The LME Weekly Review: 15-19 June 2026 - Spotlight on Aluminium

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

Aluminium and copper are reacting differently to the same conflict. Aluminium faces real supply shocks – force majeure, halted smelters, surging premiums and constrained output – creating a price floor Copper’s rise reflects risk pricing amid ample supply, leaving it vulnerable to rapid reversal.

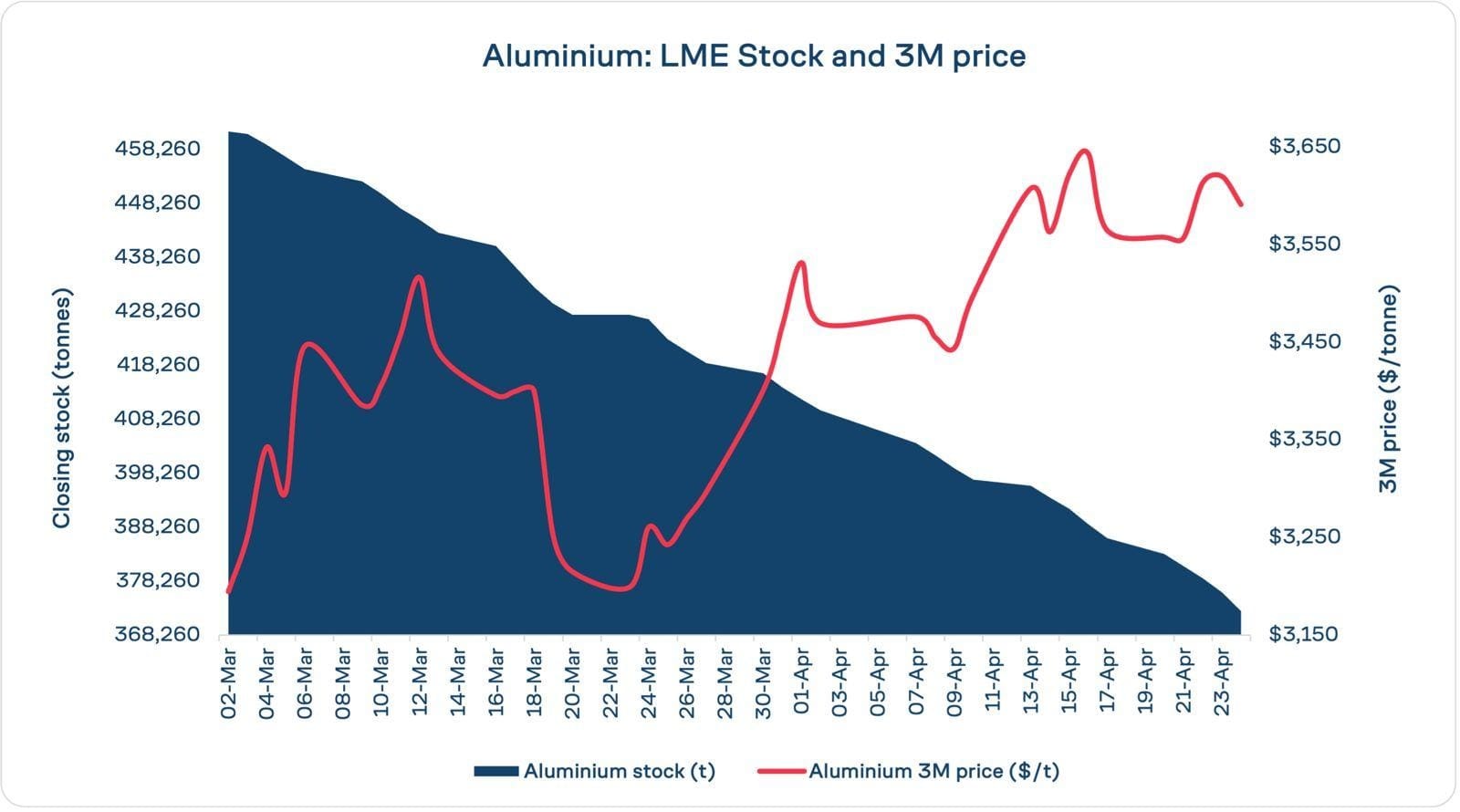

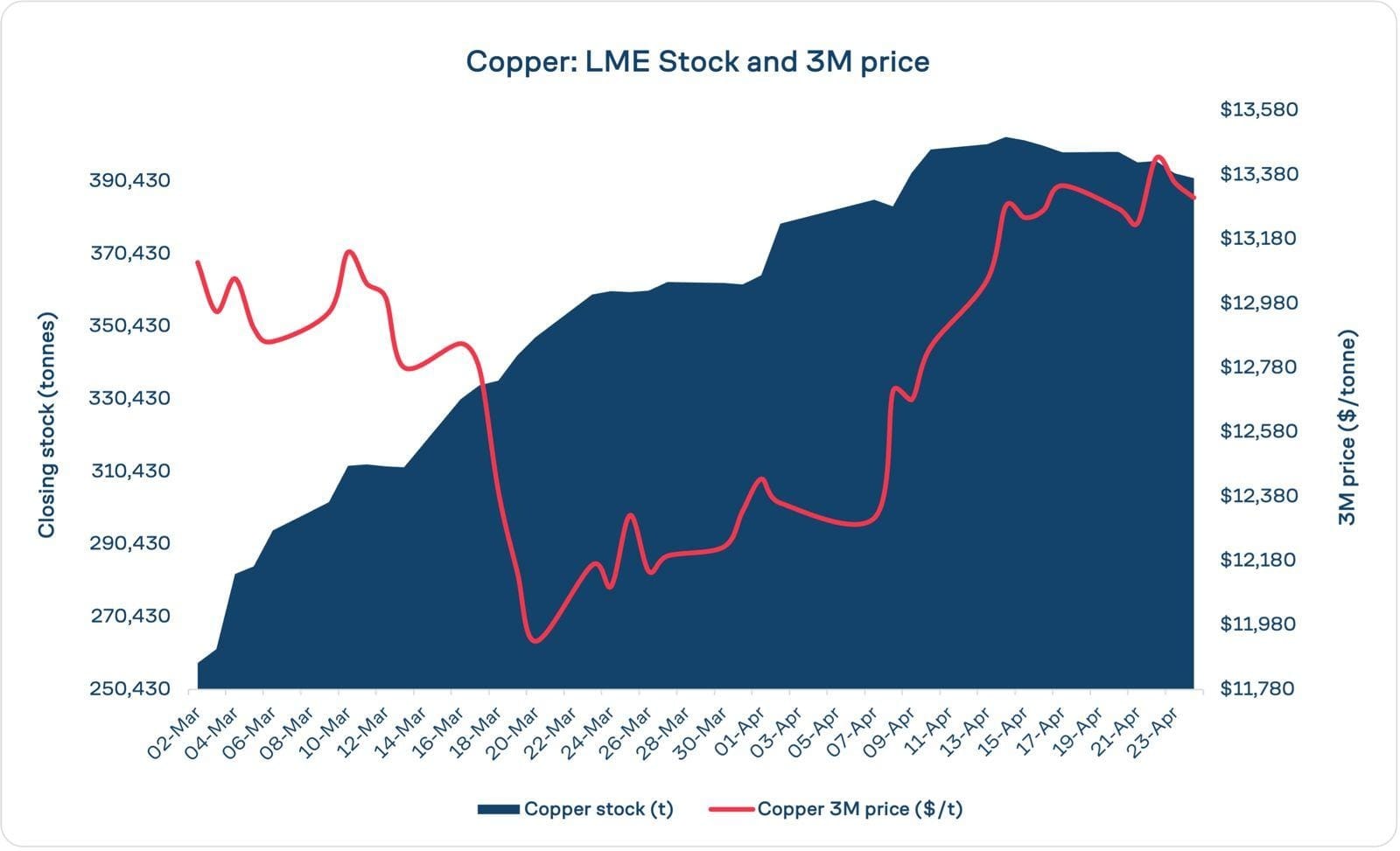

LME three-month aluminium ended the week 24 April at $3,591/mt. Three-month copper closed at $13,309.50/mt. Both metals are reacting to the Iran conflict. The drivers, however, are different.

