Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.

Aurubis – Europe’s largest copper smelter – reported this week that treatment and refining charges have dropped from nearly a third of its gross margin to just over a fifth in twelve months. The politics of reshoring hasn’t changed. The economics have gotten worse.

Treatment and refining charges across copper, aluminium, and nickel have reached levels that make new Western processing investment economically indefensible. The political case for reshoring is not wrong. The timeline implied by current economics is.

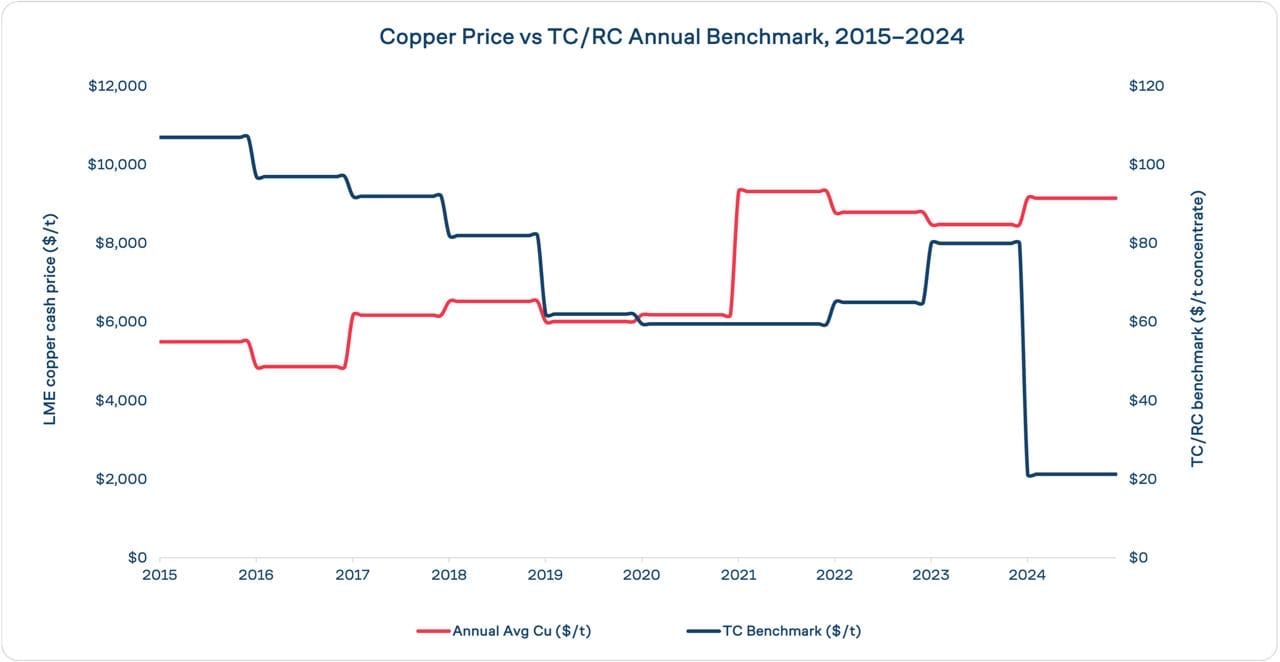

Copper: When The Processing Fee Disappears, So Does The Investment Case

Treatment and refining charges are the fees smelters earn for converting copper concentrate into refined metal. They are not a trading signal. They are the commercial foundation on which smelting investment is made. When they collapse, so does the economics of building new capacity.

The collapse has been swift and structural. The 2024 annual TC/RC benchmark, agreed between Chinese smelters and Antofagasta, settled at $21.25 per tonne – already a record low at the time. By December 2025, a Chinese smelter and Antofagasta agreed $0/t for 2026. Spot TCs spent most of 2025 below zero, reaching minus $60 per tonne by November. These are not cyclical fluctuations. They represent the most acute concentrate scarcity signal the market has produced since China’s smelting expansion began.

The mechanism driving this is straightforward. Global smelting capacity, led by China, has expanded faster than mine output. China produced 9.7% more refined copper year-on-year through October 2025, even as spot TC/RCs turned negative. Chinese smelters sustain this through by-product revenues. Sulphuric acid, gold, and silver offset negative concentrate margins. Smelters in the collective West do not have that buffer at the scale required for by-product to become a stable source.

The consequences are visible across Western smelting nations. Japan’s JX Advanced Metals and Mitsubishi Materials announced tens of thousands of tonnes of output cuts as underwater fees eroded margins. Glencore required a government rescue package to keep its Mount Isa smelter and refinery in Australia running for a further three years. In October 2025, the industrial ministries of Japan, South Korea, and Spain issued a joint statement at LME Week warning that current TC/RC conditions make sustainable development impossible for smelters and miners alike.

Germany’s Aurubis, Europe’s largest copper smelter, is the most instructive case study. In its Q1 2025/26 results, the company confirmed that lower TC/RCs had a direct dampening effect on earnings. Its CEO, Toralf Haag, stated publicly that Aurubis pays approximately three times more for energy in Germany than at its US operations. Importantly, he described the European permitting and energy environment as moving too slowly to support new investment.

