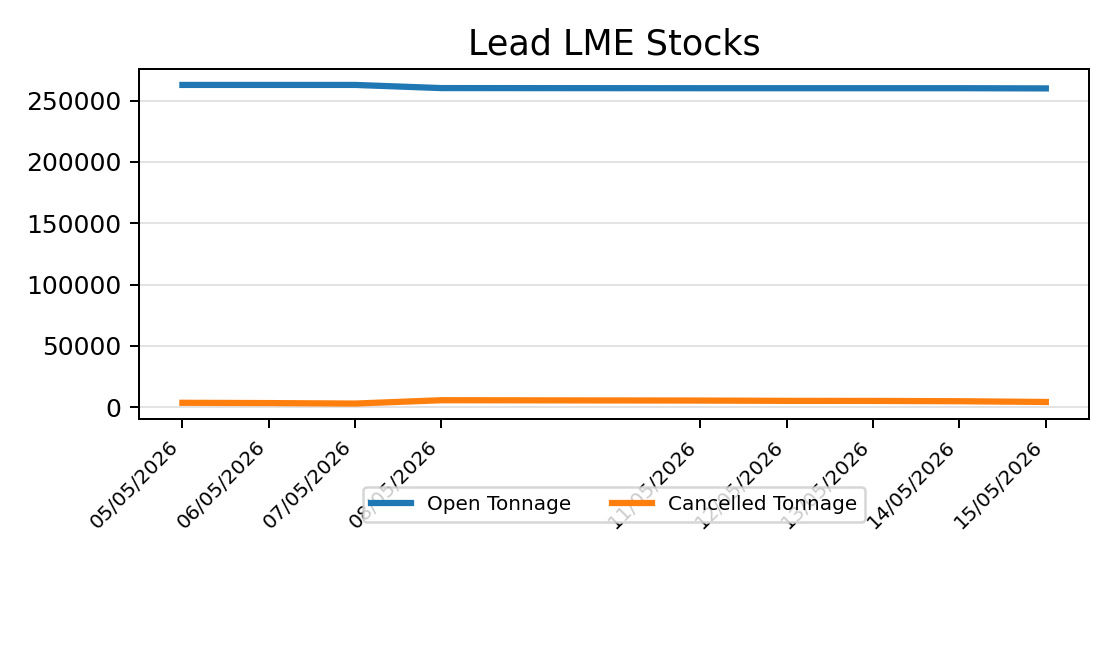

A slight divergence from the price was the cash-3s spread, moving from a $9 contango the prior week to a $3 backwardation by Friday’s close. While the shift is small in absolute terms, it still signals a firmer nearby market. While we have not seen any large cancellations, lead is always susceptible to pressure given its lower liquidity so we should monitor for further pressure.