The Iran war has generated two metals markets operating on different logics. Aluminium's price is largely anchored in physical constraint while copper’s is anchored in financial positioning. The distinction matters because the two metals are being driven by two distinctly different narratives.

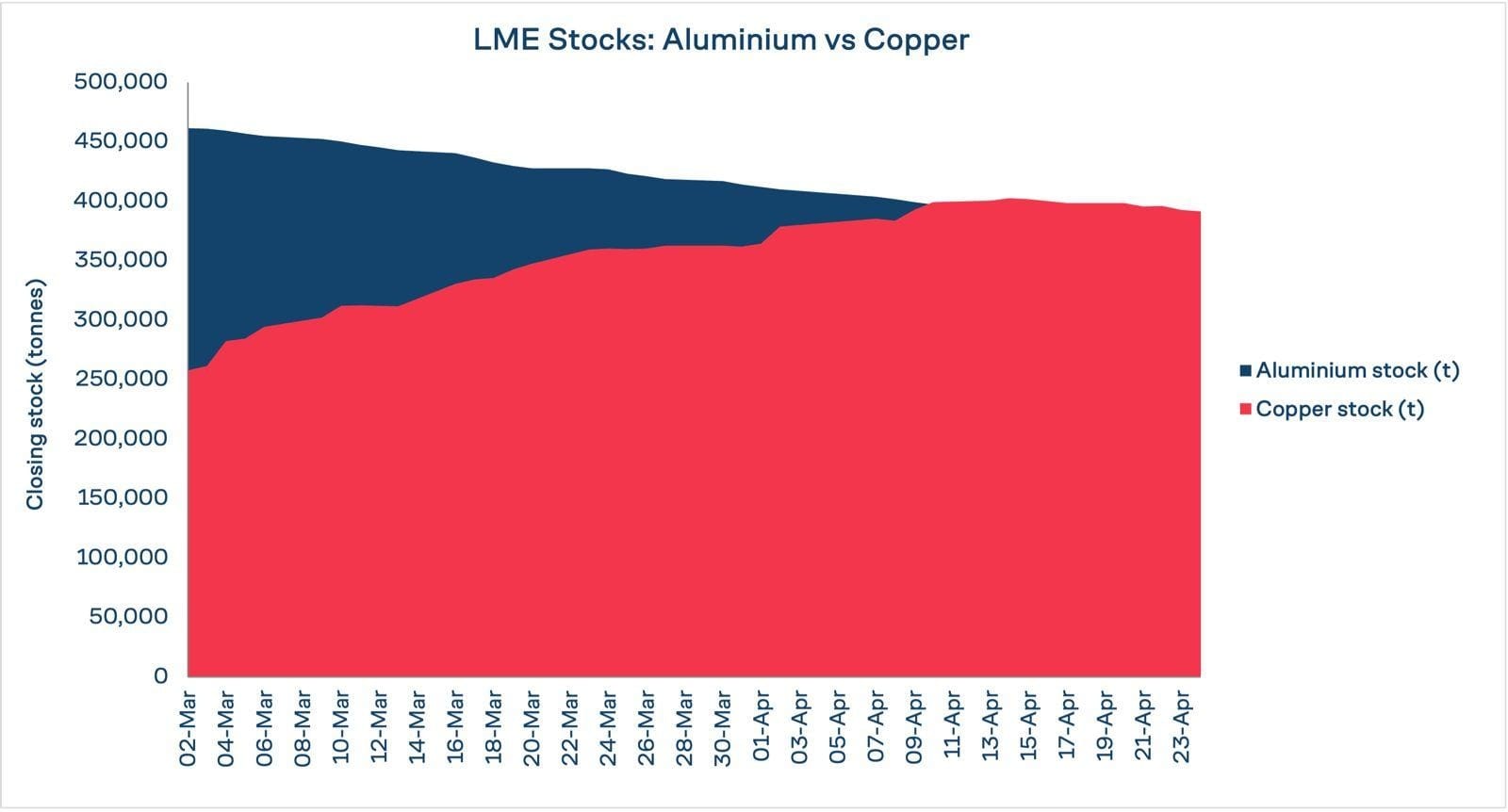

Aluminium stocks on the LME fell from 386,250 tonnes on 17 April to 378,825 tonnes on 22 April, a draw of 7,425 tonnes in four sessions. The draw continued: by 24 April stocks had fallen further to 372,700 tonnes, a cumulative reduction of 13,550 tonnes across six sessions. Live warrants on 22 April stood at 335,000 tonnes, meaning 43,825 tonnes of headline inventory is cancelled or pending withdrawal from exchange availability, though cancelled warrants are sometimes rewarranted. That live warrant figure held at 335,000 tonnes through 24 April. The effective pool is smaller than the total stock number implies.

The draw reflects tightening physical availability rather than short-term positioning.

In the Middle East, the region's six smelters depend on imported alumina, the intermediate product between bauxite and metal. The Al Taweelah refinery, part of Emirates Global Aluminium's integrated complex, sustained missile damage. Other Gulf smelters are running at reduced capacity. Qatalum and Aluminium Bahrain have announced reduced output. Saudi Arabia's Ma'aden, the only fully integrated Gulf producer, has been arranging limited emergency alumina supplies to others.

The supply disruption has moved beyond production. Emirates Global Aluminium has declared force majeure on some aluminium billet contracts with European customers following an Iranian attack on one of its UAE smelters in late March. Deliveries from Kubikenborg Aluminium, Sweden’s only aluminium smelter and a significant supplier to European markets, were halted on 9 April while its chief executive came under investigation in Sweden for possible sanctions breach linked to Russia’s war in Ukraine. Two separate constraints, from opposite ends of the supply chain, tightening European availability simultaneously.

The second constraint is less visible but potentially more disruptive. Coal tar pitch, used to manufacture the carbon anodes required in the smelting process, cannot be easily rerouted. Unlike calcined coke or petroleum coke, liquid pitch requires heated storage, heated silos, and heated trucks from the loading to the discharge point. Those facilities are not widely available. Every day the Strait of Hormuz remains closed to shipping adds pressure to a carbon supply chain with no flexible bypass.

