Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

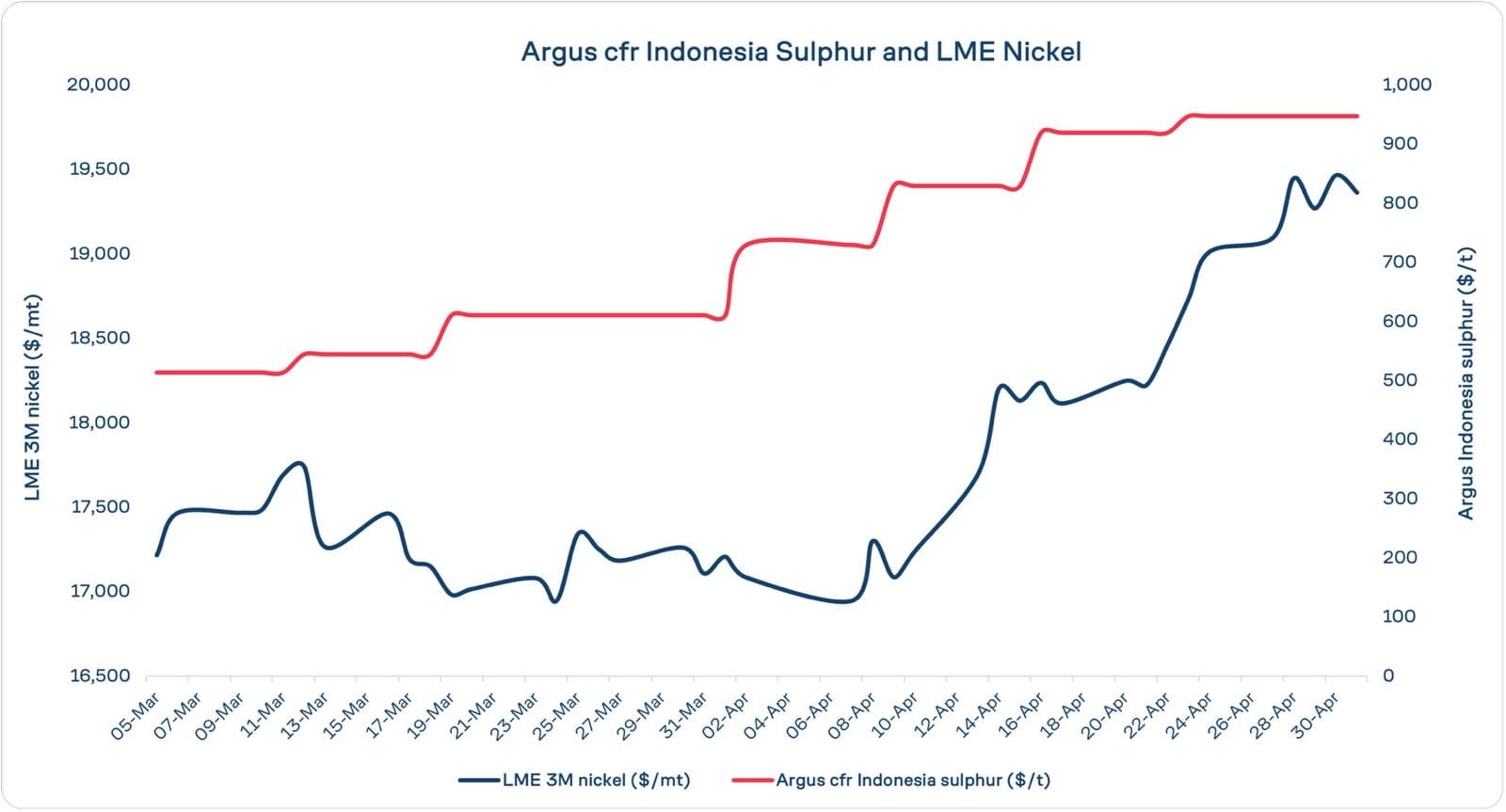

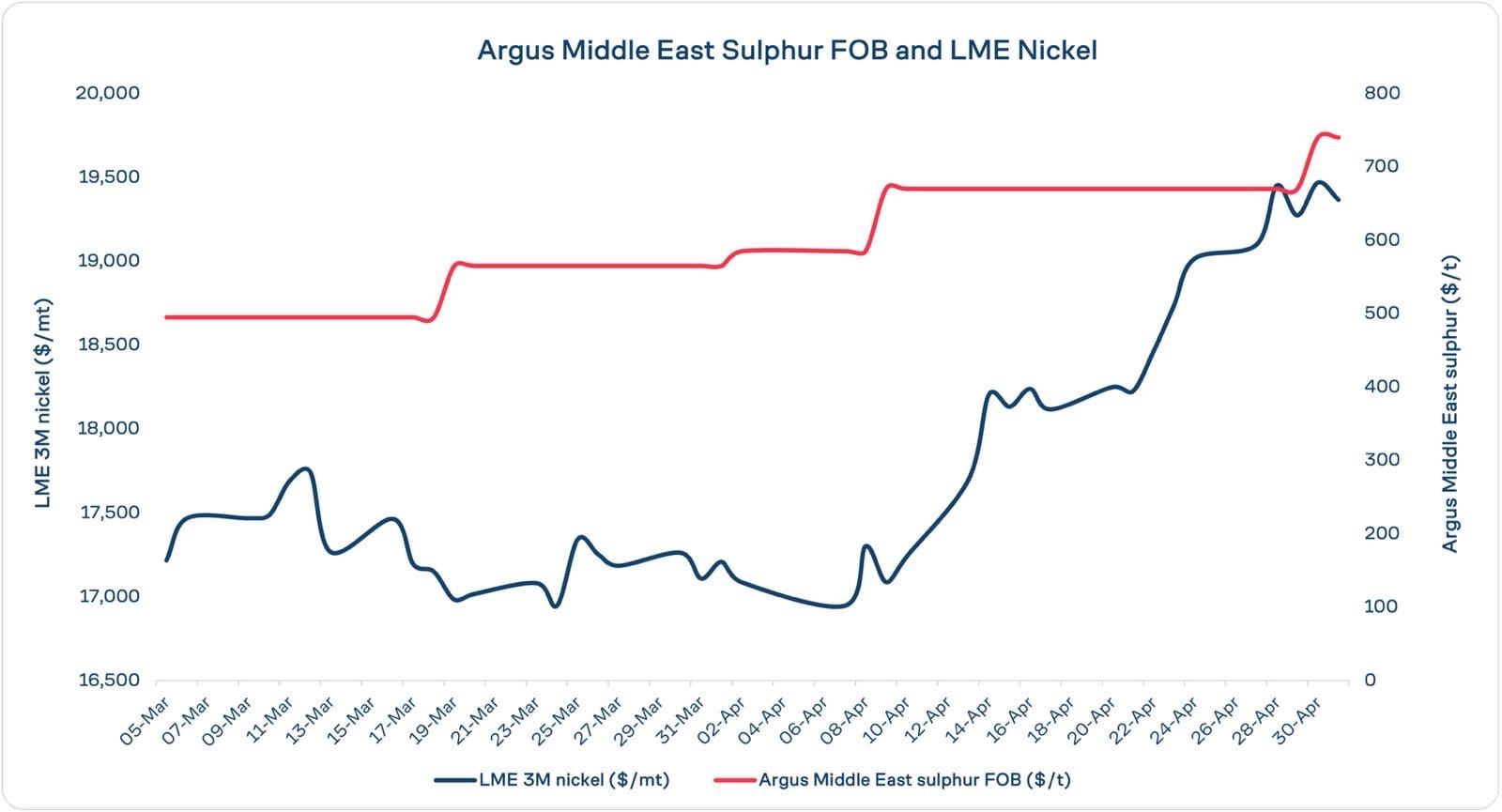

Nickel markets are focused on Indonesia’s quota cuts – but tightening sulphur supply is the real story. Disruptions in Iran, the Gulf and China, combined with declining hydrocarbon output, are constraining availability and reshaping the market balance.

Nickel on the London Metal Exchange touched $19,365/mt on 1 May, its highest since June 2024.

The market’s explanation was straightforward: Indonesia cut its production quota, mixed-hydroxide precipitate (MHP) output is under pressure, and sentiment is positive.

That framing is correct, as far as it goes. But it does not go far enough. The real mechanism driving this market is not Indonesian policy, it’s sulphur.