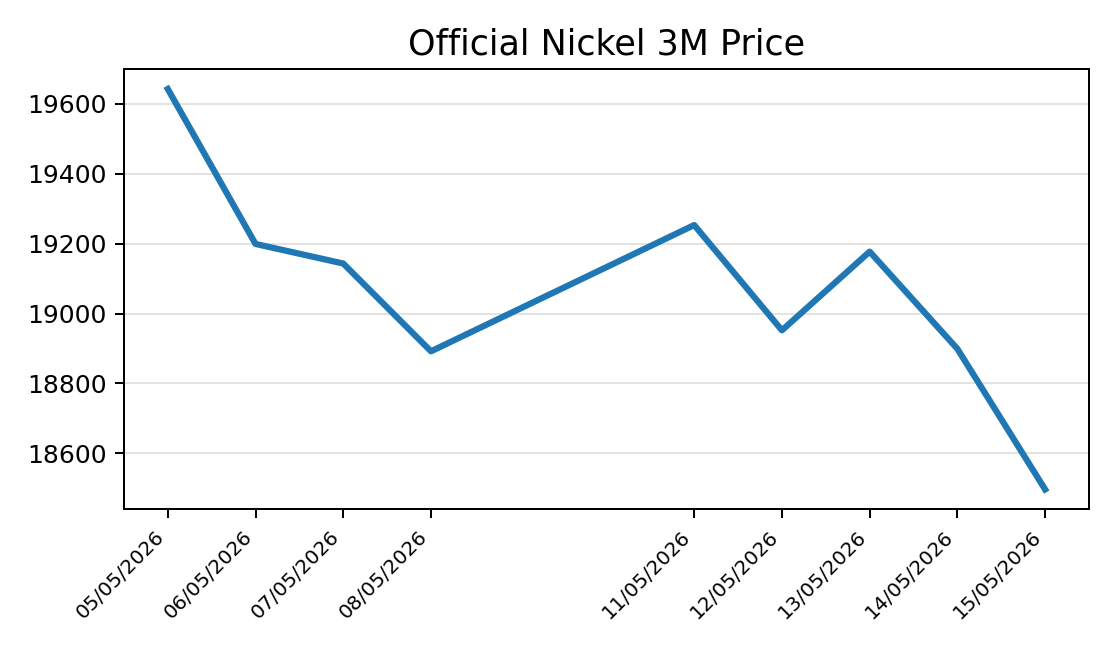

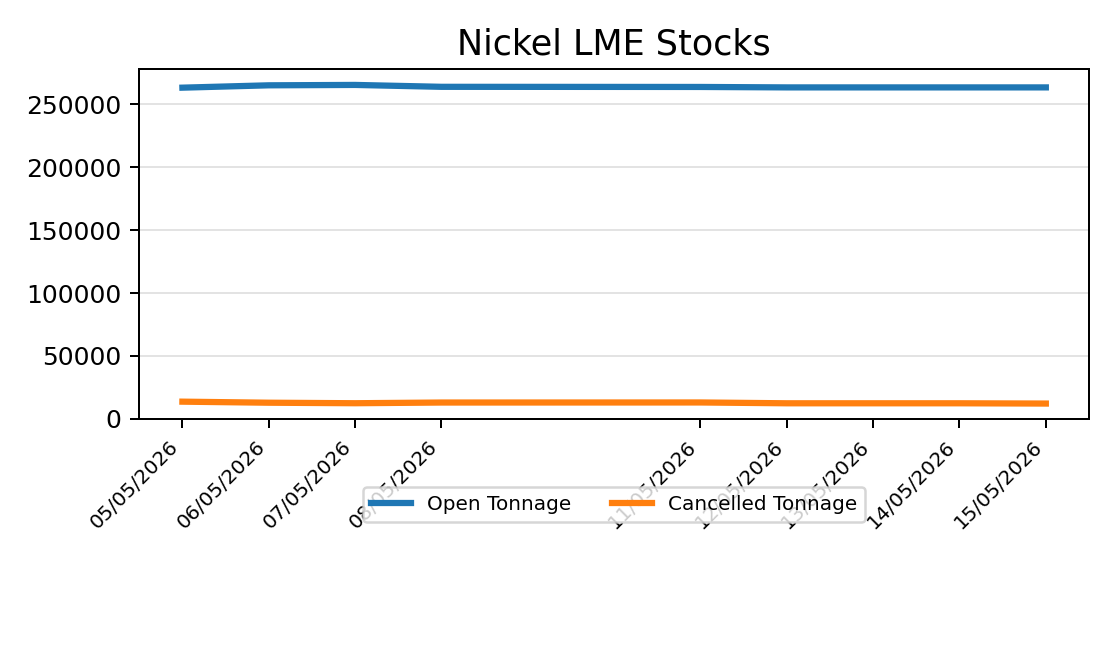

Nickel came under the most consistent pressure across the week, falling $395/mt from the prior week’s close and finishing the week on its low. Unlike zinc, nickel could not hold the early-week bid and headed lower with the complex selloff.

Warehouse stocks remain high and cash-3s are sticky around $200c, suggesting little urgency in the physical fundamentals. Nickel has not yet been able to regain the $20,000 handle and each attempt that is rebuffed makes it harder from a technical standpoint.

Until we see broader physical tightness or a genuine supply disruption nickel is likely to trade with the rest of the complex.