The supply squeeze is already visible in physical markets. Premiums paid by buyers to secure aluminium have surged, with surcharges for aluminium billet reported to have more than doubled in Europe in the six weeks since the US and Israel attacked Iran. Analysts at JPMorgan Chase have warned that deep production losses are now inevitable and are forecasting that the market will face its biggest supply deficit in more than 25 years.

The cash to 3M spread on 24 April reflects all of this. Aluminium cash stood at $3,683-3,685/mt against a three-month price of $3,598-3,600/mt. The market is in backwardation: prompt metal commands a premium over deferred delivery. The backwardation has been widening: $47/mt on 22 April, $52/mt on 23 April, $85/mt on 24 April. The backwardation indicates tightening prompt availability. That physical floor does not make aluminium immune to sentiment.

On 19 March, LME Aluminium fell more than 8% in a single session, its largest one-day decline since 2018, as broader fears about the war’s impact on the global economy triggered a selloff across industrial metals. The physical constraint sets a floor. It does not cap the downside when macro conditions turn.

LME Copper stocks rose from 395,575 tonnes on 21 April to 396,000 tonnes on 22 April before holding broadly flat. The headline number has been climbing for weeks. Total CA inventory stood at 398,425 tonnes on 17 April. Copper stocks opened in April at 364,450 tonnes and reached 396,000 tonnes by 22 April, a build of 31,550 tonnes across the month. The direction is flat to rising, not drawing.

But the headline is misleading. Live warrants on 22 April stood at 343,950 tonnes, representing 86.9% of total stocks. Cancellations remain limited. The available pool is large relative to aluminium, and the cash to 3M spread confirms it: copper on 24 April was in contango, with cash at $13,229-13,230/mt against a three-month price of $13,290-13,295/mt. The market is paying more for deferred delivery than for prompt metal. The contango structure suggests adequate near-term supply.

That spread reflects exchange inventory conditions; it does not capture off-warrant stocks or Chinese domestic availability, which are separate questions. Copper also carries a structural supply narrative of its own. Mine supply growth has been slowing for years and the energy transition remains a long-run demand driver. The market today is not physically tight, but the premium reflects risk being priced ahead of fundamentals, not simply noise.

