Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Base metals experienced another volatile week as markets reacted to a combination of deteriorating Chinese economic data, continued geopolitical tensions in the Middle East, and growing concerns over inflation and interest rates.

The week began with continued selling after Chinese industrial production and retail sales figures both missed expectations, reinforcing concerns that underlying industrial demand remains softer than many had hoped.

At the same time, the ongoing Iran conflict continued to create disruption across energy and metals supply chains. Oil prices remained elevated throughout the week, increasing pressure on global energy and sulfur dependent industries.

Despite the increasingly difficult macro backdrop, several physical indicators across the LME complex remain relatively constructive. Aluminum backwardations stayed elevated, and cancelled copper warrants increased sharply against the renewed potential for U.S. tariffs.

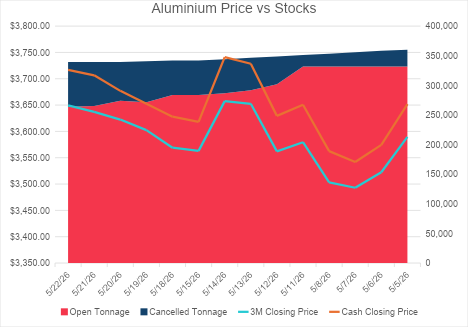

Aluminium had another strong week, finishing $86.5/mt higher week-on-week and closing on the weekly high. The price matched the broader news flow with aluminium remaining the metal most directly exposed to the Gulf supply shock. Prices, regional premiums, and nearby spreads are all adjusting upward to the impact of the Iran conflict.

We saw a significant movement in LME warehouse stocks with cancelled tonnage rising 17,675mt to 75,575mt. This means cancelled warrants now represent 22.3% of total closing stock as of Friday. A rise in cancelled warrants suggests some traders are looking to the LME inventory to replace units they would otherwise be sourcing direct from producers in the Gulf.

Cash-3s also tightened from $55b as of the close on the 15th to $67.5b as of Friday’s close. Participants are willing to pay higher prices for immediate access to metal. While aluminium still looks like the tightest fundamental story in the complex, it is also most exposed to reversals should a longer-term peace be reached that opens shipping in the Strait.

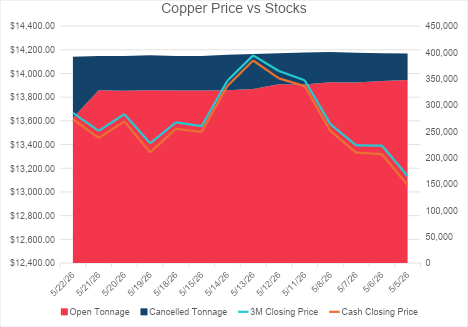

Copper finished the week up $112.50/mt higher but it had a choppier path than aluminium. Last week’s momentum continued with a risk-off Monday and Tuesday but a lack of increased military action in Iran gave some respite and copper finished the week at its highs.

The larger story this week was a significant cancellation of nearly 51 thousand tons, taking total cancelled warrants to 116,375mt. With increasingly tight TCs in the copper concentrate market (China reported TCs have broken negative $100 for the first time) we may see some of this material move to fill that smelter production.

There were also rumors that cancelled LME warrants in the US may make their way to domestic sales after a possible cathode tariff decision in late June – allowing traders to capture the valuable CME/LME arbitrage which has increased to CME premiums over LME of $600/mt.

The cash-3s spread remains in a contango, though the trend has been a tightening since mid-March. With nearly 30% of total stocks cancelled, we may see copper spreads under further pressure, particularly if there is any escalation in the Gulf or additional warrant cancellations.

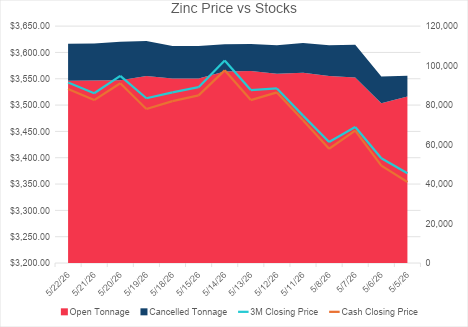

Zinc traded in a narrow range and finished only $9/mt higher week-over-week and it has been unable to move past the recent high from the 14th meeting resistance on its rally last Wednesday.

