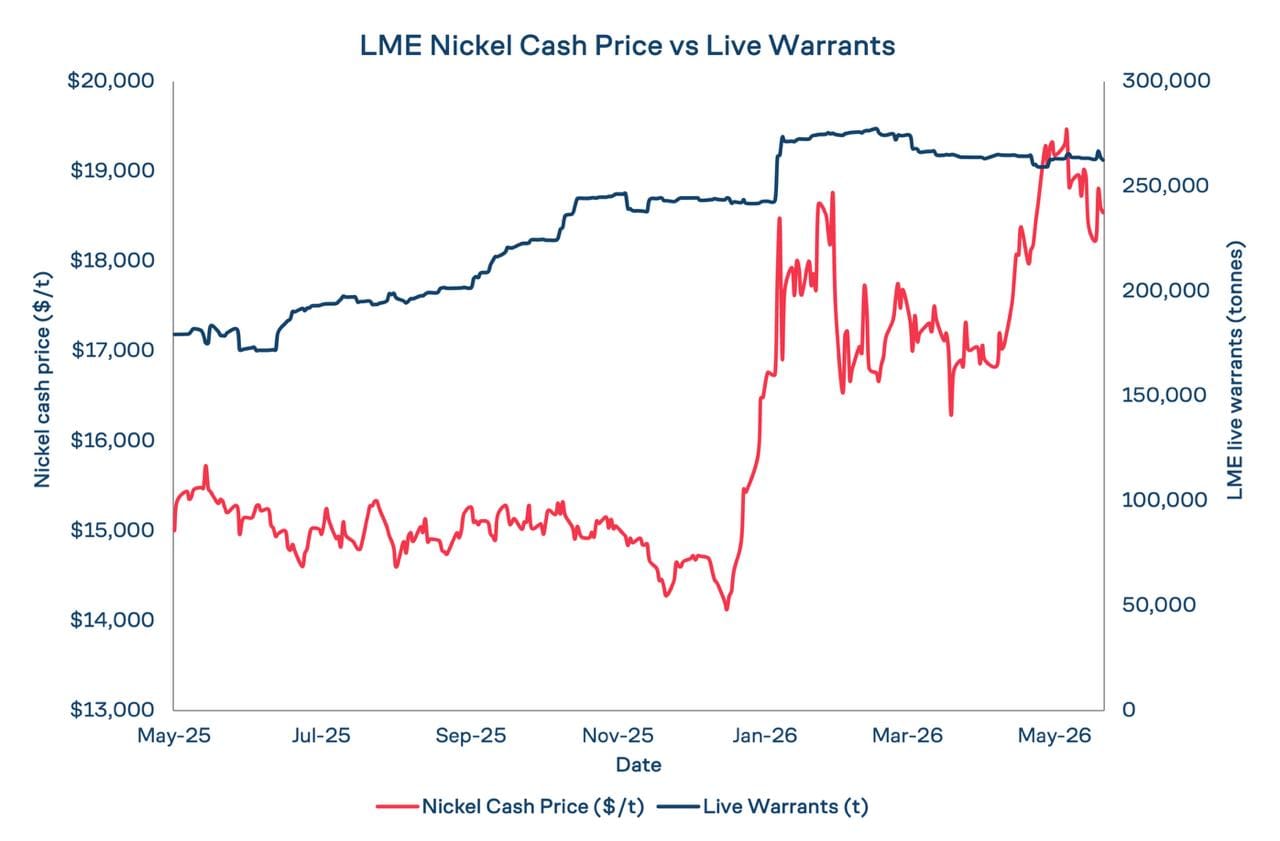

LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

News & Market Analysis:

Nickel’s Hidden Tightness - What Physical Premiums Are Telling the Broader Market

LME Nickel closed at $18,540/mt on 21 May, up over $2,200 from its mid-March low. Indonesia accounts for ~60% of supply; and the market has run a surplus for four years. That suggests oversupply, yet physical premiums and warrant data point to tighter conditions, defying the fundamentals.

LME Nickel closed at $18,540/mt on 21 May, up more than $2,200/mt from its year-to-date low in mid March. Indonesia accounts for around 60% of global output and the market has been in structural surplus for four consecutive years.1 On that reading, nickel is an oversupplied market working through its excess, but physics and politics have a funny way of defying fundamentals.

Physical premiums tell a different story, as does the warrant data.