Aurubis’s strategic response is telling: its most significant new-build – the Richmond, Georgia plant, the first greenfield smelter constructed in the US in over a century – is a secondary recycling facility, processing complex scrap rather than primary concentrate. The United States only has two active primary copper smelters – Rio Tinto’s Garfield facility in Utah and Freeport-McMoRan’s Miami operation in Arizona – both over a century old. That is not a bet on Western primary smelting. It is a deliberate routing around the bottleneck.

The concentrate bottleneck is structural, not cyclical. It sits at the mine pipeline, not the smelter gate. Global mine output has lagged available smelting capacity by an estimated 1.5 million tonnes of copper content. Building new Western smelting capacity does not resolve a shortfall that originates upstream and can’t solve the energy and regulatory problems facing producers. It adds capacity to compete for concentrate that does not exist.

Aluminium: Stranded Capacity As Power Economics Block Restarts

The aluminium story is different in mechanism but similar in outcome. Western primary smelting capacity did not gradually decline. It collapsed under a single identifiable cost shock, and has not recovered.

Between 2022 and 2023, Europe lost five of thirteen primary smelters as the post-Ukraine energy shock made production uneconomic. Approximately 1.4 million tonnes of annual capacity was suspended by the end of 2022. Europe now covers less than 15% of its own aluminium needs from primary domestic production, against demand of approximately 9 million tonnes per year. Most curtailments have not reversed.

The reason is not that supply is tight – it is not tight enough. Aluminium smelting is an electricity-intensive process. The economics require access to long-term, low-cost power that European industrial pricing no longer offers. The Aurubis data point is illustrative: if a copper smelter faces a three times the energy cost differential between Germany and the US, primary aluminium smelters, far more power-intensive operations, face an equivalent or greater structural barrier.

The US position is weaker still. American primary aluminium capacity peaked at 4.64 million tonnes per year in 1980 and stood at just 670,000 tonnes in 2024. No significant new primary smelting investment has been announced. The Iran conflict added further pressure during 2026, with Japanese producers cutting output as Gulf supply chains came under strain. Commodity trader Mercuria described the cumulative aluminium supply disruption as a black swan event.

Smelter restarts require a sustained price premium sufficient to cover power costs at European or North American industrial tariffs, plus a credible long-term power contract. Neither condition currently exists at the level required to trigger a committed restart. The investment decision is not primarily about metal prices. Power prices remain prohibitive.

Nickel: Surplus That Has Structurally Displaced Western Refining

Nickel presents the starkest case. Indonesian processing capacity, built at scale over the past decade through HPAL and RKEF technology, has structurally displaced Western nickel refining. Indonesia’s ore export restrictions, introduced progressively from 2020, forced downstream investment onshore, creating a vertically integrated processing base that now dominates over 50pc of the global supply of battery-grade nickel intermediates, as well as a large chunk of overall nickel production.

The result is a structural oversupply of Class 1 nickel and nickel intermediates at a cost base that Western producers cannot match. LME warehouse stocks have remained elevated with no sustained drawdown pressure. The carrying costs of that surplus are priced into a persistent deep contango. A brief tightening early this year, driven by Indonesian ore supply constraints and a two-year price high, eased the contango modestly but did not change the structural direction.

New Western refining investment into this environment is unfeasible. The challenge is not access to technology or capital in the abstract. It is that the landed cost of Indonesian supply undercuts any realistic Western production cost. The gap will not close without either a sustained price re-rating or structural intervention into Indonesian supply, neither of which is within Western policymakers’ hands.

What The Economics Say About Reshoring

Each metal is beholden to a different constraint. Copper refining faces a concentrate bottleneck that makes new primary smelting capacity redundant. Aluminium is shackled by a power cost structure that makes restarts uneconomic. And Nickel is under the control of costs and policies imposed by Indonesia that make new Western investment uncertain at best, indefensible at worst.

France has called a G7 meeting to address China’s stranglehold on critical materials processing. G7 trade ministers have sought common ground on securing critical minerals supply chains while simultaneously managing US-EU tariff disputes that strain the unity they are trying to project. Japan, South Korea, and Spain issued their joint statement on copper TC/RCs at LME Week – a measure of how far conditions had deteriorated – then returned home to manage smelter curtailments. Columbia University’s Center on Global Energy Policy, in analysis published in May 2026, concluded that existing Western smelters are not profitable without government ownership or significant state support.

The common thread is that processing economics, not political intent, determine where refining capacity gets built. TC/RCs tell a CFO whether a smelter earns its keep. Power tariffs determine whether an aluminium plant can operate at all. Cost-of-production differentials determine whether a nickel refinery is viable. These are investment inputs. They do not respond to G7 communiques.

New smelting and refining capacity takes five to ten years to plan, permit, and construct. The capital commitment required to begin that process today does not appear on any announced balance sheet at scale. Aurubis’s most ambitious US expansion – described by its CEO as a long-term strategic vision – is a recycling plant, not a primary smelter.

The political argument for reshoring is not wrong. The economics argument to fund it has never been so far from right.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Hydro's Slovalco aluminium plant in Slovakia has agreed terms with the Slovak government to restart 75,000 tonnes of primary aluminium production capacity, with output expected to begin in the fourth quarter of 2026.