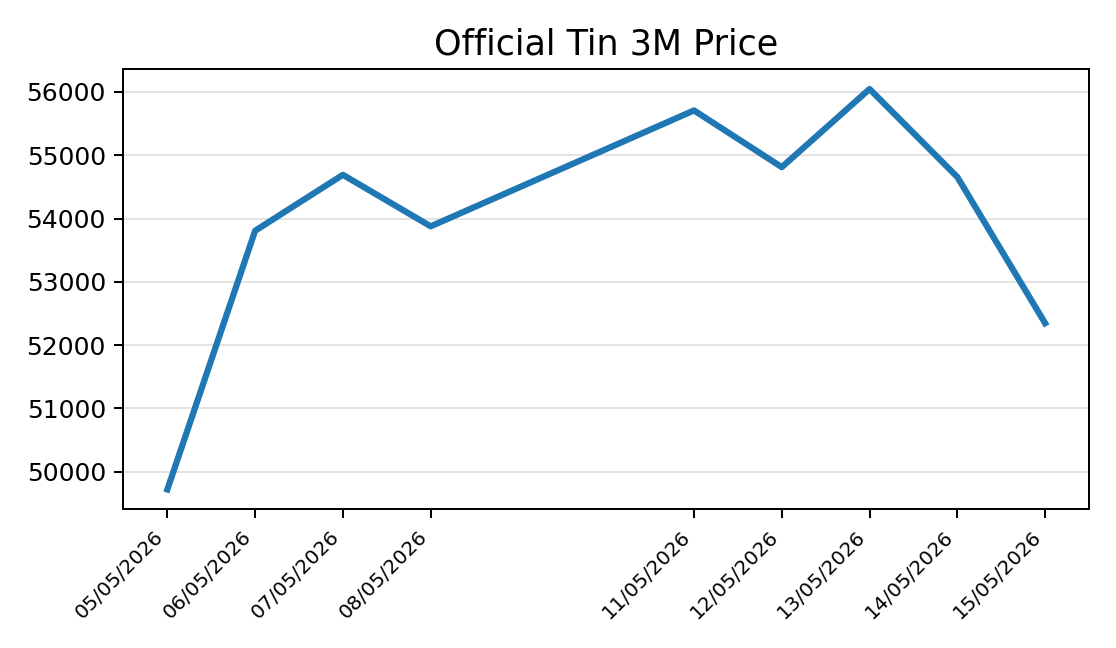

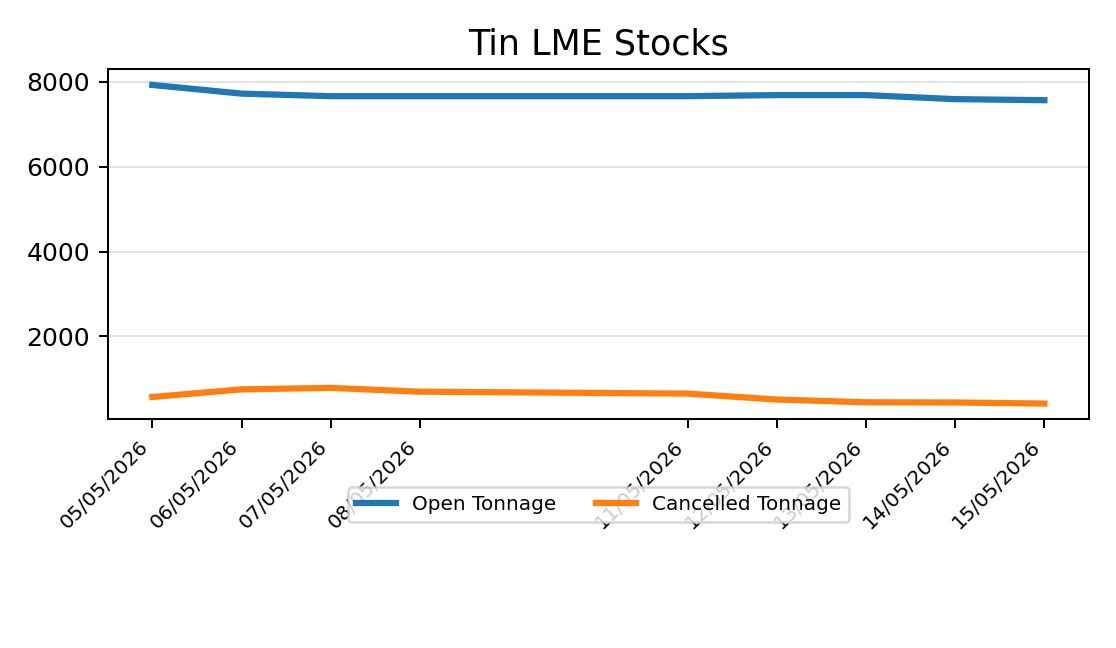

Tin remained the most volatile metal of the complex as it traded as high as $56k on Wednesday before selling off almost $4,000/mt by the end of the week to close at $52,347/mt – a $1,530/mt decrease versus the prior week’s close. The moves this week were a reminder that tin can move far more aggressively than the rest of base metals when liquidity is thin.

Spreads also softened with the selloff, with cash-3s trading in to $30c during the rally then settling at $155c on Friday. With limited warehouse stock moves, spreads are likely to follow price action with rallies leading to a tightening spread and selloffs causing a loosening.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.

Nickel markets are focused on Indonesia’s quota cuts – but tightening sulphur supply is the real story. Disruptions in Iran, the Gulf and China, combined with declining hydrocarbon output, are constraining availability and reshaping the market balance.

Aluminium and copper are reacting differently to the same conflict. Aluminium faces real supply shocks – force majeure, halted smelters, surging premiums and constrained output – creating a price floor Copper’s rise reflects risk pricing amid ample supply, leaving it vulnerable to rapid reversal.