What the Exchange Stock Is Hiding

LME Nickel closing stocks rose from 255,354 tonnes at the start of January 2026 to a peak of 289,506 tonnes on 25 February, before drawing back to 279,072 tonnes as of 21 May.2 The headline build looks comfortable but cancelled warrants are sending a different signal.

Cancelled warrants stood at 9,792 tonnes on 9 February, representing 3.43% of total stock. By 6 March that figure had reached 21,090 tonnes, or 7.34% of inventory, the highest reading of the year to date, as more than 11,000 additional tonnes were queued for physical delivery in four weeks. Cancelled warrants do not automatically indicate physical loadout: many are rewarranted, financed, or relocated within the LME warehouse network. The direction of travel and the speed of the move matter more than the absolute level. The January average was 11,655 tonnes. The March average was 18,533 tonnes.3

Open tonnage, the live warranted stock actually available to the market, peaked at 277,530 tonnes on 16 February and has drawn down by nearly 15,000 tonnes since. Cancelled warrants as of 21 May stand at 16,518 tonnes, above the January average of 11,655 tonnes and modestly above the 2026 year-to-date average of 14,287 tonnes. The YTD range runs from a low of 9,282 tonnes on 22 January to a peak of 21,090 tonnes on 6 March, giving a full-year average cancellation rate of 5.07%.

The YTD cash price low of $16,290/mt was recorded on 19 March, in the middle of the peak cancelled warrant period. The elevated cancellation rate coincided with the price trough, though the destination of that metal, whether consumption or alternative storage, remains unclear from the data alone. The paper market was pricing macro conditions and Indonesian supply; the physical market was reflecting regional Class 1 availability. These are not contradictory readings so much as different realities operating on different time horizons.

The cancelled warrant data shows two distinct phases of elevated cancellation activity, consistent with supply-side anxiety over specific product forms rather than a broad upturn in Western demand, which has remained subdued across stainless, EV, and alloy end-uses. The first, from late February into March, coincided with the halting of production at Ambatovy in Madagascar following cyclone damage on 13 February.4 The second wave, in late April, followed Sherritt International’s suspension of its Cuban joint venture at Moa, which produced 25,240 tonnes of nickel in 2025.5 Sherritt cited US sanctions pressure.

Neither Ambatovy nor Moa produces finished cathode. Both are primary producers of nickel briquettes, a Class 1 LME-deliverable form. Both supply mixed intermediate products into European and North American Class 1 refining pipelines. The disruptions were to feedstock availability, but physical traders read the downstream implications before it reached the exchange price.

The Class 1 Problem

Indonesia’s production growth has been overwhelmingly concentrated in Class 2 products: nickel pig iron for stainless steel and mixed hydroxide precipitate for the battery supply chain. Neither is LME deliverable. Neither substitutes directly for a refined Class 1 cathode, where cathode is the required form. Indonesian MHP output alone rose approximately 50% in 2025.6

That material feeds primarily into cathode refineries in China and Indonesia, and forms part of the input mix for some Class 1 producers elsewhere. It does not, on any meaningful scale, reach European cathode consumers or US industrial buyers in deliverable form.

The Russian-origin component of LME warrant stock compounds this. The LME suspended the warranting of new Russian metal produced on or after 13 April 2024, with Norilsk’s Harjavalta refinery in Finland as the principal exception, given its non-Russian production base. Pre-restriction Russian material already warranted remains deliverable but has faced effective exclusion from much of the Western purchasing base since UK and US sanctions took effect.7 The fraction of Russian-origin stock in LME nickel warehouses is not publicly disaggregated in real time; whether it materially narrows the usable buffer depends on how far buyer avoidance extends into the warranted pool.

Three Markets, Three Different Signals

In Europe, cathode premiums moved from low hundreds of dollars per tonne at the start of 2026 to the mid-$200 to $400/mt range by May, with higher specification and cut cathode holding $400 to $600/mt. Briquette premiums showed the sharpest move of any Class 1 product form, rising from near $100/mt before stabilising at lower levels: fundamentals-driven moves reflecting genuine feedstock tightness due to unavailable Russian tonnes and the drawdown of other global supply.

In the United States, premiums reflected policy risk rather than physical shortage. Section 232 investigations and broader tariff uncertainty created sharp risk-pricing in physical markets through the second half of 2025, even though critical minerals, including nickel, were effectively exempted from the April 2025 reciprocal tariff wave.8 The uncertainty was absorbed by physical inventory holders before the outcome was known.