Continued disruptions at Glencore’s Kazzinc operation and Nexa’s Cajamarquilla smelter have tightened the fundamentals but this comes against a broader fear of demand destruction the longer energy prices remain high.

The relatively small cash-3s contango reflects the low overall exchange stocks, leaving zinc susceptible to sudden cancelations and squeezes should demand increase or additional smelter curtailments occur.

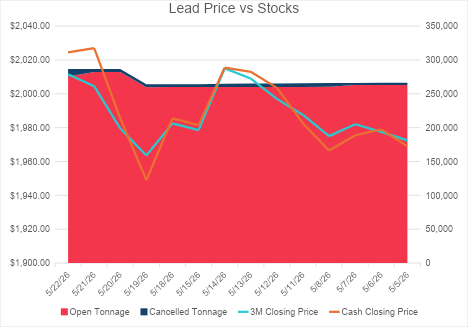

Lead finished $33/mt higher week-on-week and importantly closed above the $2,000/mt level. The price move was notable as it occurred alongside a significant warrant delivery on the 20th with LME inventories rising 22,225mt. Typically that kind of stock increase would put pressure on flat prices and spreads but both markets tightened with cash-3s moved from $3b the previous Friday to $13b by this week’s close.

While lead can often trade in a contrarian fashion to the rest of the complex, this week it was largely following zinc’s lead. This could be because the Kazzinc facility is a producer of both zinc and lead so disruptions are impacting both markets.

Lower liquidity in lead means that spread moves can quickly become exaggerated when nearby supply expectations shift. The fact that spreads tightened while stocks built is worth continued monitoring.

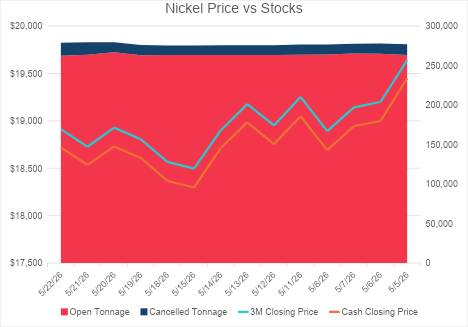

Despite Thursday’s dip, nickel performed well last week, finishing up over $400/mt week-over-week. Stocks rose and the cash-3s spread remains in a healthy contango signaling limited urgency for prompt metal.

However, sulfur shortages have been putting pressure on Indonesian nickel processing so any sustained hit to processing costs or operating rates is likely to continue driving the near-term price action. But while there have been encouraging signs nickel has yet to re-take the $19k handle and with exchange inventories not under pressure, it may take a more fundamental shift to accelerate any price gains.

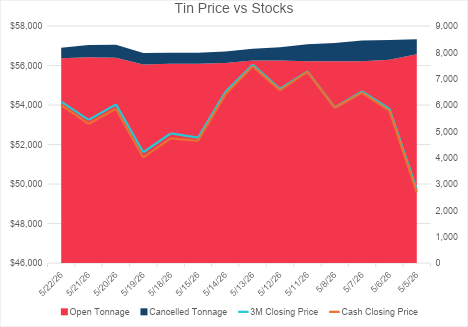

Tin recovered $1,800/mt from last week’s selloff but still closed well below the $56k print from the 13th. The scale of the moves we are seeing over the last few weeks highlights just how quickly tin can reprice when liquidity is thin – trading up 5% on Wednesday.

No major changes on exchange stocks, spreads did see the contango ease midweek to over $200c but finished the week at $170c.

Some of the upward move midweek could be related to plans announced by Indonesia to centralise control of certain commodity exports through a state trading structure. While tin was not the immediate focus of the report (initially focusing on palm oil, coal, and ferroalloys), tin has historically been sensitive to export rules and policy changes and every three months there will be a review to add more commodities.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.

Nickel markets are focused on Indonesia’s quota cuts – but tightening sulphur supply is the real story. Disruptions in Iran, the Gulf and China, combined with declining hydrocarbon output, are constraining availability and reshaping the market balance.