LME three-month nickel has risen 7%, from around $18,100/mt in late February 2026 to $19,365/mt on 1 May, as US-Israeli strikes on Iran began. Iran is a significant sulphur producer, and so are other major Gulf states. Its hydrocarbon processing sector generates recovered sulphur as a byproduct of oil and gas operations. The UAE, Qatar and Saudi Arabia are also in the same position. Ras Laffan, the natural gas facility struck early in the war, is one of the world’s single largest producers of sulphur. Disruption to the sector removes sulphur volumes from a market that was already tightening structurally before the first strike landed.

Sulphur is the reagent that makes modern nickel processing possible. High-pressure acid leach (HPAL), the technology that unlocks nickel and cobalt from Indonesia’s vast laterite deposits, is acid-intensive processing. Sulphuric acid consumption runs at 25 to 30 tonnes per tonne of nickel produced via that method. Indonesia does not produce meaningful amounts of sulphur domestically.1 Acid either arrives as elemental sulphur imports and is converted locally, or is shipped in directly. Either route is now more expensive. China has announced plans to suspend sulphur exports from May, removing a further source of supply.3

The Market Is Pricing A Forward Problem

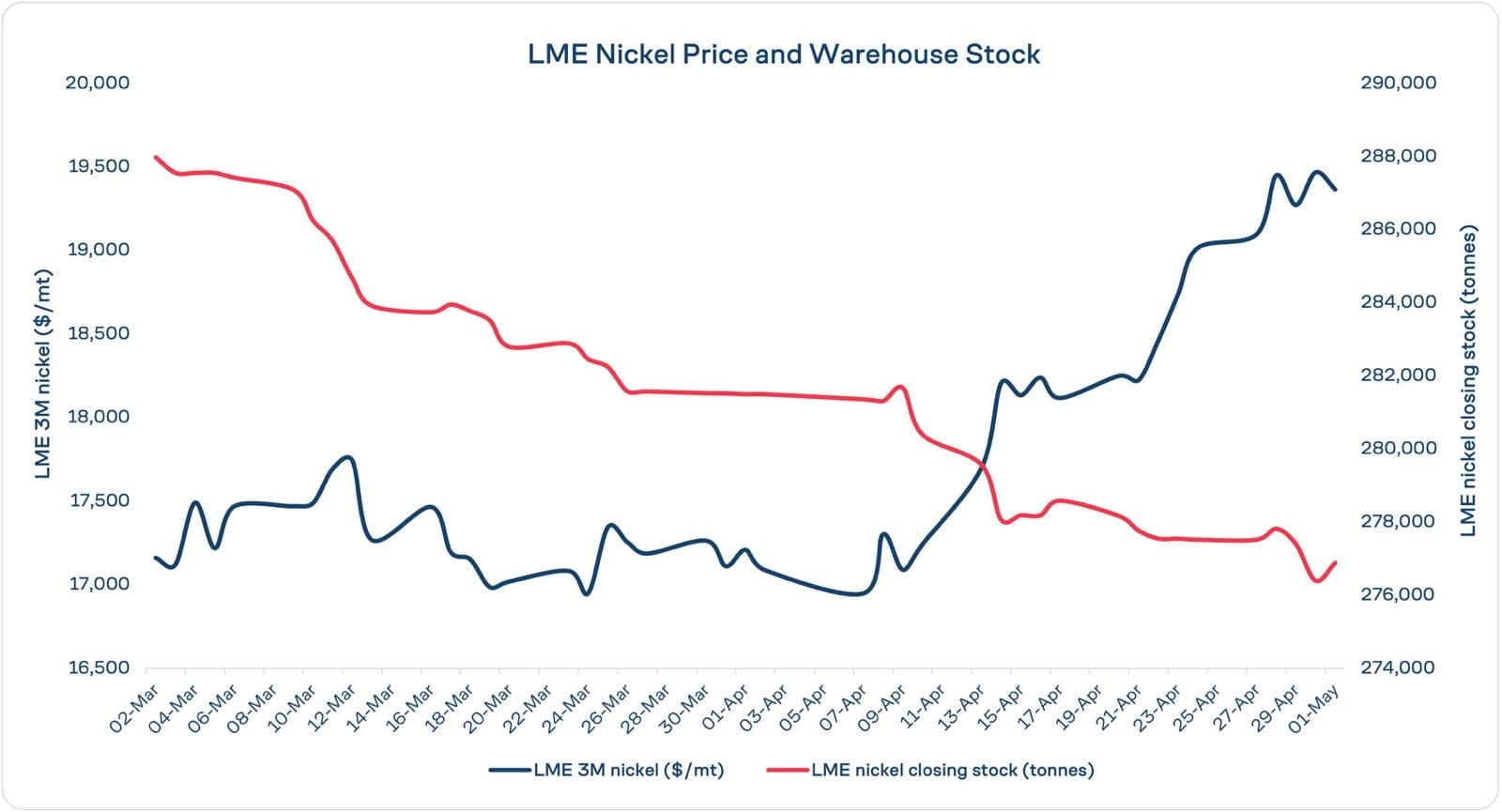

Unlike in the aluminium market, the market is anticipating a future supply issue, not an immediate squeeze. The LME warehouse picture tells a story of orderly tightening rather than acute stress. Closing stocks fell from 287,976 tonnes on 2 March to 276,888 tonnes on 1 May, a draw of 11,088 tonnes over nine weeks. Cancelled warrants, the fraction of registered stock queued for physical removal, ran at 13,638 to 21,090 tonnes across the period, reaching 13,638 tonnes or 4.93% of closing stock on 1 May.4 Active but not alarming. For context, the 2022 short squeeze saw cancellation rates above 50%.

The market structure reinforces this reading. Cash traded at a $183/mt contango to the three-month price on 1 May, a spread that has held consistently through the rally. Backwardation, the condition that signals a physical market pulling hard on nearby material, has not materialised. The market is repricing a forward supply problem, what Indonesian MHP output looks like if sulphur costs remain elevated through the second half of 2026, rather than reacting to an immediate one. The shape of the curve is consistent with sulphur cost pass-through into H2 2026 MHP economics rather than a near-term physical squeeze.

That distinction matters. Market sentiment is awaiting catalysts pointing to a substantial MHP production cut.4