China presents a third dynamic. Battery-grade nickel sulfate prices moved incrementally alongside LME benchmarks within term contract structures, from the high 20,000s yuan/mt in late 2025 to the low 30,000s yuan/mt by mid-2026. There was no comparable premium spike here because the product form, pricing mechanism and supply chain architecture are all different, with Class 2 feeding directly into the battery and stainless steel markets.

Jakarta Changes the Equation

Indonesia’s decision to cut the 2026 mining quota from 379 million tonnes to 260 to 270 million tonnes, a reduction of around 30%,9 has now challenged the oversupply narrative at the headline level. The RKAB cut is not the only constraint in play. Jakarta’s proposed export levy on nickel products, though subsequently withdrawn, created additional uncertainty for producers and traders during the first quarter. Separately, a structural shortage of sulphur and sulphuric acid has constrained HPAL output, with downstream implications for MHP supply chains that run parallel to the quota reduction. Quota levels remain subject to revision and market reports suggest RKABs could be increased again in coming months. LME nickel cash prices rallied from $16,290/mt on 19 March to $19,450/mt on 6 May, recovering $3,160/mt in seven weeks. As of 21 May, cash trades at $18,540/mt with the three-month contango at $220/mt. The contango ranged between $100/mt and $290/mt across the year. For a market supposedly carrying a heavy surplus, the incentive to finance and hold warranted inventory has been consistently limited.

Physical premiums across European and US markets responded to regional supply signals, not global surplus data. The LME cancelled warrant series corroborates that reading. Demand for physical delivery intensified precisely when regional Class 1 supply was under most pressure, at a moment when the LME cash price was near its weakest point of the year.

Physical premiums are not a replacement for LME price discovery. They measure the cost of sourcing the specific product, in the specific location, from the specific origin that a buyer needs. In a market where the surplus is concentrated in Class 2 and the tightness in Class 1, where Russian material occupies warrant space but not buyer orders, and where feedstock disruptions in Madagascar and Cuba ripple through European refining pipelines months later, that differential functions as a secondary barometer with genuine diagnostic value.

Indonesia’s policy reversal has now begun to shift the LME price toward what physical premiums were already signalling. The premiums data was leading, not lagging.

1 ING Think, "Nickel still capped by surplus," 8 December 2025; MMTA, "Nickel's Evolving Market," 7 October 2025 ("The nickel market is now entering its fourth consecutive year of oversupply"). 2 LME daily warrant data, 2 January to 21 May 2026. 3 LME daily warrant data, 2 January to 21 May 2026. 4 Kitco/Reuters, "Madagascan miner Ambatovy's operations hit by cyclone," February 13, 2026; CNBC Africa, 14 February 2026; Sumitomo Corporation, "Impact of Cyclone Gezani at the Ambatovy Project," 18 February 2026. 5 Sherritt International, Full Year 2025 Annual Report: "Full year 2025 production reached 25,240 tonnes of nickel and 2,728 tonnes of cobalt (100% basis)." 6 Argus Media, "Viewpoint: Indonesia's MHP surge to hit nickel prices," 18 December 2025: "Indonesia's MHP output is projected to reach 482,000t in nickel metal equivalent this year — almost a 50pc rise from 2024." 7 LME Warehousing Notice WAREHOUSING-BRANDS-24-171, 13 April 2024; Reuters, "LME bans Russian metal following new US, UK sanctions," 23 April 2024; UK Government, "Russian metals sanctions: overview," GOV.UK. 8 SFA Oxford, "U.S. National Emergency on Trade: Tariffs, Exemptions," 3 April 2025 ("PGMs, rare earths, and critical minerals are exempt from the tariffs"); Federal Register, Executive Order on Section 232 Actions on Processed Critical Minerals, 18 April 2025. 9 Mysteel, "Nickel prices surge as Indonesia plans one-third cut," 29 December 2025; Benchmark Mineral Intelligence, "Indonesia announces significantly lower nickel RKAB quotas"; Shanghai Metals Market, 26 February 2026; The Oregon Group, 11 February 2026.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 22 May 2026.

Carbon pricing is reshaping aluminium markets. As CBAM introduces a measurable cost on emissions, high-carbon metal becomes less competitive while low-carbon supply gains value. The result is a structural shift in pricing, trade flows and the emergence of a green premium within global markets.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 15 May 2026.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.