What is moving copper is sentiment and arbitrage. The US tariff threat on imported copper pulled metal into American warehouses earlier this year, inflating LME inventory and stranding supply that might otherwise have tightened the exchange pool. Chinese smelters are running at record output on the back of improved sulfuric acid margins. Physical supply is not yet showing stress in exchange indicators, though tightening in off-warrant or over-the-counter markets would not necessarily appear in LME data before it registers in prices.

The price, however, has been volatile. Copper fell from its highest close since February after Middle East peace talks stalled, then recovered on reports of a ceasefire extension. Recent price movements are not aligned with changes in exchange availability. They track geopolitical sentiment. Copper’s price strength reflects financial positioning rather than immediate physical tightness.

Western aluminium production fell by an annualised 312,000 tonnes in March due to Gulf curtailments. Chinese production rose by 88,000 tonnes in the same period. China's share of global output reached a record 60.2% last month. These are structural shifts, and they are not temporary dislocations. Smelters that curtail do not restart in days. The physical constraint in aluminium is durable.

The constraint is not limited to primary aluminium or European markets. India’s secondary aluminium sector, which produces nearly half of the country’s 4.2 million metric tonnes of annual output from imported scrap, is running at 20 to 40% reduced capacity as Middle East scrap supplies dry up. Scrap prices have risen nearly 30% since the conflict began. The disruption is feeding through to Indian automotive OEMs, which consume around 60% of domestically produced secondary aluminium. That assessment is finding support in capital allocation. The Financial Times reported on 24 April that Swiss trading house Mercuria is taking a 25% stake in an aluminium smelter in Indonesia operated by Chinese group Tsingshan, its first equity investment under its metals unit and estimated to be worth hundreds of millions of dollars. Kostas Bintas, Mercuria’s head of metals, told the FT the group was “very constructive on aluminium,” citing the conflict’s squeeze on supplies. LME Aluminium prices have risen about 14% since the war began.

Copper is seeing record Chinese refined output, rising LME stocks, and a contango curve all pointing to a market that is adequately supplied at current prices. The price is elevated because macro conditions and tariff uncertainty have made it so, not because the physical market demands it. For now.

This divergence has implications for how each market may respond to changes in macro conditions. A ceasefire confirmation or a shift in tariff policy could deflate the financial premium in copper quickly. Aluminium would not follow in the same way or on the same timeline. Aluminium prices are also sensitive to sentiment, particularly around energy costs and industrial demand, but the current price has a physical floor that copper lacks. Aluminium’s price is supported by physical supply constraints. Damaged refineries, stranded alumina cargoes, and a pitch logistics problem have no easy fix.

Those constraints persist regardless of what happens to sentiment.

LME price and stock data: LMElive official reports, 1 April to 24 April 2026. 19 March aluminium price decline: Golden Ten Data, 19 March 2026. Production data: International Aluminium Institute, March 2026. Gulf supply chain analysis: Wood Mackenzie, AZ Global Consulting, via Reuters, 23 April 2026. Aluminium billet premium, EGA force majeure and Kubal delivery halt: Reuters, 28 April 2026. India secondary aluminium sector disruption: Reuters, 28 April 2026. Mercuria capital allocation and Bintas quotes: Financial Times, 24 April 2026. JPMorgan supply deficit forecast: Bloomberg, 17 April 2026. Yan Weijun copper market assessment: Bloomberg, 23 April 2026.

It was another mixed week across the LME base metals complex. Aluminium finished modestly higher but that was the only metal to end the week in positive territory.

Copper concentrate deliveries from Mongolia's Oyu Tolgoi mine returned to normal after protesters briefly blocked a key export route to China.

The Iran ceasefire is being read as good news for Gulf aluminium producers. The spread data tells a different story.

Protesters blocked a transport route serving Rio Tinto's Oyu Tolgoi mine in Mongolia, disrupting copper concentrate exports and prompting warnings of economic losses.

Stay connected with our latest developments. Share your details to receive updates and analyses from LME Insight.