The Copper Floor Is Also At Risk

The second-order transmission runs to the copperbelt. Solvent extraction and electrowinning operations in Chile and Zambia, which use sulphuric acid for heap leach processing, face the same input cost inflation. SX-EW copper is typically the marginal production that sets the cost floor for the copper price during periods of concentrate tightness. Pressure on SX-EW margins in southern Africa and the Andes is a read-across to copper supply that has not yet entered the mainstream narrative.

There is structural irony in the sequence. The energy transition reduces recovered sulphur supply by cutting hydrocarbon throughput over time. The same transition increases sulphur demand by expanding HPAL nickel capacity, itself required for battery production. The two effects compound. The Iran conflict has accelerated a tightening that was already in motion.

The buffer against that tightening is thin. Sulphur has no large-scale alternative source. Recovered production from oil and gas refining accounts for the dominant share of global supply. Mined sulphur, once the primary source, is now a marginal contributor. If refinery run rates continue to fall and Iranian supply remains constrained, the market moves from tightening to structural deficit without a clear release valve.

Nickel is pricing the first chapter. The rest of the mechanism is still being written.

1 Sulphuric acid consumption per tonne of contained nickel in HPAL processing of Indonesian laterite ores; range reflects variation in ore grade and limonite/saprolite feed mix. Source: Sumitomo Metal Mining and Vale operational disclosures. 2 China sulphur export suspension: Reuters, May 2026. 3 LME nickel NI price data and warehouse stock data: LMElive official reports, 1 May 2026. 4 Jinrui Futures Co., market note cited in Bloomberg, 27 April 2026.

Weekly review of LME base metals markets covering aluminium, copper, zinc, lead, nickel, and tin, analysing price action, spreads, warehouse stocks, cancelled warrants, and the macro and physical drivers behind trading activity during the week ending 3 July 2026.

For decades, nickel has been priced according to chemistry, purity and form. Increasingly, however, industrial buyers are asking a different question: how was it produced?

Emirates Global Aluminium has reported that restoration work at its Al Taweelah site is progressing ahead of schedule, with 89 of the plant's 1,262 reduction cells restarted as of today.

Hydro's Slovalco aluminium plant in Slovakia has agreed terms with the Slovak government to restart 75,000 tonnes of primary aluminium production capacity, with output expected to begin in the fourth quarter of 2026.